Data_Note: Consumer Price Index Comes in Mild in May

Tariff price pressures not here yet, possibly related to front-running inventory buildups.

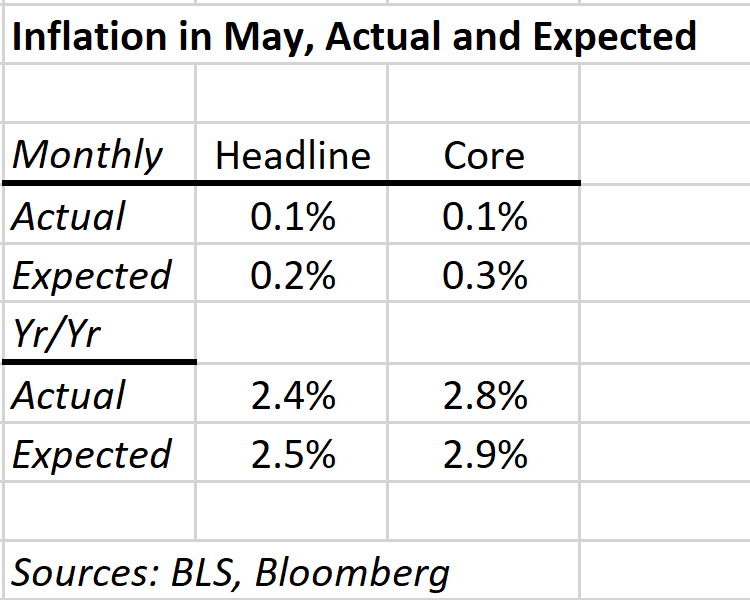

The CPI rose in below expectations last month, with little evidence of tariff induced price pressures. The core rate was particularly subdued, up just 0.1% (0.08%) against expectations for a 0.3% rise. On a yearly basis, both indices came in a tenth below expectations (see table below).

This looks like a mild report, showing continued disinflation with few obvious signs of tariffs pushing prices. To the contrary, the core goods category came in a zero for the month, apparel prices fell 0.4% in May (and were -0.2% in April), and new car prices came down 0.3%.

The soft headline number was pushed down by a larger-than-expected decline in gas prices, down 2.6% for the month and 12% for the year. The average national gas price this morning was $3.12 down from $3.44 a year ago. Analysts suggest the decline in gas prices is coming both from tariff uncertainty weakening consumer demand and an increase in OPEC+ supply (U.S. suppliers are dialing back production due to both of these factors).

Relatedly, airfares were down 2.7% in May, after falling a similar amount in April.

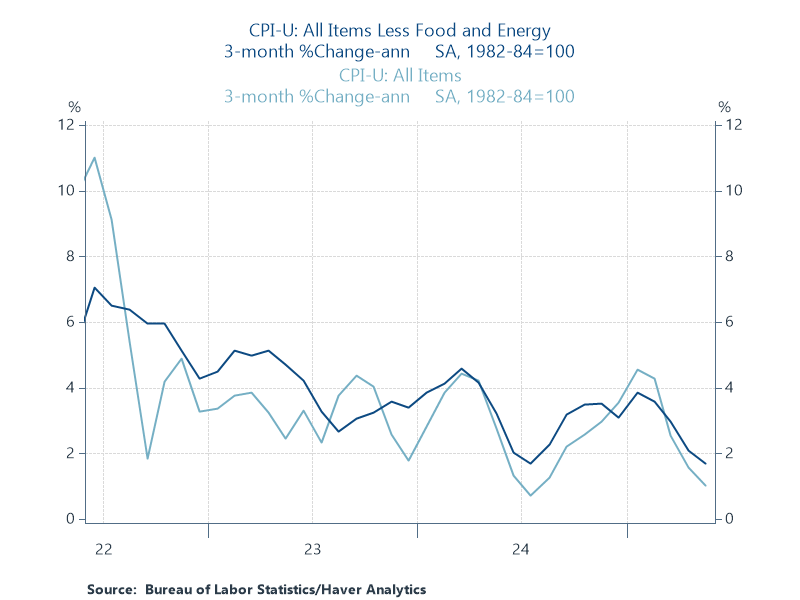

A good way to see the more recent trend in inflation is to look at 3-month annualized changes. On that basis, headline inflation was a mere 1% last month while core was 1.7%, tied for the lowest core rate since March 2021.

Groceries ticked up by 0.3% in May after falling 0.4% the prior month. Food packagers have said they’ll need to pass part of the recently doubled steel and aluminum tariffs forward to consumers as they raise the costs of soup, soda, and beer cans, but if that’s the case, it will show up in later reports.

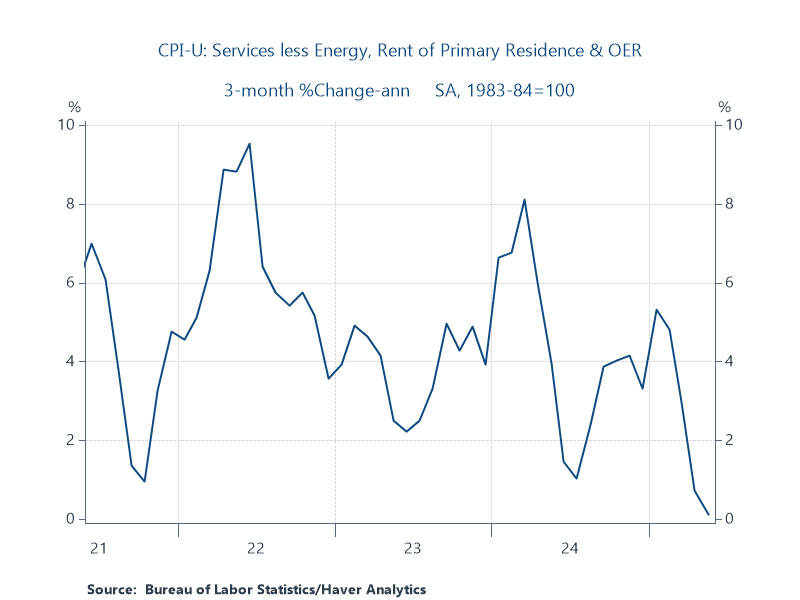

One group of prices that’s always worth checking in on is core services, ex-housing. This group comprises about three-quarters of the core CPI, and is therefore an important aggregation for gauging underlying price pressures. It ticked up on a yearly basis (not seasonally adjusted) from 2.7% to 2.9%, but the last few months have been soft, up just 0.1% (0.06%) in May. Thus, on a three-month annualized basis (again, a good way to gauge the most recent trend), we see substantial disinflation in this series.

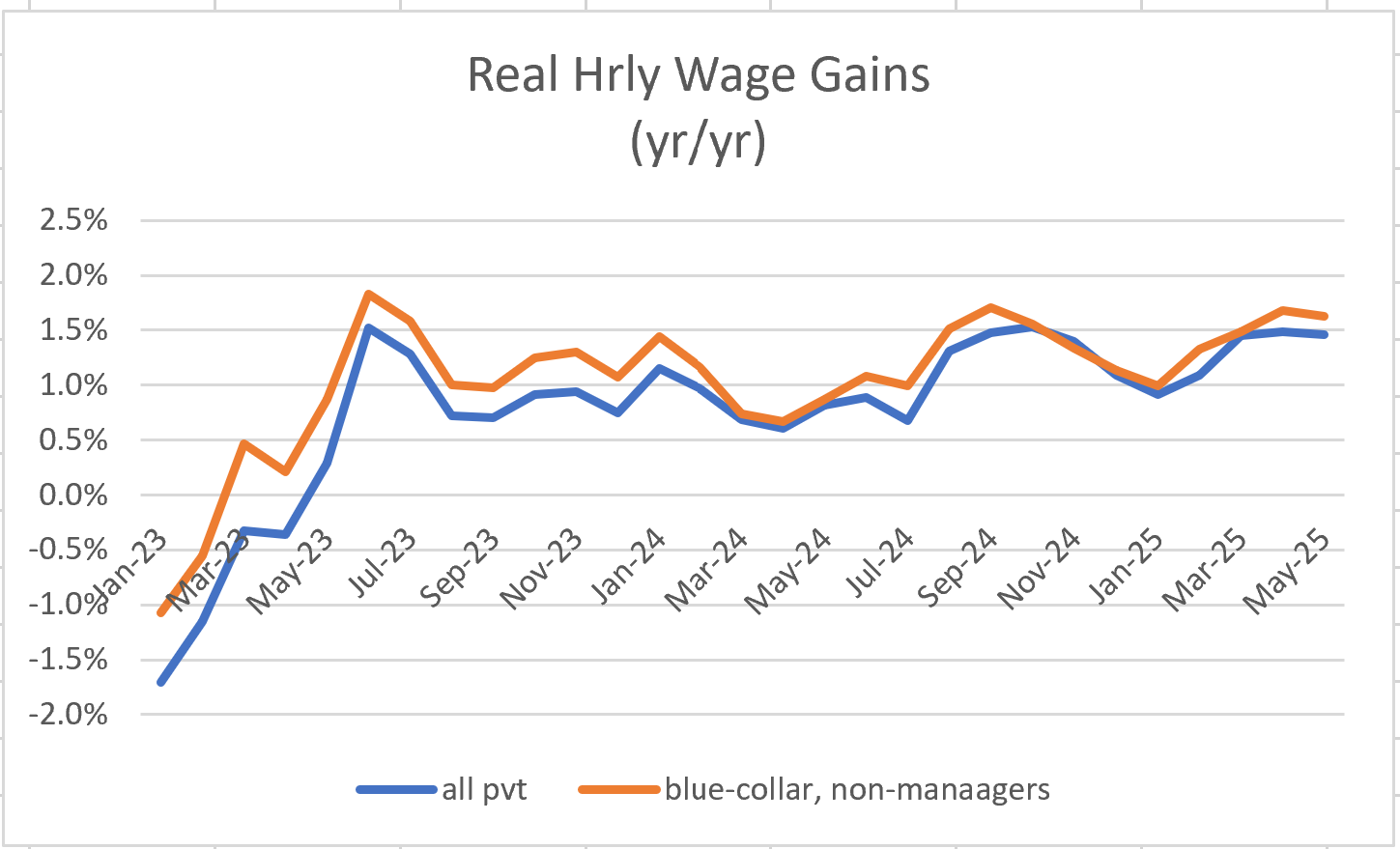

Lower-then-expected inflation means a nice pop for real earnings. Inflation-adjusted hourly wages were up about 1.5% over the past year for both all private-sector workers and for the 80% of workers that are blue-collar or non-managers. As the figure shows, these gains have been cruising along at this healthy clip for awhile.

Source: BLS, my calculations

My strong prior is that the combination of easing inflation, the still solid job market, and the consistently rising real wages shown in the figure above are a reliable recipe for continued expansion, driven by rising real incomes supporting consumer spending.

BUT…there’s no escaping the fact that the tariffs still lurk in the background. They’re mostly not in the hard data yet, but remember, firms that depend on imports aggressively front-ran the tariffs, jamming their inventories full in recent months. That provides insulation from their price effects which is likely reflected in today’s softer-than-expected report.

Lastly, what about our friends at the Fed? How might they absorb this info? As I see it, the last jobs report (decent job growth, layoffs still down, unemployment still low, decent but not scary wage growth) and this CPI report are a recipe for them to remain in wait-and-see-what-happens-with-the-tariffs mode.

Worth considering that many goods prices are really services prices. E.G.: $10 T-shirt from Bangladesh = $2 to buy shirt pre-tariffs + $0.25 ocean shipping + $0.65 handling + 0.45 port to store transit + $0.55 store handling + $2 store labor & overhead + $0.50 encumbered for writeoff if returned + $3.60 profit. A 50% tariff, even if fully passed through (unlikely), adds $1 = 10%. Not surprising that goods inflation is modest.

Home Depot recently reported that they would not raise prices to cover the cost of tariffs while other retailers have announced they will be increasing prices. This tells me that Home Depot's prices are already too high and they can still make a profit even with their increased tariff-induced costs. Home Depot, like other companies, more than likely took advantage of the elevated inflation in the recent past to aggressively raise prices and gouge consumers. I will no longer shop Home Depot.