Data_Note: Federal Reserve edition

Like a good jazzer whose lost in the tune: when in doubt, lay out.

Numerous lives ago, I was a jazz bassist, which of course requires improvisation over chord changes. Sometimes if you weren’t paying attention, you got lost, and in those situations, the applicable adage was “when in doubt, lay out,” meaning stop playing until you figure out where the rest of the band is, and then come back in.

At 2pm today, the Federal Reserve Open Market Committee (FOMC)—the folks who decide interest-rate policy for the Federal Reserve—will almost certainly announce that they’re keeping the federal funds rate where it is. That’s the interest rate they control—a benchmark for key rates throughout the economy—which currently sits at about 4.3%.

Why not cut rates to offset the potential drag on the economy from Trump’s policies? Isn’t inflation gradually, if bumpily, heading back to target? Haven’t forecasting firms (and the OECD) marked down their growth forecasts—generally from >2% to >1% for Q1 GDP—creating more room for a rate cut?

Because when in doubt, lay out.

As I’ve said a lot in recent commentaries, the hard data is still holding up even as the soft data’s been tanking. The Fed looks at both, of course, and rarely a speech goes by without the reminder that there policy decisions are “data driven,” which, for the record, means data-trend driven, not specific data-point driven.

Hard data—jobs, growth, and especially inflation—are paramount; their mandate from Congress is, in fact, stated in hard-data terms: to maximize employment at stable prices. But soft data matter too, including financial conditions and most importantly right now, as I stress below, inflation expectations.

They went into this meeting knowing that inflation forecasts have been marked up. Here’s the latest from the Goldman Sachs research team. The difference between their “no tariffs” and baseline expectations, which expects an historically very large 10 percentage point increase in the average tariff rate, is a full percentage point of inflation by the end of this year, ending up closer to 3% than the Fed’s target of 2%.

The FOMC, especially Chair Powell, have to be careful, for political reasons, about how they talk about the tariffs (can’t upset President Snowflake), but neither can they ignore the impact of the economic uncertainty generated by Trumpian whiplash in this space. In fact, during the Trump 1 trade war, they lowered rates as insurance against the negative growth impacts of a set of tariffs that were far more mild than the current batch.

That said, tariffs are less of a big deal for an inflation-fighting Fed than you might think. Because tariffs are a tax on imports, we expect them to bump up the price level of the effected goods, but we don’t expect them to necessarily push up the ongoing rate of inflation (this assumes that the tariffs are turned on, left on, and not added to, possibly a wrong assumption; this is how all the policy lurching around the tariffs is raising uncertainty through the roof). That’s why all the tariff-influenced forecasts in the GS forecast above drift down next year. Central bankers are taught to “look through” events that boost the price level but not the rate of inflation.

Unless, and this is a piece of soft data that matters a lot to the Fed, the tariffs de-anchor inflationary expectations, meaning they lead people to expect higher inflation, which can be a self-fulfilling prophecy and is basically the nightmare that haunts FOMC members in their sleep.

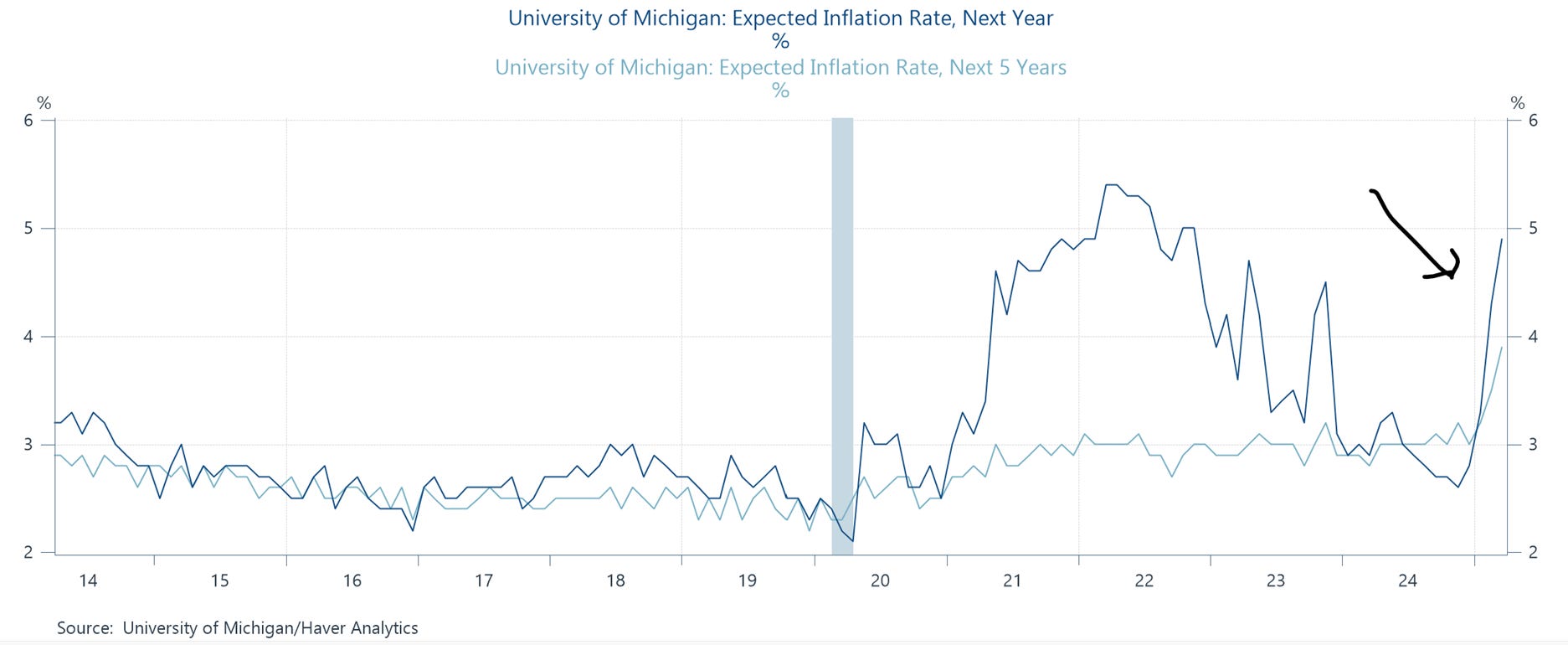

How do they track such expectations? By looking at surveys—soft data—on what people say about where they think inflation is heading, along with market indicators. You can bet that they saw the data below from a recent consumer sentiment survey from the University of Michigan. Note how shorter term expectations (“next year”) look something like inflation itself, but it’s the longer-term ones that matter most to the Fed. Back in ’22, one-year expectations had drifted way up, but the 5-year version was stable, suggesting people thought, correctly, that the inflation shock was pandemic-driven and would eventually subside. That pattern is very helpful to the Fed’s mission.

But this survey is of regular folks on the street, not people who set prices, so it’s hard to gauge the true extent of de-anchoring from it. It’s suggestive, not dispositive. And in this regard, it’s yet another reason for the Fed to be cautious, leave the rate they control where it is for now, and track the tariffs’ inflationary impacts from the two key perspectives discussed herein—a bump to the price level—not great, but not a biggie—versus de-anchoring—a definite biggie and, should it occur, a real problem.

When in doubt, lay out.

Thank you for your very readable explanations. But IMHO, you don't need to be an economist to know that the certainty they need is going to come in the form of very bad economic news.

Great analogy!

When I was playing bari-sax in a big band, the adages for when in doubt were:

A) play solo — so low no one can hear you;

B) play chromatic.

The latter might actually be the FED’s Plan B — make only the smallest incremental changes.