Data_Note: Retail Sales, Oil, Senate Bill

And a nudge to do lunch with me--and Bobby Kogan!--today at noon ET at the Contrarian.

Retail sales for May was another one of those damn tricky reports we keep getting that says one thing at the top and another thing below the surface. The report came in soft, down 0.9%, below expectations (-0.5%) with a lot of negatives for the months, led by auto and parts sales, down 3.5%. That’s two months in a row of flat of falling top-line sales (April: -0.1%…call that “flat”). Restaurants were also down 0.9%; groceries fell 0.8%.

But the core sales measure, the one that feeds in Q2 GDP was up 0.4%, slightly ahead of expectations. So, that muddies the water a bit. Still, there’s some evidence of consumer weakness in here. CNBC read the weak topline as a function of “looming unease over where the economy is headed.”

The weak auto sales likely reflects tariffs. March auto sales popped 5% in a frontrunning play, followed by declines in April and May.

We’ll see how the GDP prediction shops incorporate the sales report, but again, the key number there isn’t the topline, it’s the core, which was pretty solid. And at any rate, the trade balance and inventories have been so battered about by TTC (Trumpian Trade Chaos), that topline real GDP growth won’t mean much in Q2, same as Q1.

Remember also that retail sales is noisy, and covers less than half of consumer spending. So, not a great report, and given the extent to which consumer spending has been driving this expansion, any signs of shaky consumers is dangerous. But given the better core measure, I’d say this is flashing yellow at worst.

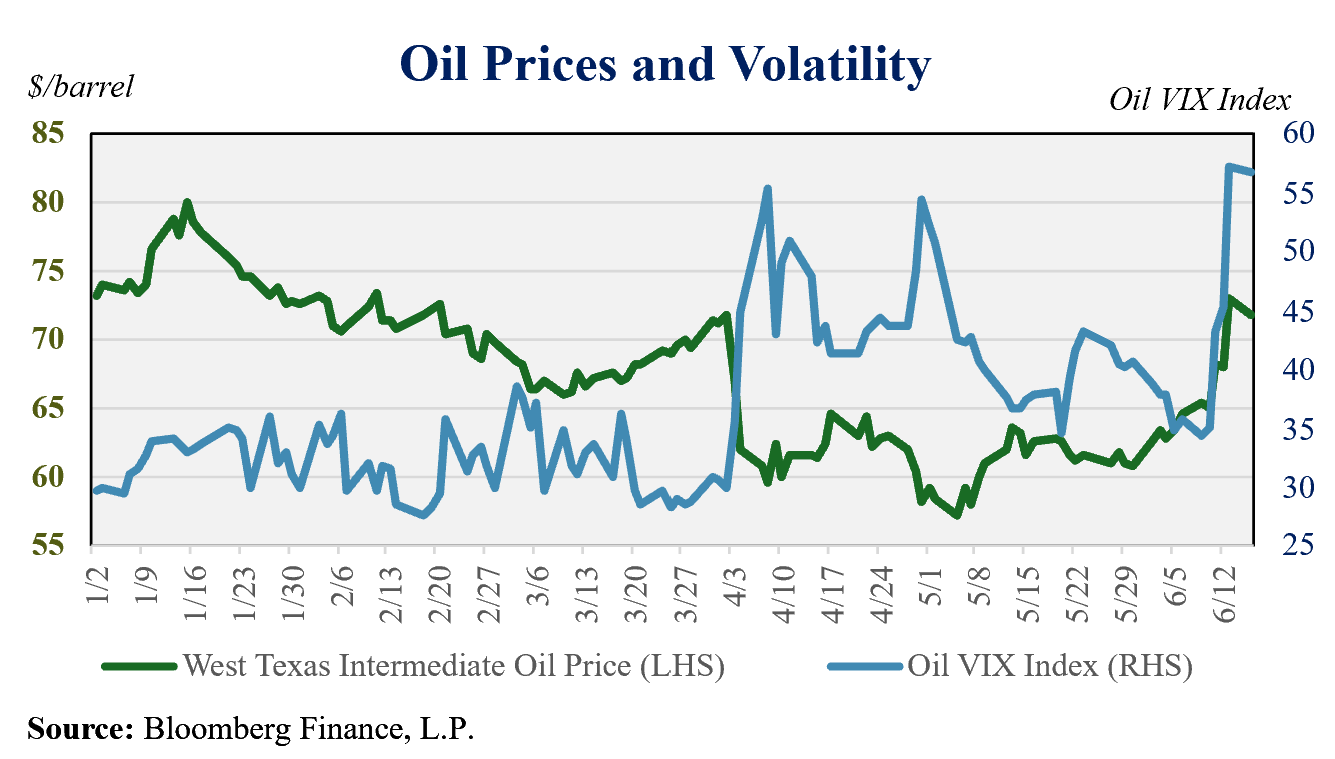

The Oil Price

Given the escalation of the Israel/Iran conflict, I was surprised to see the oil price go down yesterday and I’m less surprised to see it climbing this morning. Apparently, yesterday’s slide was due to oil traders expecting a relatively quick resolution, which looks a bit more like wishful thinking today.

There are three things to share on this.

First, this Bloomberg Interview with oil market expert Bob McNally is worth a listen. I found his take resonant, and was particularly attuned to the warning that Iran is not without cards. They could, as they've done before, decide to disrupt the Strait of Hormuz, which would lead to quick and very large spike in the oil price (“…risking an oil price spike is really the only leverage Iran has over Israel”). There are reasons to doubt such actions. American warships are already in the region and ready to protect this vital supply chain, and as McNally says, Trump will want to protect the price of gas. But as we saw with the Houthi’s in the Red Sea, stopping such actions can be harder than you might think.

Second, a barrel of WTI crude has climbed from about $60/barrel at the end of May to $73 as I write. Part of that is the onset of summer driving season, but movements in the the last few days reflect the conflict. Anyway, that’s more than $0.25 per gallon added at the pump, and if consumers are, in fact, already pulling back as per the sales report, that could be consequential to overall spending.

Third, my pal and close-energy-market watcher Ryan Cummings shares this slide with me, point out that “oil volatility—measured by an index referred to the Oil Volatility Index (or “Oil VIX” for short), has risen to its highest level since Russia invaded Ukraine.” It’s a clear sign of how this conflict adds to the already high levels of economic angst and uncertainty.

The Senate Version of the Big, Ugly Bill

We’re just learning about this now, and I’ll tout a way to get to the nub of it in a moment, but topline observations from what I’ve read are:

—The core tax cuts look mostly the same, though the Senate dials back the SALT cut. Interestingly, while there are R House members from states fighting to raise this cap, there are no R Senators from those states. Deeper thinkers than I can tell us where this might land as the two chambers reconcile their differences.

—Deficit implications seem similar if not larger than the House bill.

—Medicaid cuts go deeper, a truly harsh and terrible development. Also, the Senate reduces Medicaid payments to hospitals more so than the House.

—There’s a longer runway to phasing out IRA tax credits.

—Trump’s addition tax cuts—overtime, tips, seniors—are still in here but dialed back.

But if you really want to learn about what’s going on with this highly consequential budget, you’ve got to tune in at noon ET to Let’s Do Lunch on the Contrarian, with my guest today, Bobby Kogan. Bobby’s as deep a budget expert as we’ve got, but the weird thing about him is he somehow manages to untangle these weeds in ways that normal people can understand.

The Senate version of the Big Beautiful Bill is essentially the same as the House--deep regressive tax cuts for the wealthy, severe cuts in essential program spending, and trillions more in borrowing. I blogged about this in Forbes, press coverage saying there are big differences between House and Senate are misleading and normalizing this awful bill.

https://www.forbes.com/sites/richardmcgahey/2025/06/16/republicans-unbelievable-unity-not-division-on-big-beautiful-bill/

Slightly, but not totally off topic:

On the subject of volatility, have you read today's FT Alphaville article "The era of sudden shocks - revisited"? (link below)

There's a great graph showing "Standard deviation of annual US GDP growth per capita, 20 year time window" which depicts the rise of US GDP volatility from 1871 (the creation of the German Empire State) through to 1945 (the end of WW2) within an 1820-2020 frame.

Presumably, when GDP itself is very volatile, the internal, normally correlated measurements, suffer from declining R².

Economic forecasting is likely to become more and more difficult the more the great powers of the world are competing. And they are doing that.

https://on.ft.com/45rB8tu