Friday Mash-Up

Pushing a jumble of random thoughts from my mind to yours.

This just in: Most people agree with Ryan and me on crypto. The most common response to our NYT oped on how crypto values are tanking because a) there are almost no (legal) use cases, and b) the bros bought the president/Congress and their asset values are still tanking, was some combination of “duh!” and thanks for confirming our priors. A number of folks pushed back that the currencies are more useful than we say but I can’t recall any examples, outside of cross-border payments. And even that is suspect. Here’s Ryan responding to a question about this:

As for the international payments aspect, we hear this one a lot and it’s usually the first example of a “use case” trotted out by the industry. But the reason sending money abroad is expensive and inefficient is because of policy, not technology. That is, when you send money abroad, the U.S. government (rightfully) wants to ensure that you are not sending money to drug cartels or terrorist groups. And crypto is very good for this usage. As we mention in our piece, the Times recently reported Binance was facilitating billions of transfers to terrorist groups in Iran. That said, the cost of sending remittances and other cross-border payments is far too high, and there are alternative, cheaper, instant payment technologies that policymakers should explore (see, for example, FedNow https://explore.fednow.org/common-questions).

Folks, we have a currency. It works fine, though some have too much of it and many have too little. This country has a lot of big problems, of which crypto solves none, while introducing many new ones.

Trump and Biden Delivered the Same Non-Resonant Message: Also from the NYT, we have an accounting of how, in their respective SOTU speeches, both Biden and Trump talked past the people, touting an economy that bore little resemblance to their lived experience.

“Inflation is plummeting,” Mr. Trump declared on Tuesday. “Incomes are rising fast.”

“Wages keep going up,” Mr. Biden had said two years ago in his final State of the Union address. “Inflation keeps coming down.”

“I inherited an economy that was on the brink,” Mr. Biden said two years ago, blaming Mr. Trump.

“I had just inherited a nation in crisis with a stagnant economy,” Mr. Trump said on Tuesday, blaming Mr. Biden.

And both presidents claimed credit for a turnaround that voters had not bought into.

“Now our economy is literally the envy of the world,” Mr. Biden said in 2024.

“Now we are the hottest country anywhere in the world,” Mr. Trump said on Tuesday.

To be clear, I was an econ messenger as part of my role in the Biden admin, so I’m not employing the passive voice here (“mistakes were made…”). As I’ve said before, we talked past people but we didn’t gaslight them. We never said prices are down 600%, and not just because that’s mathematically illiterate. But while that means something to me personally, I recognize that it’s a distinction without a big difference.

I can tell you this, and it applies to all admins, even the current…um…bespoke version. There's a view, and it usually comes from the president himself, that “if we don’t tell our success story, no one else will.” When the president thinks that economy is better than most people think it is, he invariably seems to think it’s because they don’t know enough about what we’re doing to help them, and the reason they don’t know is that we’re not telling them. So, the comms function dials up the “tell them how we’re helping” machine, citing positive data reports along the way.

The thing is, I don’t know of any examples where that has worked.

We used to worry about insufficient demand. Now we worry about excess supply. This one’s admittedly obscure, and I’ve yet to absorb this new spate of literature, but there are a number of future-oriented reports predicting that agentic AI will finally deliver the massive technological unemployment that was the one big thing no less than Keynes got wrong (he thought we’d be there by now). The latest version argues that this will either be awful for growth, because while they’ll be much more output, it won’t be produced by workers, leading labor demand and wages to tank. Or, we’ll spread all that extra output/income around to everyone through some universal income plan.

First, of course this time might be different, but the reason this hasn’t happened thus far throughout the long sweep of history is that new tech doesn’t just create new supply. It also creates new demand. The internet wiped out business (e.g., travel agents) but created millions of new business opportunities. Again, I’m not denying AI, which even an old techno-challenged dude like me is finding to be remarkable on a daily basis, could be the gamechanger that breaks this pattern, but I don’t assume that’s the case. Human creativity has always found new demands from new technologies, which is why both productivity and hours worked have, broadly speaking, pretty much always trended up.

To be clear, you know my methods: hope for the best, plan for the worst. I’ve been out there advocating that policymakers start now constructing a robust AI insurance program, one that doesn’t just substantially beef up our unemployment insurance program but adds a job guarantee and a wage insurance component to it.

But my concern here is the same one it has always been. Who gets what? That is, my expectation is less that massive labor displacement will occur than the gains from new tech will flow disproportionately to the top, as has largely occurred thus far. My internal economic model is to worry simultaneously about growth and about the distribution of said growth. Should large productivity gains occur, I don't see what mechanism is supposed to channel them to the middle on down.

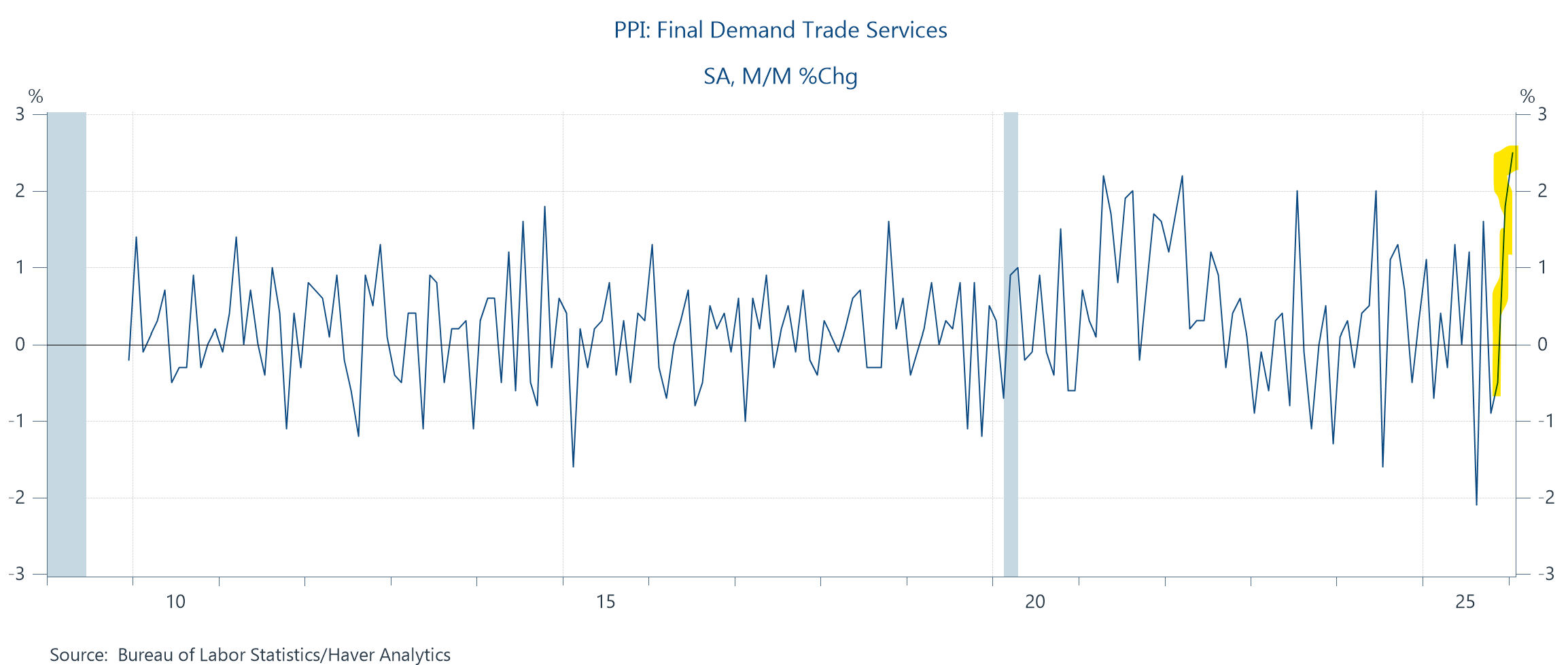

PPI spikes up: I’ve gotten a few queries whether this AMs PPI report (wholesale prices), which came in hot relative to expectations, is worrisome re inflation re-accelerating. I’d say mostly no.

—The core index came in at expectations of 0.3%.

—PPI is a noisy monthly indicator that is mostly relevant in that a subset of its components feed into the more important PCE deflator, and those components came in a slight bit below expectations.

—The firmest part of the report was services, up 0.8% for the month, and that did catch my eye. It was mostly the margins component (“trade services”, shown below), which is particularly jumpy and spiked to its highest monthly print on record. I wouldn’t over-torque on this at all, but if you follow my work on this, you know I’ve highlighted numerous indicators showing inflationary pressures in services, which are less linked to tariffs, so that remains on my watchlist.

I run a small retail Website. For a while, I was accepting Bitcoin and Ethereum as payment. As with paying by credit card, you filled out a form at checkout, which told you how much of either token you needed to pay.

You plugged in your public key, hit the purchase button and after the sale was validated, you received a "Thank you for your purchase" email message.

But...

Before shipping, I had to verify that the amount that came in roughly matched the amount of the sale, which was an extra step I don't have to make when people pay by credit card. And with crypto fluctuations, that amount could, a few hours after the sale, be a lot more or a lot less than the actual sale price.

After two years or so, I stopped accepting crypto, simply because crypto transactions made up about one half of one percent of my sales and it simply wasn't worth the effort.

My real motivation at the time was that I was dabbling a bit in crypto as a hobby and accepting it on my Website effectively allowed me to acquire Ethereum at the cost of my merchandise.

By the way - No one EVER used Bitcoin. The per-transaction fees were simply too high to justify paying that way. Every single crypto transaction was with Ethereum.

Re cost/hassle of cross border transfers, in Canada, TD Bank recently introduced a new international remittance system which permits us to transfer money almost instantly and free online from our TD account to anywhere in the world. Not sure what tech they'e using but it's super helpful. So far only used it for US $ transfers.