GDP posts a solid quarter and (another) strong year

DATA_NOTE: Don't be distracted by the headline miss

[Two maintenance notes: First, we’re all still reeling from the tragic crash over the Potomac last night, a few miles from where I sit this AM. This feels close-to-home in many ways, and we must learn what went so horribly wrong in that crowded airspace.

Second, there’s a bit of a bait-and-switch going on with this Substack. I originally signed up folks to get short, easily-digestible data notes like the one below (and like we provided at the Biden CEA), not a bunch of econ-punditry-chin-music on other stuff. But rather then have two different Substacks, I’ve decided to label the data notes as DATA_NOTE in the subhead, so readers will know what’s coming.]

The AM’s preliminary GDP report for 2024Q4 came a touch below expectations, but looked very solid under the hood.

Real GDP for the quarter up 2.3% at an annualized rate and 2.5% for the year (Q4/Q4).

Yes, that quarterly rate is down from Q3’s 3.1%, but these are all just buff rates, easily strong enough to support ample job creation, low unemployment, real wage and income gains.

Consumer spending was once again a standout, up 4.2% in the quarter (annualized). It’s the same old story: solid labor market (UI claims were fine this AM) driving strong consumer spending (68% of nominal GDP). That’s been a reliable recipe for steady, above-trend growth. Also, wealth effect (high-end wealth gains also in play here).

So, if spending overperformed, what underperformed to generate the expectations miss? Investment and inventories. The latter, by far the noisiest component (it’s a change-of-a-change!) took almost a point off of growth. Biz investment has been solid lately, but contracted last quarter. I wouldn’t read much into this…yet.

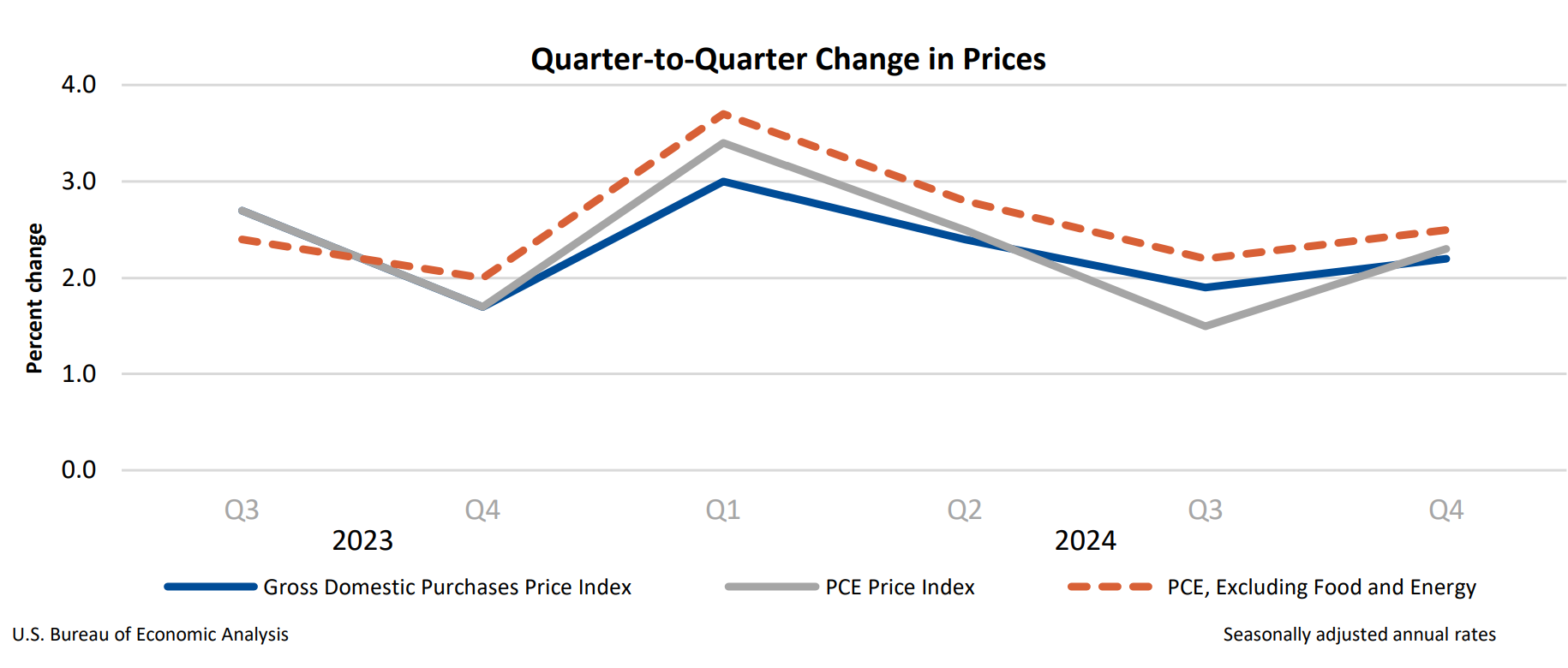

Price growth ticked up a bit but we already knew that. I’ll a bit more to say about that with tomorrow’s Personal Income release.

Other indicators we like to track looked good: sans-inventory real growth rates, which tend to give better takes on where we’re headed, were north of 3% in the quarter.

One shouldn’t typically measure growth rates over presidential cycles, versus biz cycles, but the 13% real growth over Biden’s term stands out as a great growth record. The president tacked for strong, steady growth driven by a healthy labor market supporting consumer spending, along with strong investment in key sectors. And that’s what he got.

Along with the 21-22 price spike, for sure. But the goal was to get inflation down without sacrificing growth, and that’s also what happened.