Good Macro, Bad Micro: The Vibes Gap Revisited and Explained

The second in a series of diagnoses and prescriptions.

A few days ago, I focused on the impenetrability of the near-term macro economy to Trumpian policy (longer-term, I’m quite certain real damage is occurring). I was careful to distinguish micro from macro, and in this post, I’ll dive a bit deeper into that distinction.

BLUF: A number of phenomena—political, economic, cultural, technological—are interacting to make macro-economic indicators less relevant than ever when it comes to people’s assessment of their well-being. To be clear, GDP growth is as necessary as ever, but it is increasingly insufficient.

A Deepish Data Dive

First, we need a data check on the vibes gap. There are many different surveys that attempt to gauge economic vibes, and their results vary significantly. But not that significantly—they all confirm the hypothesis of this post: there’s a large split between the macro-conditions I touted in my last post and how people are feeling about those conditions.

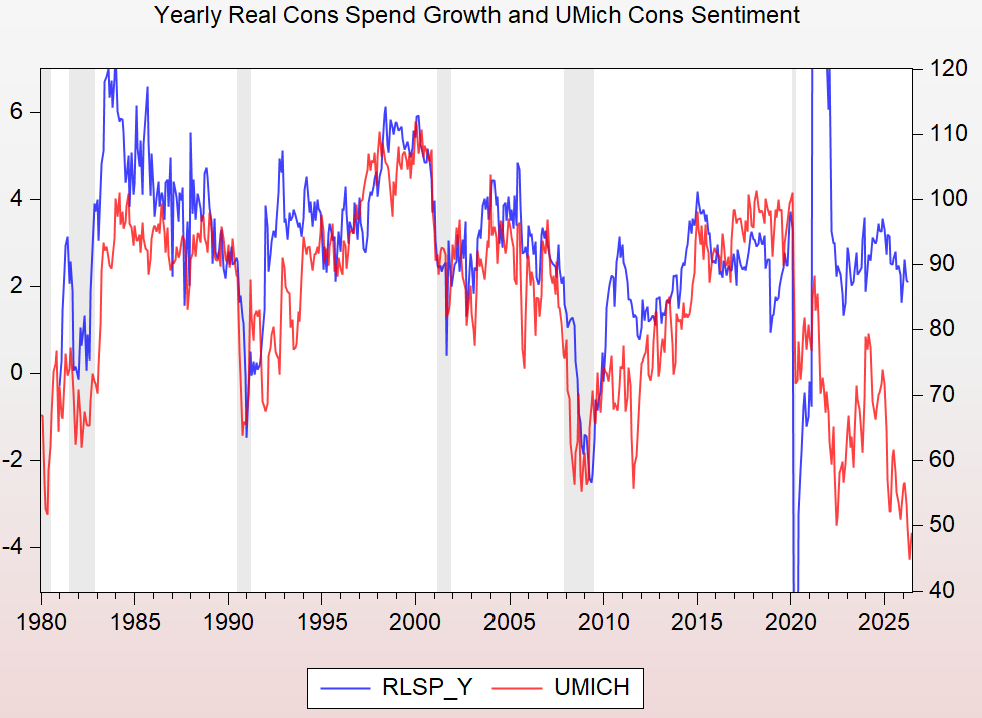

Probably the most common way to show the vibes gap is to elevate the recent divergence between the growth in real consumer spending and the UMich Sentiment Survey. In our paper, Daniel Posthumus and I dig deeply into this series, explaining that gap by referencing the sharp, post-pandemic spike in the price level. We find this series particularly useful for such analysis because it previously hug closely to the macro variables (in our paper, we show this is case with many other variables beyond just real spending) before it underwent a large, structural change. But it is also notable that UMich shows the largest and most relentless gap, seemingly unresponsive to macro improvements.

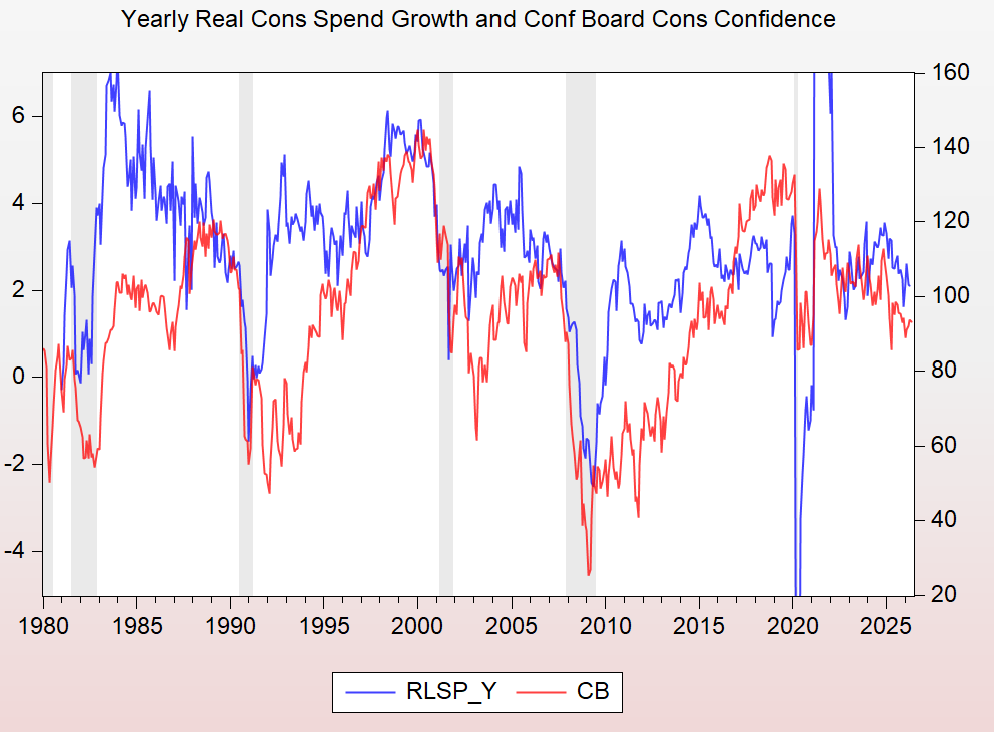

The Conference Board’s consumer confidence measure is plotted below against the same real spending series as above. Historically, it hugs the spending line less closely, and, at least by this measure, it doesn’t show much of a vibes gap (in our paper cited above, we show more of a gap between the actual and predicted CB series). But it does tilt down starting ‘25, in contrast to the macro numbers in my earlier post.

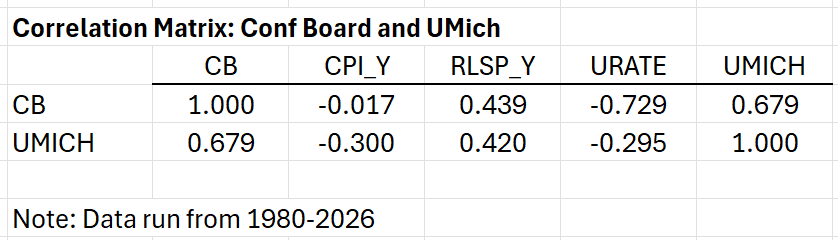

One often-made point is that the questions in the CB survey tend more to evoke people’s views on labor market conditions, which have been uniformly strong over the gap period, while UMich gets more at prices, a particularly salient factor in the vibes gap. The correlation matrix below supports that claim: note the relative correlations for CPI inflation (yearly) and the unemployment rate (URATE). The yearly growth in real spending (RLSP_Y) looks like it does slightly better in CB than UMICH, but that’s just because of the UMICH post-pandemic breakdown. Run the matrix through 2019 and r=0.71 for UMICH and 0.57 for CB.

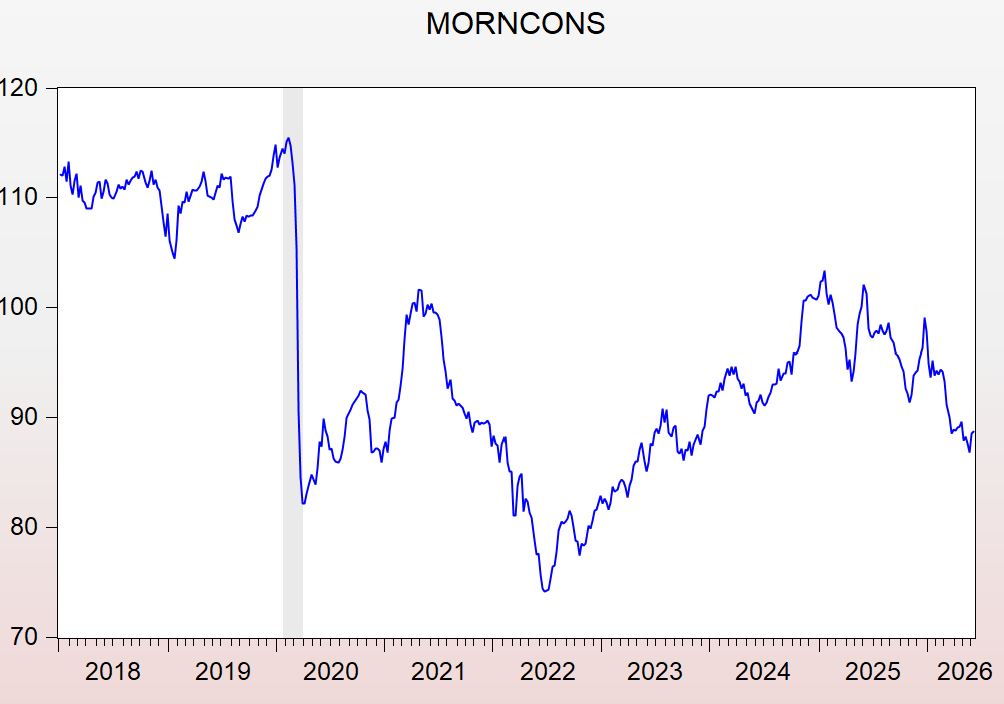

At this point, I should point you towards an interesting, recent paper from the Chicago Fed arguing that UMICH recently reflects a negative bias born of timing and methodology changes (the survey recently shifted to online responses, which was shown to have a negative impact, though the trend stays largely intact). One source cited by this study is a series I’ve long admired, the Morning Consult daily consumer confidence survey. It’s a daily survey with a large, consistent sample that asks some of the same questions as UMich.

Here’s that survey, plotted from its inception in 2018:

As you see, not only does it fail to recover from its pandemic hit—which, ftr, all the macro variables have done—but after climbing ‘22-’24, its trend reverses around ‘25 such that it’s now 23% below its pre-pan peak and 12% below its level from a year ago.

This isn’t an exhaustive data dive, but I’m very confident asserting that the vibes gap is real, measurable, persistent, and a reality of post-pandemic America.

What Explains This Macro-Micro Split

I’ve written about this for decades now, and I’ll be mercifully brief. The most obvious answer is the growth of economic inequality, which has ebbed and flowed in recent decades, but is, of course, considerably higher since the 1980s. Yet, the figures above do not reveal an inequality-inducing vibes gap back then.

Understanding the role of inequality in the gap thus requires both recent developments and a wider aperture. First, I and others have recently focused on the fact that more GDP is flowing to capital than labor income. Labor income is money you make; capital income is money that your money makes for you, and thus is more of function of wealth than paychecks. As the egregious Musk example reveals, tech econ dynamics amplify this trend.

Even as real wages have been growing over the gap period, they’ve been growing more slowly than productivity—arithmetically, that’s the formula for a declining labor share—and most recently, Trump’s awful war-of-choice led to real wage declines, though hopefully those recover as (if??) energy prices normalize.

Then there’s the pandemic-era price level shock, which temporally syncs up closely with the vibes gap. I’ve said it before but it bears repeating here: when I was an economic spokesperson for the Biden admin, I don’t think I did one interview wherein I wasn’t asked about why, if the macro-data were good and inflation was falling (mid-’22 through when Trump retook office), people felt so lousy. I often cited the price level back then. Btw, I also pointed to the Morning Consult data showing how by that measure, people were starting to feel better as inflation retreated, but because it’s private, not-highly-visible data, unlike UMICH or CB—and because it challenged the negative narrative—no one believed me.

That negative narrative was incredibly powerful. It was elevated by the if-it-bleeds-it-leads media, the muscular, Fox-news-driven, Republican propaganda machine and the far more powerful and pervasive force of social media, wherein doom scrolling your grocery receipt got you way more attention than the fact that inflation ticked down or we got a good jobs report.

And then, finally, there’s the relentless, unchecked Trumpian ineptitude. Today’s papers are brimming with expert analysis putting all the correct fine points on the question I posed a few weeks ago: what was this war for? It is shaping up to be a huge, lasting, and deeply costly blunder. At this point, even Rs seem to be recognizing that everything Trump touches turns out wrong, from the reflecting pool, to inflationary tariffs and war, to backing inferior MAGA candidates that should, if there’s any justice (a big if!), crash and burn, hurting their party and given Ds a chance to takeover.

Which poses its own set of challenges that I will shortly get back to. My point of these last two posts is to a) follow the data and show that, while fragilities exist, the macro data are at least pretty good, and b) by almost any measure, people aren’t feeling it.

That’s the diagnosis. Thoughts about the prescription are forthcoming.

PS: Saw Disclosure Day last night. It got great reviews but while I enjoyed the acting, especially Emily Blunt, I found it mostly silly and boring. OTOH, I think the Apple series Maximum Satisfaction Guaranteed is really great, albeit pretty violent.

Well put, sir. Violence, however, per your film recommendation, is - as noted by Tim Snyder’s recent post - - taking us down. The violence of Trump, “ Kegsbreath,” , Miller et al. As the vibes get sharper and their Iran disaster is further revealed they will dig into retaining power. Free elections be dammed. Talk about real violence - coming to small screens in your hands soon!

For other readers who are like me and not "with it", let me save you the internet search.

"BLUF" stands for "bottom line, up front". It seems to have its origins in the military.

(I wonder how many years that term has been in common usage, and I just learned it today.)