Things I Read and Wrote Last Week

Why, if you have >$200bn, must you bend the knee?; our worsening fiscal outlook; fixing finance; why letting in some Chinese EVs is the right long-term play.

If I Were a Rich Man…

Jeff Bezos’ net worth is over $200 billion. Yet he still bends over and kisses the butt of the president and his wife. Explain.

I know, this isn’t that big a mystery. Many of the wealthiest among us never seem to say, “cool, I’ve got enough. From here on in, I’m gonna call it like I see it. I’ll buy a newspaper and build it up to promote factual reporting at a moment when facts are on the run because, you know, Democracy Dies in Darkness.”

Instead, we get “Melania Stuns with Hotness.”

Or, as David Remnick at the New Yorker put it, under the headline “Democracy Dies in Broad Daylight:

Last week—after the Wall Street Journal broke more news about the Trump family’s dodgy crypto-business dealings and before the President shared a racist video of the Obamas depicted as dancing apes—the Amazon entrepreneur Jeff Bezos decided that one of his smaller properties, the Washington Post, has proved such a drag on his two-hundred-and-thirty-billion-dollar fortune that prudence required that he obliterate much of its newsroom.

You could, of course, argue that such wealthy magnates are rationally protecting their fortune by sucking up to an irrational, vindictive and very powerful potential adversary. But that would require them to abandon personal integrity, along with any sense of social responsibility, the idea that one’s responsibility to improve the lives of others is proportional to their wealth. FTR, I’m sure Bezos does some philanthropy, but I’m obviously talking about the way he’s undermined the principles of journalism that for years defined the Washington Post.

I like to think that if I had a fraction of Bezos’ wealth, I would neither bend the knee nor kiss the ring—in fact, I do….and I don’t! But the evidence too often suggests a non-linearity in play here. At some point, the extent of your riches not only fails to insulate you, but, if you lack the integrity to do otherwise, leads you to kiss the royal butt.

Me and Bobby McGee Kogan…and the Fiscal Outlook

As you may know, I’m a policy fellow at the Center For American Progress, and it was my privilege to do a deep dive into the US fiscal outlook with the great Bobby Kogan. Our point is not simply to assign numbers to the fact that the big, bad budget significantly worsened the outlook. It was to analyze the primary source of the demise and to explain why it matters.

Readers know that I believe this last part is by far the most important missing piece of US budget analysis. Barrels of digital ink have been spent bemoaning the outlook, and yet the macro economy continues to trundle along, investment has been pretty robust (if too concentrated), and no skies have fallen.

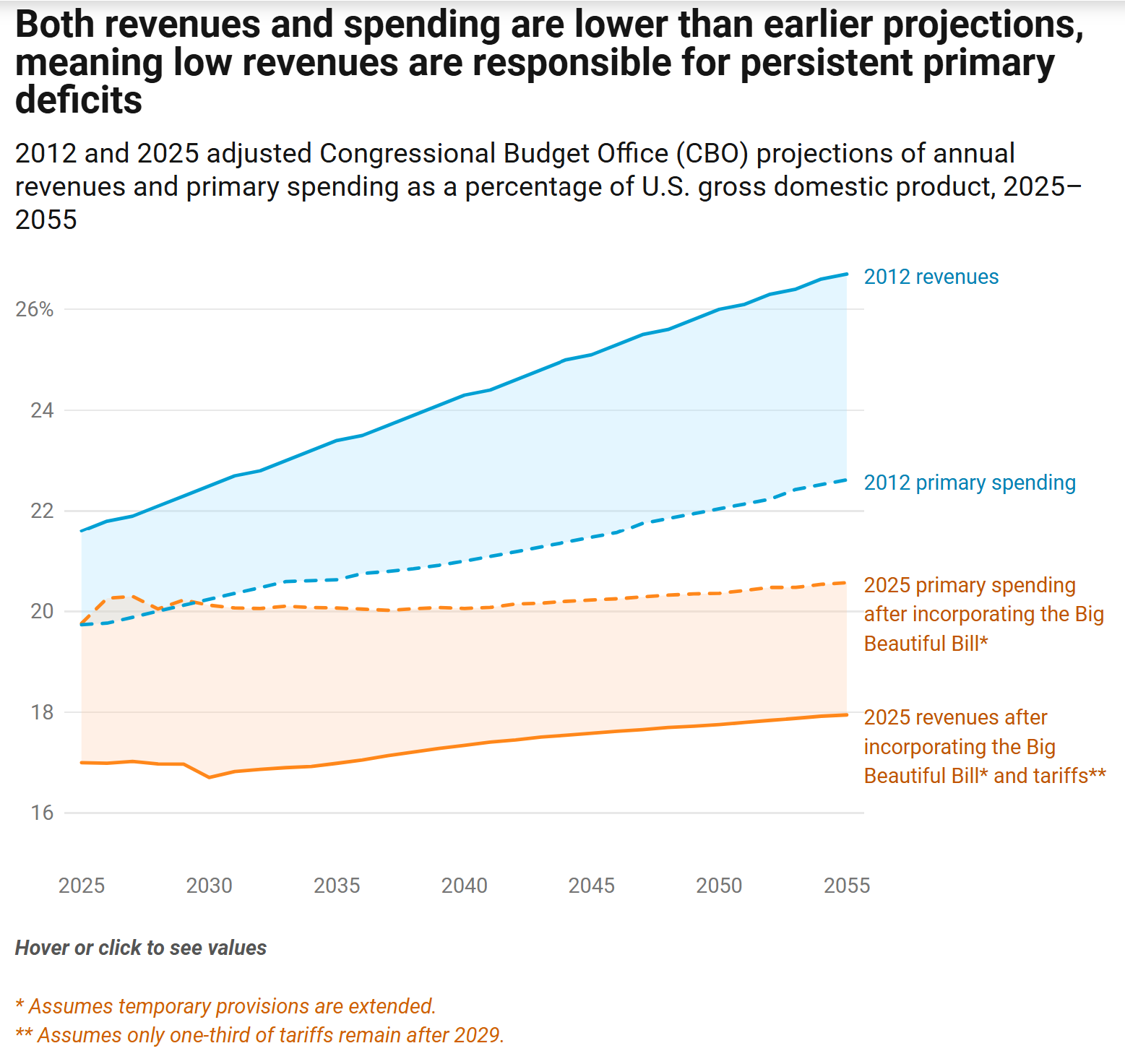

On the source of worsening outlook, we use historical forecasts to show how revenue forecasts have tanked relative to spending forecasts. Here’s the key figure. Compared to forecasts from over a decade ago, spending outside of interest payments is actually on a lower trajectory (we leave out interest not because it isn’t a key forthcoming constraint, but because this is about policy changes driving spending and revs).

The revenue line, however, is 5-8 ppts of GDP lower now than it was then.

I’m happy to put some spending on the table. There’s definitely waste that could be cut without hurting vulnerable Americans (here’s my favorite latest e.g., also a function of the budget bill); who didn’t see this coming?). But there’s just no path outta this mess without new revs.

Why does it matter? I encourage you to read that section. We worry that interest rates are creeping up in ways that have flipped at least yours truly for move dovish to more hawkish. The risk is less a Truss-event than a slow deterioration that raises debt service, crowds out vital spending, and raises the specter not of a “sudden stop" wherein creditors stop lending, but a rise in the risk or term premia on the debt that forces a too-quick reduction in the primary deficit.

…the adjustment that would be needed in order to get back on a more sustainable path would be historically very large, meaning it would require a significant amount of fiscal consolidation that would be extremely challenging to the current federal budget system, which has grown highly unresponsive to debt concerns.

Cass, Baker and the Weight of the Finance Sector

Oren Cass provides a long, detailed, fulsome takedown of the finance sector in this recent NYT oped, but I wanted to lean more into Dean Baker’s review, as he makes two points I’ll amplify.

First, Dean underscores that “finance is essential to the economy.” It’s a simple point but it often gets lost in the mix (Cass starts from the same place, to be clear, but that’s not his point). Every economy, regardless of its structure, needs some function to allocate excess savings or capital to its most productive sources. It could be the gov’t sector (i.e., industrial policy) or it could be a private allocator like the stock and debt markets. But the absence of such a function would take a huge toll on investment, growth, productivity and wealth accumulation (which does not have to be as concentrated as it is here; that’s a big part of the problem).

The problem starts building when you move from this simple, obvious function to the complexities and “rent-seeking” that make up the body of Cass’s oped. To be clear, there have been innovations in finance that don’t fit this mold, like low fee index funds that allow people to participate in the market in ways that were not available decades ago (Dean points out how much is wasted in fees in certain retirement accounts). But what’s most important in these pieces is the steps we should take to—the guardrails we need to erect—to preserve the allocative function while squeezing out the rents.

In this regard, I wanted to tell a story I’m not sure I’ve told before. Dean and I have both long called for a small tax on high-frequency financial transactions, an idea that over the years has become increasingly mainstream (this proposal, from the centrist Brookings Institute, is best-in-class).

The tax would apply to a broad range of assets—including stocks, bonds, and derivatives—in order to raise as much revenue as possible while also preventing potential distortionary effects. Certain assets (such as U.S. government bonds and new equity issuances) would be exempted for efficiency reasons. The tax would start at 2 basis points and be phased in over four years until it reached its target level of 10 basis points. Prior to each annual adjustment, the U.S. Department of the Treasury would consult with other regulatory agencies to monitor the effects of the FTT.

As Dean points out:

Even this small tax will discourage a huge amount of pointless trading, while having no negative impact on companies’ ability to raise money in financial markets. It would also raise a substantial amount of revenue. A tax of this size, with scaled taxes on bonds and derivatives, could raise around $160 billion a year or 0.5 percent of GDP. That’s 60% more than what we spend on food stamps each year. And this money would come almost exclusively at the expense of excessive trading, not out of the pockets of investors.

Well, in the Biden admin, we got very close to adding this proposal to our budgets. All of above facts moved both the many economic and policy analysts involved in crafting such proposals, including the Treasury tax team, who, back in our day, were hard-core experts who carefully scrutinized all proposals, especially those from gadflies like me.

It went all the way to top but got shot down at the last minute, largely due, as far as I could tell, to deep-pocketed market opposition that argued it would hit retirement savings accounts. In fact, those accounts engage in very little of the high-frequency trading that even a 2 bps tax would kill.

But it’s a good e.g. of how hard it will be to make the necessary reforms to lower the “rents,” dial back the scourge of private equity (Dean: “Companies controlled by private equity firms go bankrupt at ten times the rate of other companies”), and move back toward simple, allocative efficiency in this space.

Do the Carney Shuffle and Let In Chinese EVs Under a Low Quota

Finally, in numerous posts, I’ve argued that Canada has the right idea re allowing a small number of their EVs into their country, conditional on transferring their tech knowhow, which is miles beyond ours in this space. Well, the very same Dean B and I wrote a longer piece on this, which he posted and I’m pasting in in its entirety below.

I’m interested in what folks think about this proposal. It is, of course, hard to look around such corners, but Dean and I are pretty convinced that a move like this—if someone has a better idea, we’re all ears—is essential if we want to have a viable auto sector in years to come.

Canada Has This Right: We Too Should Allow in Some Chinese EVs

By Jared Bernstein and Dean Baker

There is no question that, under President Trump, the U.S. has become a far less trustworthy trading partner for Canada. Thus, to diversify its trade portfolio away from the U.S., Canada recently announced an agreement with China, which includes allowing 49,000 Chinese electric vehicles to enter Canada at a tariff of 6.1% instead of the prevailing rate of 100%.

Though we realize that such a move would be anathema to the Trump administration, we would be smart to do the same thing here. Doing so would significantly hasten the shift to electric vehicles, yielding both economic and environmental benefits. It would increase consumer demand for quality, affordable EVs. If done the way we articulate below, it would jumpstart the heretofore stagnant U.S. EV industry, and in so doing, give our auto sector a fighting chance to not only survive, but to flourish.

Our argument starts from the recognition that Chinese EVs are high-quality, low-cost vehicles. Some sell for as little as $8,000 in China. The lowest cost cars have ranges of close to 200 miles between charges, but more expensive models have ranges of between 300-400 miles, and the most expensive ones can travel over 500 miles on a single charge.

Many of their cars can be charged in less than 7 minutes and the fastest can be charged in 5 minutes, close to the time it takes to fill a gas tank. These vehicles have gotten outstanding reviews for their handling and comfort. As Ford CEO Jim Farley recently said about his Chinese-made Xiaomi SU7, “I’ve been driving it for six months now, and I don’t want to give it up.”

To be sure, we wouldn’t be having this conversation but for China’s deep subsidies for EV and battery production. While estimates vary on the size of the subsidies, they were likely over $200 billion for the decade where China was building up its industry. The government has withdrawn many of these subsidies as survival of fittest among many subsidized competitors has played out, but they’re ready to jump back in if needed.

We do not advocate anything like that level of subsidies, though we would at least initially reinstate some of the Biden-era tax credits that were contributing to consumer demand for domestically produced EVs before Trump got rid of them. However, we should go into this project with the realization that EVs sold here, and especially EVs built here, will not be as cheap the ones in China.

But the goal of this policy is not to cut autoworkers’ wages or union jobs. To the contrary, it is to boost both, which is why the relatively low quota is key to this plan. By just letting in enough Chinese EVs such that only a small number of consumers can buy them, we’re confident, again based on quality and cost, that demand will quickly climb. This will signal domestic producers to get into the EV game in a way they’ve thus far avoided.

One reason for their reluctance to jump in is that they simply don’t have the production acumen that the heavily subsidized Chinese builders have acquired. Therefore, another essential part of the plan is to insist on technology transfer.

This transfer can take two forms. First, we can require that a certain percent of the cars sold here are made here, with that percentage rising over time. And to give the Chinese firms more incentive in this direction, their quota of sales can increase as they produce more cars here. The other form is for Chinese companies to directly work with the established U.S. automakers. If Ford or GM jointly produce vehicles with a Chinese manufacturer, it can be a basis for increasing their quotas further.

This begs the question of whether the Chinese would agree to such an arrangement. If not, then no deal. We must protect our domestic industry. But we believe China would jump at the chance to invest directly in U.S. EV and battery production, and, in fact, would recognize hardball industrial policy of the sort we’re recommending as part of their own manufacturing playbook. Also, China has made similar deals with Thailand and Brazil, so the country is clearly open to such arrangements.

We are not naïve to the security concerns invoked by working with China on this project. But as the economist Noah Smith recent pointed out, cybersecurity experts are making progress on this challenge and the fact is that “detecting and countering Chinese espionage and sabotage efforts will be important whether we buy Chinese cars or not, since China already makes so many of our electronic devices.”

But regardless of how much we fear China, we have to look at the ascendency of EVs clear eyes. More than 60 percent of the cars sold in China, which has a much larger market than us, are electric. In Europe, sales of pure EVs now outnumber sales of gas or diesel-fuel cars. EV sales are also growing rapidly in large developing countries like Turkey and Brazil. Here in the U.S., our EVs sales were last seen stuck at 8 percent.

All signs suggest that within the next decade, the overwhelming majority of the cars sold will be electric, especially outside the U.S. The question is do we want the U.S. auto industry to be an active player in that market. If not, we can follow Trump’s lead to build walls around the country, leaving American drivers with little choice other than to buy more expensive, polluting, gas-fueled vehicles (unless they want to do their car shopping up in Canada). Or will we try to get in the game and grab market share by producing high-quality, affordable EVs?

Even if you choose to ignore the impact on global warming, making this play for EVs and batteries is essential for maintaining our auto sector, our industrial base, our global competitiveness, and the jobs that come with all the above. Enacting a quota on Chinese EVs while building out domestic production is a great way to get started.

It took a visit to Shanghai for me to understand how far ahead China has become with EVs. Excluding their technology would be foolish. Think what Honda Accords did for American vehicle quality.

We have a surfeit of scoundrels. I used to enjoy reading gardening and art books and novels. Now my book list is overloaded with economics, political theory and history. Capitalism and its Critics is one of many in this genre. I hope I can forgo Wealth of Nations and The Theory of Moral Sentiments, not because they’re not worth reading, but because I fear I will never crack another gardening book. This came courtesy of David Runciman and his guest on the Past, Present, Future podcast and their discussion of the philosophy of Adam Smith. I think it goes a long way to explaining Jeff Bezos and all the other scoundrels too numerous to name.

“This disposition to admire, and almost to worship, the rich and the powerful, and to despise, or, at least, to neglect persons of poor and mean condition, though necessary both to establish and to maintain the distinction of ranks and the order of society, is, at the same time, the great and most universal cause of the corruption of our moral sentiments. That wealth and greatness are often regarded with the respect and admiration which are due only to wisdom and virtue; and that the contempt, of which vice and folly are the only proper objects, is often most unjustly bestowed upon poverty and weakness, has been the complaint of moralists in all ages.”

It’s not just bad for our moral sentiments. It’s bad for our democracy and our economy. From what I gathered Adam Smith thought so too. He wasn’t just the invisible hand guy.