Too Much Wealth Concentration, Not Enough Revenues: I've Got An Idea...

Tax wealth.

Last week was about many things, from the amazing Knicks victory, to the lovely spectacle of Trump’s name coming off of the Kennedy Center, to the pumped up SpaceX IPO.

Re the Knicks, what a series! I’ve been following basketball for decades and I’ve never seen anything like it and doubt I ever will again. One could easily pull out a favorite, decisive moment, but I’ll remember waiting through 3/4 of the game for the Brunson burner to get lit, as it invariably was in Q4. I could go on, but if anyone needs a reminder that fighting back from adversity is the only viable option, go watch the tapes.

Re Trump’s name coming off the Kennedy Center, I’ll just note that a) coming a few days before his 80’th birthday, I couldn’t think of a better present, and b) the appearance of this lovely rainbow during the removal was surely nature’s way of showing whose side she’s on. It’s a symbolic victory—it doesn’t replace lost SNAP or health benefits—but it’s a victory nevertheless, and it’s consistent with the decline of the Trump project about which I recently held forth.

Okay, that’s enough winning for now. Back to econ.

The other big news of the week was the SpaceX IPO, the one that pushed the newly-public company’s valuation to over $2 trillion and Musk’s wealth to over $1 trillion. That’s paper wealth, of course, and if those of us who see bubbles and overvaluations in this space are even partially correct, it could deflate. But the broader point is that, as Ben Casselman put it the other day:

The wage-falling part is probably—dare I say it—transitory, as it is largely a function of the inflationary gas-price spike. Not at all to discount that fact, one I’ve highlighted in many places, and just the latest e.g. of Trump pushing hard in the wrong direction on affordability. But my point is that the “wealth surging” part and the “workers facing higher prices” part and the “AI fears” points are all increasingly and lastingly embedded in our current political economy.

But even if—I’d say when—real wages start rising again, their pace will likely remain below the rate necessary to prevent labor’s share of national income from continuing to contract (for data nerds, if real compensation lags productivity growth, labor share falls; over the last decade, productivity growth has been 2x real comp growth—22% vs. 11%).

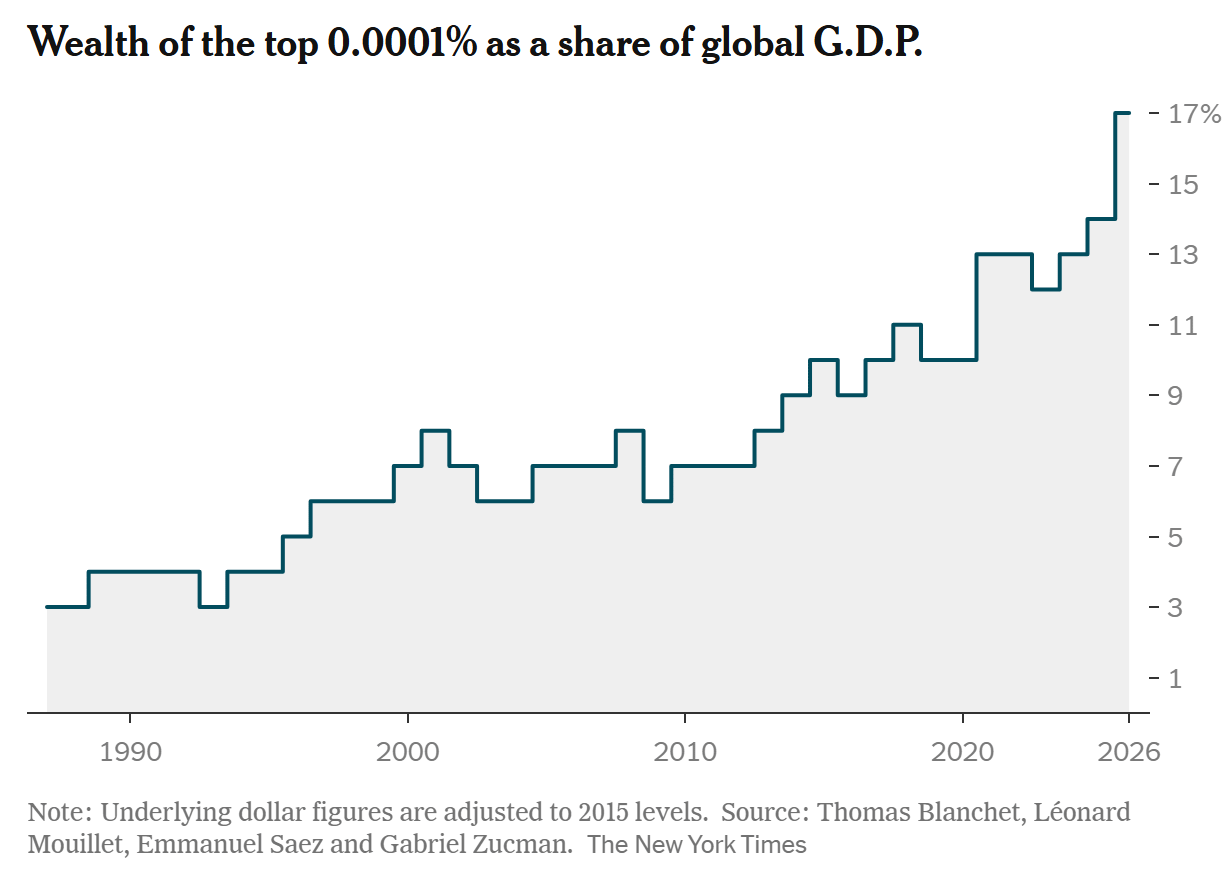

It’s easy to find evidence of the extent and the increase in wealth concentration. There’s the Zucman et al global dimension (see figure below), the Federal Reserve accounts (bottom 50% equity holdings: 1%; top 10% holdings: 87%), the labor vs. capital share data I recently featured. While all of these data have nuances that are debated, I’m not aware of arguments accurately discrediting the trend.

And, if data’s not your thing, just look at the billionaires crowding the stage at Trump’s second inauguration. I mean, Musk fatefully—and incompetently—held the keys to federal gov’t for awhile. Given that money buys political power more aggressively in this relative to any other advanced economy, increased wealth concentration means increased political power.

All of that is well known. But let’s connect it to another spate of articles over the past week about a related problem: the forthcoming shortfall in the Social Security and Medicare accounts. My go-to analyst on this is CBPP’s Kathleen Romig, who wrote that “The 2026 annual report of the Social Security trustees released today shows a worsening outlook for the program’s finances, driven in part by Trump Administration policies.”

Romig points out that the Rs budget bill worsened the Social Security’s fiscal outlook but that the trustees rosy—relative to what Trump/Miller have wrought in this space—assumptions re immigration likely bias up their predictions of Social Security’s fiscal health: “Accounting for the full effects of the Trump Administration’s immigration restrictions and mass detention and deportations would make the picture even worse because immigrant workers strengthen Social Security’s finances by contributing to the trust fund through payroll taxes.”

Moreover, readers know my recent fiscal work, often with Bobby Kogan, has stressed the need for not just more tax revenues but for reconnecting the tax system to how the economy has evolved. At this point, revenue collection is fatally disconnected in three consequential ways. First, the incomparable Natasha Sarin tells me that the tax gap right now is around $700 billion per year, over 2% of GDP. This is the amount of the annual shadow tax cut we provide for wealth tax evaders by underfunding IRS enforcement.

Second, as Bobby and I show, the one-way downward ratchet of tax policy since 2000 has broken the connection between economic growth and revenue flows.

Third—the point of this post—an ever increasing share of resources are escaping taxation because we don’t tax wealth. This must change. That’s a lot easier to say than to do, but ask yourself how the Knicks kept coming back from crushing deficits, which was by not taking “no” for an answer.

Moreover, the context is changing, as captured by the Casselman piece. Consider the juxtaposition of billionaires and a trillionaire against a backdrop of unaffordability, or the AI-moguls arguing that the tech that’s making them modern Midases will dis-employ huge shares of the rest of us (which, for the record, is but one among many possible outcomes). I think we can safely conclude that there are large, growing, majority shares of Americans who are pissed about all the above.

That energy can and should be politically harnessed to re-introduce fairness back into our tax system and that implies taxing more wealth and wealth-adjacent income sources (it also implies disallowing billionaires to buy politicians, but that’s a different—and extremely important—post). In this regard, I was struck by the comments of the (reasonable) Republican economist Glenn Hubbard in the Casselman piece: “Congress should consider ways to tax billionaires more effectively, he said, and to ensure that the wealthy don’t exert undue influence on the political system.”

I don’t know if Hubbard was saying we need to tax wealth, though that is implicit if we want to “tax billionaires more effectively.” At least it calls for ending step-up basis, taxing capital gains as regular income, moving from an estate to an inheritance tax, adding a financial transaction tax, and closing loopholes that allow tax avoidance through pass-through income. (I won’t take the time right now to explicate these ideas but they’ve all been around for awhile and I’m sure AI can explain them well.)

But I definitely wouldn’t and won’t stop there. In the Biden years, we developed a tax on unrealized capital gains, and there’s a billionaires’ surcharge tax on the ballot in California. IOW, ideas for taxing the assets of the wealthy are out there and I expect them to proliferate.

Last point for now. If your response to wealth taxation is “you know this SCOTUS won’t allow it,” I’d offer two responses. First, you’re probably right. Second, no one, myself included, thought the Knicks could erase a 29-point deficit in game four, and yet…

It is flat-out unacceptable that a few unelected politicians in black robes get to decide that government must be starved of resources, leading critical retirement and health benefits to be cut because of their interpretation of what can and can’t be taxed. If it means ending the filibuster to change the rules, absolutely. If that means adding more and better judges to the SCOTUS, so be it. Based on reproductive rights alone, such a move is likely necessary.

I recognize that this is a radical solution and I don’t go there lightly. But the extent of these economic imbalances, which I fear will only grow, militate a firm rejection of the status quo, which is working far too poorly for far too many while bestowing unprecedented rewards on far too few.

Excellent essay.

We should remember that Congress is a co-equal branch of federal government. They can overrule the Supreme Court and the Executive by clarifying legislation. It's not easy, but it is well within the realm of possibility.

Just like overcoming 29-point deficit. Difficult but possible.

Thanks, Jared! Two good news vs one bad which will not last long! Musk bubble will explode soon enough...