Updating our AI Bubble Call

New data, including IPOs and even deeper capital investments, reinforce our view that AI is likely the latest asset bubble.

Back in October, we published an oped in the NY Times arguing that the lofty valuations of AI stocks and companies meant we were more-likely-than-not in an asset-price bubble. In this post, we revisit and re-evaluate our case.

Our fundamental take hasn’t changed. AI still looks bubbly to us, even though since we wrote our piece, the stock market has gone up 10 percent. While AI and related stocks (e.g., memory chips) have been somewhat volatile, they too are up roughly 25%. If there is a bubble, it’s still inflating. But the gap between AI’s outsized capital spending, its valuations (which are coming into clearer focus as private AI firms go public) on one side, and profitability and investor returns on the other, is even wider than when we first worried about this.

To be sure, we didn’t predict that the bubble would pop imminently and were clear that neither we nor anybody else can time such things. But several developments have occurred in recent months that are relevant to our view that the AI bubble is alive and well.

One such development is that private AI startups are going public. Most notably, earlier last month Elon Musk’s SpaceX performed the largest Initial Public Offering (IPO) on record, while the other AI giants Anthropic and OpenAI have filed for IPOs to take place this fall or early next year.

This maps onto our bubble watch in various ways. First, as Craig Coben and David Erickson over at FT Alphaville have pointed out, previous exposure to the AI trade was partially limited by the fact that three of the most important players (xAI, Anthropic, and OpenAI) have remained private. Thus, exposure to these companies was gained either by being among the selected few who could invest during a private fundraising round, or indirectly though buying stocks like Microsoft and Amazon, which are invested in both OpenAI and Anthropic (as well as in their own AI models).

Once they’re public, however, those who decide to wish upon an AI star can do so more directly, yielding more public information about returns than was previously available. Investors will have a clearer line of vision into how much money the firms are making…or losing. In terms of bubble impacts, the opaqueness of losing billions in private may prove easier to recover from than losing billions in public.

Perhaps the most important impact of the AI IPOs is that it will now be easier for investors to not only buy the stocks, but also to sell them. Six months after going public, firms face substantial pressure because early employees and institutional investors who were rewarded shares in an IPO are subject to “lockup” restrictions that prevent them from cashing out their shares for six months. But once these lockups expire, investors are free to sell their shares, and they often do. Indeed, one paper found that one reason for the bursting of the dot-com bubble was tied to the expiration of lockups. Additionally, once stocks are publicly traded, they can be shorted by pessimists, which can drive down prices.

In other words, greater public exposure means more information about profits, losses, share prices, volatility, all factors that will feed into investors’ bubble assessments.

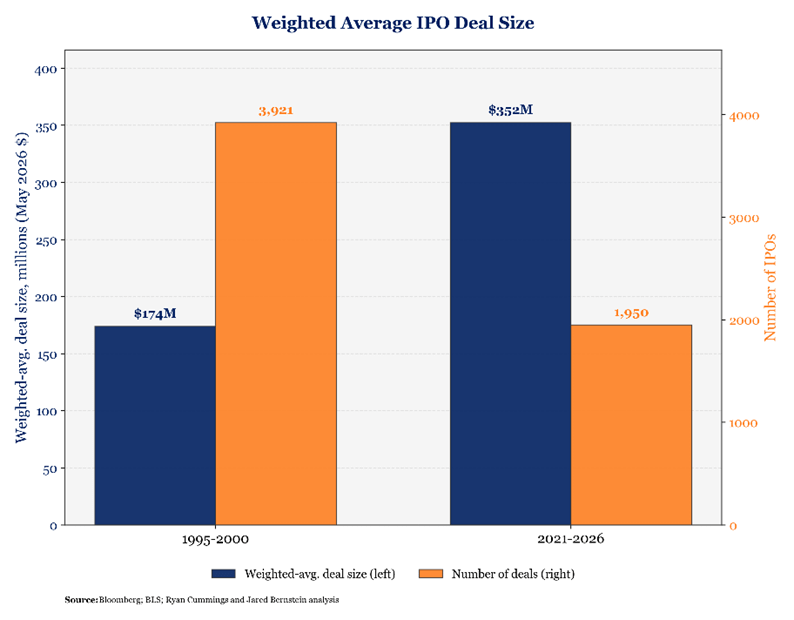

Of course, more startups going public doesn’t mean the end is nigh. There’s no obvious long-term correlation between the number of firms going public and market shocks (or bubble implosions) one way or the other. Moreover, because of the historically large, fixed costs associated with building AI models, at least in the US (Chinese models apparently require less capex), there may be fewer firms going public, but the ones that do go public have much higher valuations. When we compare the five-year period from 1995-2000 to the latest five-year period, we find that there’s been about half as many IPOs, but those IPOs are roughly twice as large on average (see figure). This matters in terms of our bubble assessment because it means we’re much less likely to see small firms with no credible business model rapidly go public and then go bust faster than you can say Pets.com. Instead, it’s more likely that there will be a long run-up to “unicorns” going public, while their valuations will be litigated by financial markets over a longer period of time.

Of course, what’s been driving our AI bubble call hasn’t been firms that have yet to go public, but the ones that have. For those firms, a core part of our bubble case has been that the time gap between huge investments and investor returns will eventually try investors’ patience, leading to potentially pervasive selloffs and sharp wealth losses. These concerns remain as germane as ever.

We see no signs of the firms most committed to the AI buildout—so called “hyperscalers”—slowing down on their capex spending spree. To the contrary, the graph below from Goldman Sachs Research shows that hyperscalers are on track to spend more than $750 billion this year and nearly $1 trillion in capex next year.

To put this into context, this capex spending has resulted in technology investment composing nearly five percent of GDP—a share higher than at the peak of the dot-com bubble (chart also from Goldman).

Is this sustainable? We think not, in large part because these investments eventually must start generating positive cash flows, i.e., profits. So far, the AI buildout has largely been financed by firms who have existing profitable businesses (such as ads with Google, ecommerce for Amazon, etc) that have allowed them to direct those profits to the AI buildout. As the chart below from Nomura demonstrates, this has resulted in hyperscalers using their cashflow not to pay out shareholders (through dividends) but spending instead on their AI buildout.

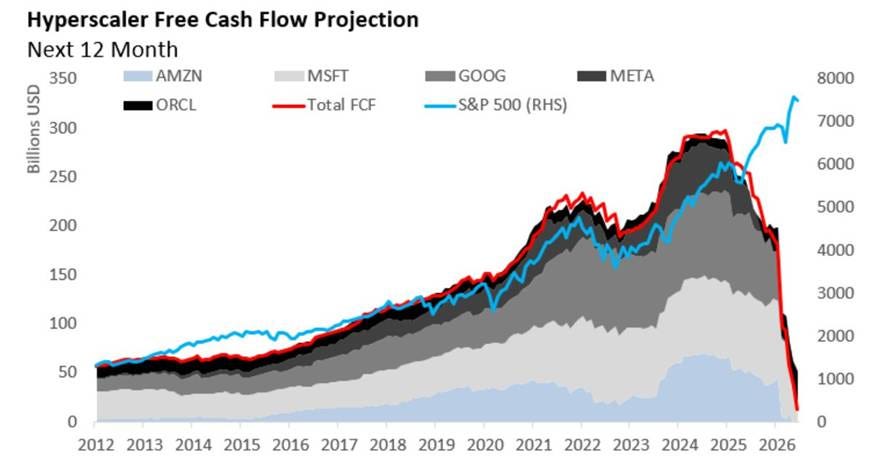

And while this wasn’t the case when we wrote our oped, the end of the figure shows that many hyperscalers are now exhausting their internal cash flows.

The aggressive push into AI is leaving these tech giants with significantly less cash. Wall Street forecasts show the combined free cash flow of Amazon, Alphabet, Microsoft, and Meta could drop to around $4 billion in the third quarter. This marks a dip from the quarterly average of $45 billion since the COVID-19 pandemic.

Since they’re now spending more cash than they are earning, the hyperscalers are turning to debt financing their AI capex. Bloomberg reports that “credit markets have been flooded with AI-linked debt sales, [totaling] about $335 billion globally, or more than twice the levels seen in 2025…The rapid increase in supply has fueled concerns of investor fatigue, with Amazon’s offering prompting outstanding tech bonds to weaken in the secondary market.”

The key words, bubble-wise, are “investor fatigue.” If AI continues to be unprofitable over the next 5-7 years (the window in which many of these investments are amortized over), then valuations will adjust downward, as investors will recognize that the amount of cash available to flow back to them in the future is now lower because of wasted or unrealistically (in ROI terms) large investments. At that point, this probably-a-bubble will deflate.

To be clear, none of that should be taken to imply that AI won’t be transformative to life, work, productivity, and growth. Many past bubbles did a lot of damage before the underlying assets proved to be of great economic value (e.g., railroads, the internet; not e.g., the housing bubble).

We’ll report on such developments, as well as their absence. Though if we’re right and the AI bubble bursts, you won’t need us to tell you about it.

| A guest post by

|

Thank you, Jared and Ryan, for your insightful article and clarifications. My main takeaway is that the timing of the AI bubble is crucial. How will it impact ordinary people like us who are just trying to get by in this economy? Will this future AI bubble affect all of us as badly as the housing bubble did? I have a strong dislike and distrust for Musk and others like him, so it's reassuring to know that you'll be keeping an eye on the AI bubble they are creating!

Thank you for this. A very persuasive case for an AI bubble! I have just one even more pessimistic quibble:

You argue that having half the IPOs investing twice as much is anti-bubble vis-a-vis the dot-com bubble, but isn’t the opposite just as possible? I don’t have any data, but theoretically speaking, isn’t a far less diverse portfolio concentrated in far fewer firms even riskier than the dot-com basket of firms? This time there won’t be any pets.coms to absorb the losses. Just a thought…