War Notes: DoD Wants $200Bn, Post-Shock Oil, Markets Over-listen to Trump

We must always support our troops, but not one more war dollar should flow until critical questions get answered.

A few scattered notes on the war and its econ impact though I shortly plan to get back to policy. A number of folks responded, quite reasonably, to my post yesterday (about just how costly this admin is to America) by nudging me to get back to the policy agenda upon which a new coalition could be built. It’s a great point. Speaking of opportunity costs, if you spend all your time obsessing about the damage of the current regime, you have that much less time to plan for a much better regime. And yes, I’m talking about “regime change.”

A $200 billion supplemental to support the war?! Not so fast.

The NYT reports:

The Pentagon has asked for $200 billion in funding for the war in Iran, according to a military official and an administration official, a significant sum adding to the costs of an already divisive campaign.

I suspect everyone reading this agrees with me that we always want our brave men and women in the military to have the resources they need, especially when we send them into harm’s way.

But there should never be any blank checks in government and those requesting this supplemental must answer some important questions before one more dollar flows their way.

First, the Defense Dept’s annual budget is about $900bn and on top of that, the DoD got another $153bn from the Rs budget bill. As CAP’s Bobby Kogan and Damian Murphy recently put it, “the White House seems poised to request more money for weapons for which they already have tens of billions of unused dollars.”

—So, question 1: why is existing funding insufficient?

It’s an obvious question that I’ve never seen anywhere close to answered. One reason for that surely relates to the fact that the Pentagon failed its last eight audits in a row. I think most taxpayers would agree that before an institution gets more money, they need to reliably tell you what they’re already spending.

—Question 2: What’s the goal of the conflict and how does another $200 billion get us there? Once that goal or goals are clearly articulated, what metrics inform us of how we’re doing in hitting those goals? I’ve heard reports of the thousands of targets hit, but while Iran’s forces are clearly degraded, they’re demonstrably still able to counterattack and disrupt commerce, often with mines, drones, and speedboats. So, when I say “goals,” I’m talking about metrics beyond “targets hit.”

—Question 3: What’s the exit strategy? Trump, who is unilaterally calling the shots, says he’ll know when to end the war as he’ll “feel it in my bones.” This means it’s entirely possible—perhaps likely—that he decides the political hits he and his party are taking from the war’s impacts on American consumers are too much and declares victory. Of course, if Israel and Iran disagree, the conflict will persist, the region will remain volatile, transit through the Strait still dangerous, and so on. Without clear guidance on the endgame, more resources are not justified.

The reporting is that enough members of Congress are skeptical of this “supp” that its fate is in question. That’s as it should be, until questions like these are convincingly answered.

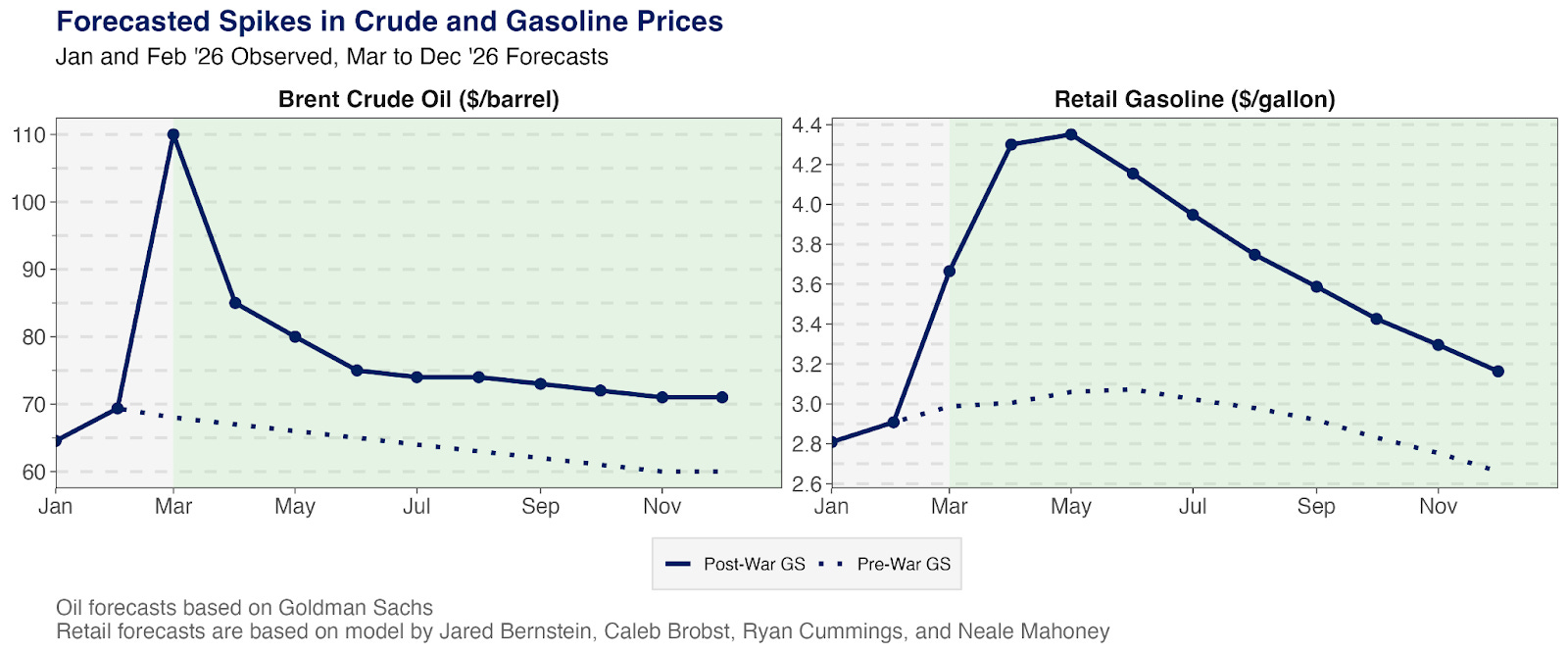

Once the war is over, will oil bounce back and prices fall?

Understandably, I’ve been getting this question a lot, including on Ari Melber’s show last night. I’ve talk a lot about rockets and feathers—how, even as the oil price could (not a slam dunk, as I’ll show) come down quickly, the gas price tends to unwind more slowly. Here’s a picture of that from our recent forecast:

But the bigger issue here must be gleaned from the history of oil shocks, including disruptions from wars. As GS Researchers wrote in an historical review, “Looking at the 5 prior largest supply shocks of the past 50 years, we estimate an average hit to production of 42% after 4 years, often due to infrastructure damage and low investment.”

The key point is, of course, infrastructure damage, which has been common in the current war, as both sides have damaged oil and gas fields, as well as refineries. This suggests a slower recovery. Also, as in the “what’s-the-endgame” discussion above, if we pull out and Israel and Iran keep fighting, energy transit through the region will likely still be constrained.

This is relevant because in numerous past shocks, some suppliers, especially the Saudis and the UAE, have increased production to offset the supply shortfall. But, if so, they’d still need to move oil through the region.

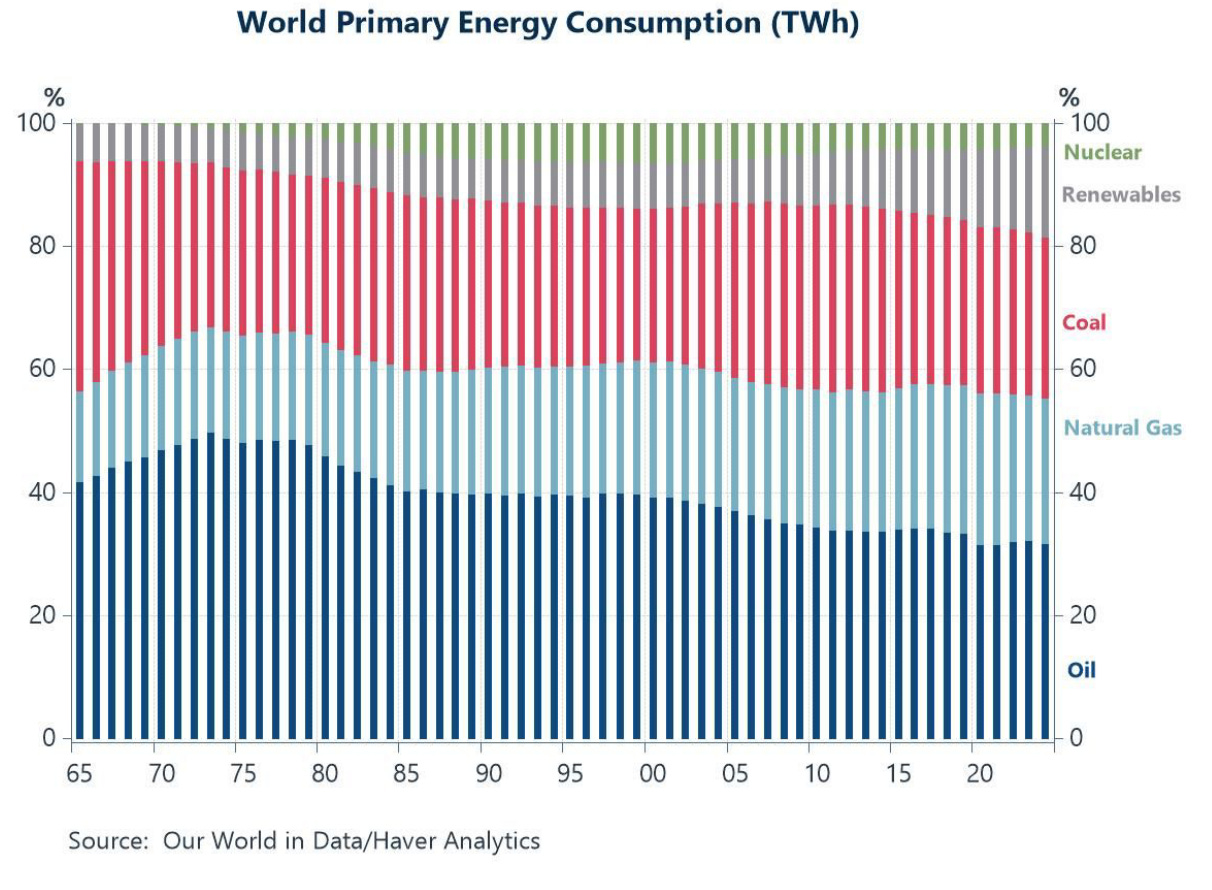

BTW, I wanted to share this figure. Some folks have expressed surprise to me that the world is still so dependent on fossil fuels that a partial disruption in their supply can rattle the global economy. After all, doesn’t the U.S. use oil much more efficiently than ever (it does) and aren’t renewables a much bigger part of the global energy supply?

Not so much. As the figure shows, renewables and nuclear power account for just 20% of global energy consumption (the U.S. renewable share is just north of 20%). Eyeball that chart for a moment and you’ll get why where we’re we are. And the Trump admin’s deep hostility to renewable sources is making us even more dependent on the other sources.

Why would anyone, including the Markets, listen to Trump?

Axios puts it this way: “Stocks stumble in the morning and mostly recover by the end of the day after President Donald Trump says something that's viewed as reassuring about the Iran war.”

Why would they put their trust, not to mention their and their clients’ money, in a president who just blathers on in a polluted stream of consciousness? In part because they believe there’s a Trump “put,” which I referenced above. If he takes enough incoming political pressure on the costs of the war, he’ll end it (though, again as noted, that doesn’t mean prices quickly bounce back to where they were).

But an equal if not larger part of this is just market psychology. Here’s what they’re saying, from Axios:

“Albeit minor, this is the first sign of de-escalation that may lead to others in the future,” Jim Caron, chief investment officer at Morgan Stanley Investment Management, tells Axios.

“It’s too soon to say for sure, but if there is willingness for both sides to draw bright lines around what can and cannot be attacked is a new data point for the market to assess.”

“Any little positive thing can really generate a big move in the market,” says Jose Torres, senior economist at Interactive Brokers.

“Traders are waiting for the Trump put to kick in. This is the TACO trade. Trump always chickens out.”

Investors are just so anxious to get back to calmer markets, which were at least flat this year before the war, that they’ll listen with underserved credulity to Trump, who has long enjoyed moving markets around like a puppet on a string. Thus, if you value your sanity, this would be a good time to take a break from market-watching.

Yet they weren't able to find $70-90B for enhanced ACA subsidies?

One of the lesser discussed functions of National Security is the physical health of the nation.

It’s reasonable to speculate about potential self-dealing grifts associated with DoD’s request (“never let a good crisis go to waste”).

It’s reasonable to demand precise, binding accountability for each additional appropriated USD.