What the Fed Said

There are, apparently, many ways to say "we're on hold for now."

Listening to and understanding the Federal Reserve’s position on monetary policy right now seems pretty straightforward. Before they start cutting rates to get the interest rate they control back down to more normal levels, they need to better understand the tariffs’ impact on inflation.

You might think there’s not a lot more to add, but there’s a huge market/media complex that pours over these entrails. Did you know that in yesterday’s press conference, Fed Chair Powell said that monetary policy is in a “good place” a mere four times, compared to 12 times at the prior meeting in May? Is he really saying that monetary policy is only in one-third as good a place? (That’s snark, ftr.)

Here are a few things I found interesting, all of which, except one, were raised many times over by lots of different sources. Again, there’s just not a lot to see here folks. Move along, please.

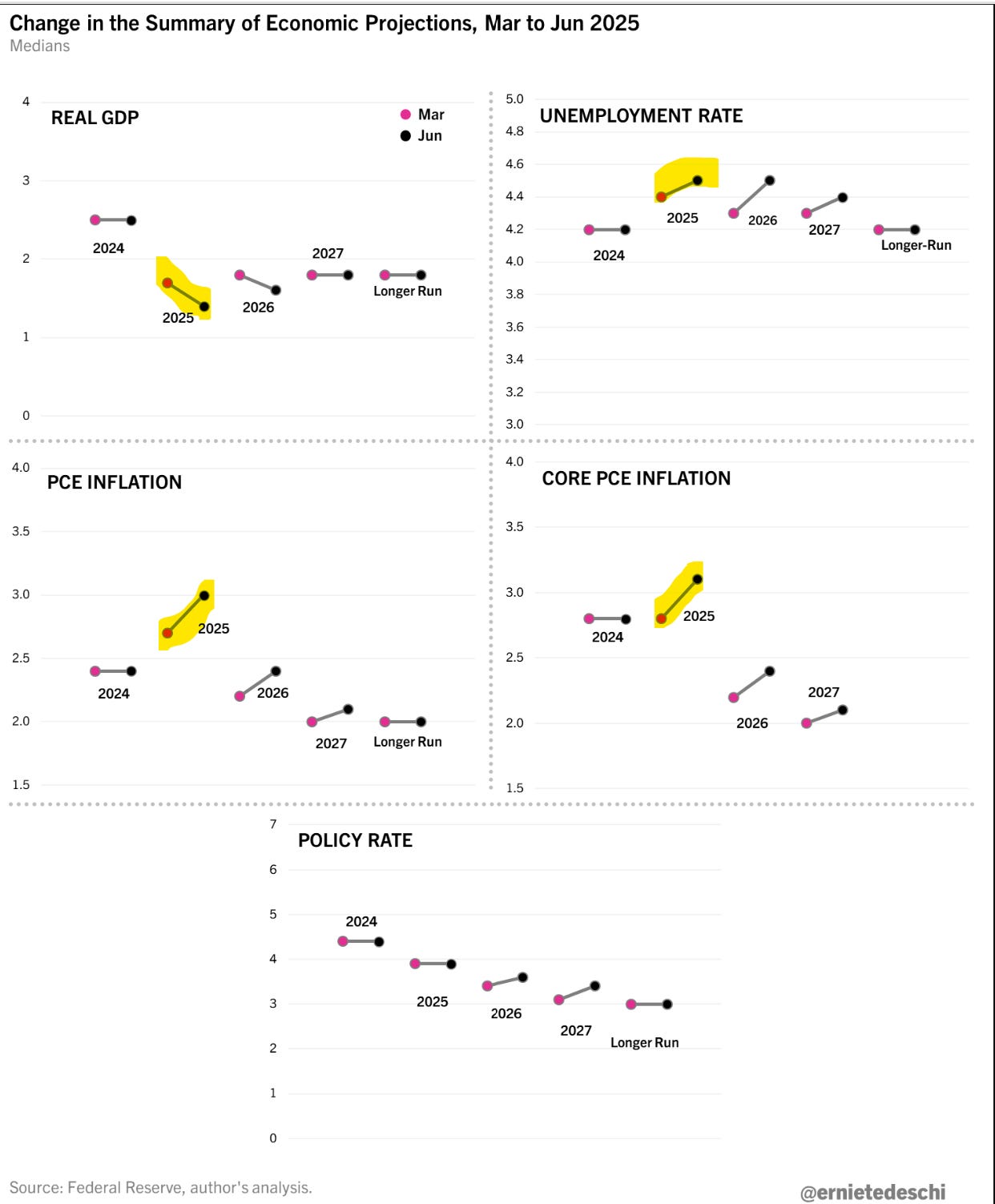

—I think Ernie’s figure here is a great way to visually summarize where the Fed interest-rate-setting committee thinks the big variables are headed, and how that’s changed from their previous forecast (my highlights). They’re clearly forecasting tariff-induced stagflation—slower growth, higher inflation—meaning they’re in the same camp as many of us: tariff-induced inflation is likely to shortly be upon us.

—I liked the way Powell explained these tariff mechanics in one of his responses during the presser. We know tariff revenues are up sharply, 3x from a few months ago, as U.S. importers were paying $8bn a month to customs agents and are now paying $24bn. That’s gotta go somewhere:

…the pass-through of tariffs to consumer price inflation is a whole process that's very uncertain. As you know, there are many parties in that chain. There's the manufacturer, exporter, importer, retailer, and consumer. And each one of those is going to be trying not to be the one to pay for the tariff. But together they will all pay. Or maybe one party will pay it all. But that process is very hard to predict. And we haven't been through a situation like this. And I think we have to be humble about our ability to forecast it. So that's why we need to see some actual data to make better decisions. We'd like to get some more data.

The bit about “each one trying not to pay for the tariff” is a good way of making the classic tax-incidence point: the party that pays the tax is the one with the most inelastic demand for the taxed item. They’ve gotta have it so they’ll swallow the tax. But that’s a long chain of folks in play here, and as I stressed in a recent post, there are dynamic factors in play: firms that boosted their profit margins post-pandemic might cut into that buffer before passing the tariffs forward to consumers. But they won’t do so forever.

—Here’s the one thing I didn’t hear anyone say yesterday, though I might have missed it. I know this sounds partisan, and I’m fully capable of partisanship, but I don’t mean it that way. If Harris were president, we’d be getting rate cuts.

Why is that even worth mentioning? Because it strikes at the heart of the Trump’s false-flag project, one he applies in every policy area: create a phony crisis; declare that despite norms and laws, you must invoke authoritarian privilege to solve that crisis; take unilateral steps to do so.

In this case, the crisis was grew out of the extremely weird claim that countries from which we willingly buy things are always and everywhere ripping us off. Thus, we get a trade war that has jammed the Fed into their current wait-and-see mode.

The fact that Powell challenges Trump authoritarian project in this monetary-policy case in clearly rattling the president, who blathers on about how he (Trump) should be Fed chair. Here’s a tweet from me yesterday on this point, one in which Trump inadvertently pays Powell a big compliment:

Anyway, sometimes it’s important to step back and recognize that it didn’t have to be this way.

—I’ve long wondered if all this information-sharing from the Fed in cases where there’s no policy change adds value to the markets’ and the public’s understanding of current monetary policy. I think it does, and as someone who tries to explain complex things to non-economists, I’m in awe of Powell’s skill in that space. But there’s an unavoidable tendency to over-torque on the dots (committee members’ thoughts about where rates are headed) and forecasts. Powell practically waved folks off of doing so yesterday:

These individual forecasts are always subject to uncertainty and as I have noted, uncertainty is unusually elevated. And, of course, these projections are not a committee plan or decision…

…I think, again, people write down their rate paths and they do not have a really high conviction that this is exactly what’s going to happen over the next two years.

Anyway, we can keep talking about this or go outside and watch the grass grow. I’m gonna do the latter.

"as I have noted, uncertainty is unusually elevated"

This statement is full of dry British wit. A dissertation could be written on the causes of that elevated uncertainty.

When Powell's term ends next year, Trump will stop musing and appoint himself chairman of the Fed. That would, of course, be challenged in the courts. But, as the various appeals move toward the supreme court, Trump would have a field day doing to the delicate balance between inflation and employment rates what he has already done to the executive branch.