When (Budget) Doves Cry

JB in the NYT re r and g (r=interest rate; g=growth rate)

I’ve got an oped in the Times today summarizing a new policy brief that will be out any day now from the Stanford Institute for Economic Policy Research (co-authored with Adam Shaw and Daniel Posthumus), where I’m a jolly-good policy fellow.

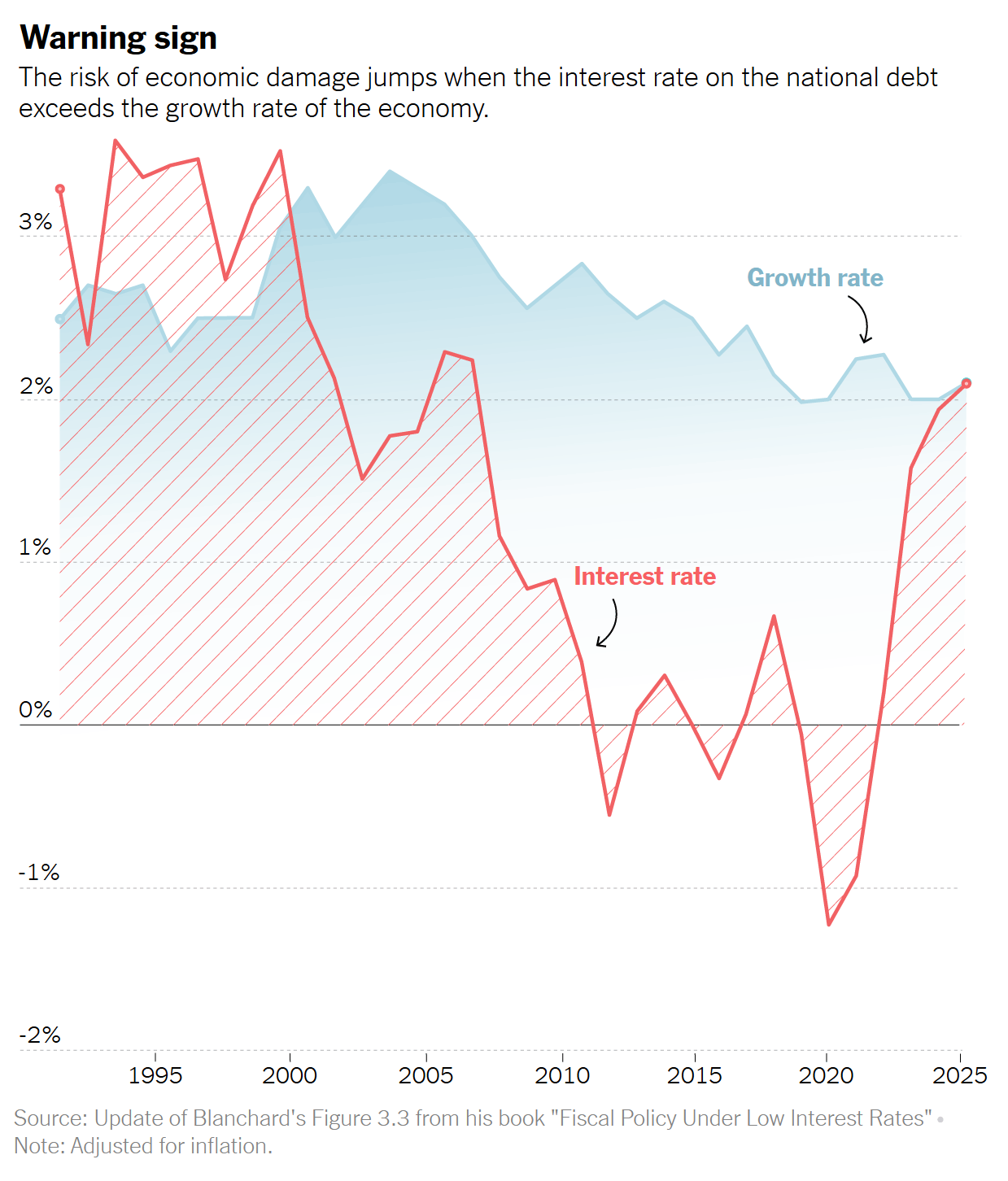

BLUF: For years, I and many like-minded colleagues have bristled at unnecessary fiscal austerity, or, if you like, deficit attention disorder. To be clear, we didn’t love the structural gap between what the nation collected in taxes and what it spent, but as long as the interest rate on the debt was well below the growth rate, as was the case, we could service our debt without breaking a sweat.

But, as seen here in one of our key figures printed in the oped, this is no longer the case, and if this sticks—if, the interest rate stays equal to or above the growth rate—well, that’s a game changer.

The rest is nuance and caveats. If the interest rate falls back down and rejoins its earlier trend, we’ll have more fiscal space. But in both the oped and more so in the SIEPR brief, we argue that Trumpian policies—e.g., the tariffs and the massively deficit-financed budget bill—push the three key determinants of debt sustainability—the interest rate, the growth rate, and the primary deficit (the deficit net of interest payments)—in the wrong direction.

If that’s the case, what can be done? As I note, “It’s not just that Congress won’t stop digging us deeper into debt. It’s that it has moved from shovels to excavators.”

We suggest a three-part plan that you can read about, but let me focus on one part here. Which signals should trigger our attention that something’s gotta be done to move us to a safer fiscal path?

We found this definition of sustainability from Abecasis et al (2025; no link) to be resonant:

If the debt grows large enough, the fiscal trajectory could become 'explosive' in the sense that interest expense would be so large that stabilizing the debt-to-GDP ratio would require running persistent fiscal surpluses of a size that has seldom been sustained in the past and is unlikely to be sustained in the future because it is economically costly and politically difficult.

This leads to the following figure from the brief, which requires some serious unpacking:

It shows primary deficits since the 1960s, and how they’ve clearly deteriorated. The blue dotted line at the end shows CBO’s forecast pre-big-bad-budget bill and the other dotted line is the Budget Lab’s forecast of the Senate version of the bill (which is close to what passed). The orange dots show the necessary adjustment—the change from big negatives to big positives—in primary deficits required to get fiscal policy back on a sustainable path (in the case, that means getting the real debt service as a share of GDP back down to 2% or less).

The magnitude of the adjustment is the difference between the green line (I think it’s green—color blind and no one’s around for me to ask)—and the dots, which as you see, outside of the big recessionary ups and down in this series, is what we call an AA: Ahistorical Adjustment. That’s precisely what Abecasis et al are worried about: that a debt shock would demand an historically large, fast, and economically painful fiscal adjustment.

Now, you may be thinking “Sure, if we’re the UK, where these kinds of debt shocks happen all too frequently. But not here!” And it’s true that the global market for U.S. sovereign debt remains huge, liquid, and is generally considered to be risk-free.

But that “generally considered” is starting to do a lot more work than it used to. You’ve seen what’s been happening to the dollar, right? More to the point, we show in the brief that the term premium on US Treasuries—the extra interest rate that investors insist on to buy longer-term debt—is drifting up.

The point of the oped and brief is that our budget math has gotten more dangerous. Maybe that will change, maybe it won’t. But when doves start to cry, it’s time to pay attention.

Dear Dr. Bernstein,

Wishing you had included the hit to projected growth from Trump's deportation funding explosion, hostility to foreign students, and already measurable decline in foreign tourism in your piece.

Perhaps we need to start discussing tax increases. I believe it's a fantasy to suggest that only corporates and the rich should face increased taxes although we should substantially increase effective tax rates. To pass such legislation most but not the bottom 20% or so should pay a bit of something more. It could take the form of higher retirement age, somewhat higher SS taxation for all but mostly raising the ceiling for contributions to at least $400k. We could also narrow the gap between taxes on capital and dividends vs. earned income.

A great start would be closure of the worst of the tax deduction giveaways starting with carried interest and moving on to LLC passthroughs.