Why is Central Bank Independence So Important?

Inflation control, of course. But it also allows the Fed, unlike politicians, to not overly discount the future.

I did a few media engagements yesterday touting the importance of CBI (central bank independence). Here’s one link.

The pressing question, understandably, is whether Trump can fire Jerome Powell, the Chair of the Fed, before his term is up a year from now. Of course, as Symone Sanders-Townsend pointed out during our MSNBC discussion, Trump nominated Powell for the gig back in 2017, but has been whining about him almost ever since.

I’ll say a few words about that, but it’s widely covered elsewhere. What I didn’t get into on TV was why CBI is so important. It’s something we thought a lot about back at the Biden CEA, motivating us to write a brief which holds up well.

As I said on TV, Trump’s been trash talking Powell for years. The highly elevated worry now is that Trump 2 is far less constrained by the rule-of-law than Trump 1. He could thus fire Powell without due process or ignore the courts should they decide the Fed chair should be reinstated.

That’s a powerful force in the wrong direction. But there are two countervailing forces. One, it’s entirely possible Trump’s setting up Powell not to be replaced but to stick around as the fall guy should those rising recession probabilities—purely a function of Trump’s actions—prove correct (and, as I wrote the other day, it doesn’t take a recession to trigger layoffs and related pain; growing at 0.3% feels awfully similar to working folks than shrinking 0.3%). Two, screwing around with CBI threatens higher inflation, higher (market) interest rates, and further erosion of faith in U.S. stability and assets. Trump’s already blinked once following a bond-market selloff.

What CBI means is obvious, but just to be clear:

An independent central bank is one that can carry out monetary policy without political interference. In an important distinguishing factor, governing bodies (typically national legislatures) legitimately dictate the goals or mandates of central banks, which, in the U.S. case, are maximum employment and price stability. But CBI requires that the Federal Reserve’s operational activities to achieve its dual mandate occur without political pressure or interference.

There are at least two reasons why this is so important. The reason that’s always cited first is particularly germane to today’s policy cluster*&#!: inflation control. The point is well-explained by Paul K today so I won’t dwell on it. But it’s also obvious: the risk that president’s will manipulate interest rates to juice the economy without regard to inflation is just too damn high. And that’s far from a theoretical concern. History is littered with examples.

Former Fed chair Ben Bernanke put it well: “A central bank subject to short-term political influences would likely not be credible when it promised low inflation, as the public would recognize the risk that monetary policymakers could be pressured to pursue short-run expansionary policies that would be inconsistent with long-run price stability.”

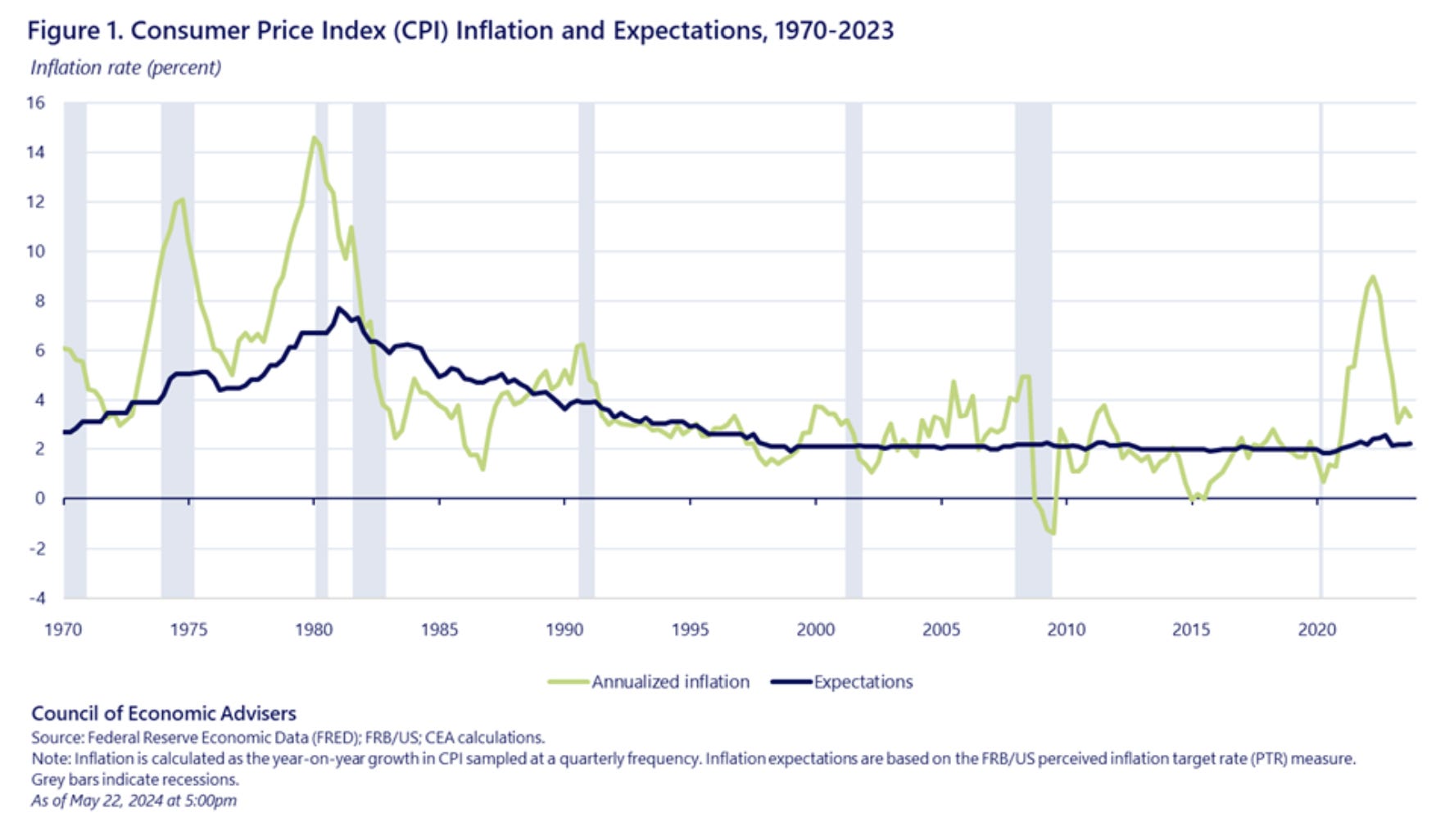

More CBI==>better anchored inflationary expectations==>more stable prices, even, as the figure below shows at the end, through an inflationary shock.

But I’d like to focus on a more nuanced value of CBI, one that has long interested me in political economy: the problem of overly discounting the future. Politicians, and therefore the policy makers that work for them, as I often have, are incented to worry about the next election, not the long-term. So, for example, deficit spending to provide goodies to constituents today makes a lot more sense to them, regardless of the fiscal outlook, than say, a tax on carbon to mitigate climate change.

Its CBI provides the Fed “the insulation it needs to implement policy over longer time horizons, without reacting to near-term political pressure.” What does that look like in practice?

In fact, we’re seeing it in real time. Because the trade war is stagflationary—slower growth and higher inflation—and because inflation is still not back down to the Fed’s target rate, they can’t provide Trump with the “put” he seeks against the economic damage he’s meting out. Instead, Powell has to take what he correctly calls a “wait and see” approach, a luxury that CBI affords him.

If the trade war and the whiplashian uncertainty its implementation is delivering unto us were to hurt growth a lot more than raise prices, the Fed will cut the benchmark rate it controls. But neither Powell and Co. nor the rest of us know where this mishegoss is heading (that’s two vital Yiddish words this week!). Their remit and their independence—and they can’t meet the former (full employment at stable prices) without the latter—allows the Fed to act not just on the present but to consider longer-term, future outcomes.

Such patience, caution, measure-before-you-cut (or raise) is, of course, anathema to Trump (and, to be fair, to most politicians, though he’s worse). But history is clear that these actions—or inactions, if that’s what’s needed—are central to central banking, and CBI is key to making sure they it remain in place.

From an engineering point of view, to achieve a stable system, feedback needs to happen with the right phase AND respond to changes much more slowly than the behavior itself changes. Otherwise the system keeps chasing an unstable target and usually goes into very unstable behavior.

Allowing Fed policies to change according to political whims is a near-guarantee for instability, when what's needed is a slowly changing response with the right timing.

Firing Powell is a one way trip to a nine handle on the 10 year.