Are Layoffs Accelerating?

The job market appears to be slipping a bit more and, while growth remains positive, it's more fragile than I'd like to see.

For awhile now, the best way to describe US labor market conditions has been “low-hire, low-fire.” That’s not great, as in a robust labor market, hiring would be stronger than it is, providing insulation should layoffs tick up, along with ample opportunities for folks coming into the job market and those trying to move from unemployment to employment. But as long as layoffs stay down, the economy can continue to expand and working families can continue to get by, though with all the affordability headaches I’ve long focused on up here (and dig into more deeply here with respect to last week’s election).

But if layoffs start to proliferate and hiring stays low, that’s a recipe for much slower growth, if not recession. Highly concentrated stock market wealth can juice consumer spending up to a point, but there’s no period in the history of the American business cycle wherein layoffs spiked (which, to be clear, is not currently the case) and we did not have a recession. It’s kinda definitional (i.e., I could have said “no recessions without layoffs”).

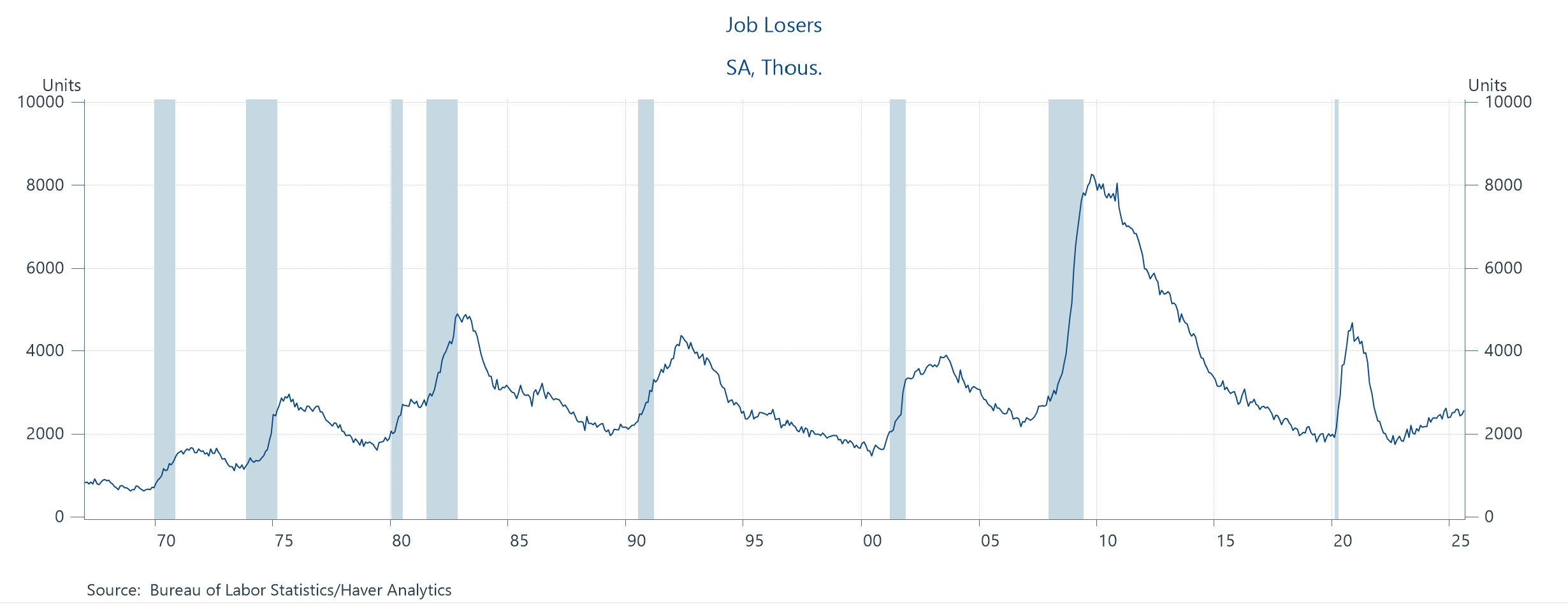

As you know, we don’t have labor market data for Sept or Oct, though we should have Sept soon. The end of the above figure shows a slight uptick in layoffs through August but there’s more up-to-date info on layoffs from non-gov’t sources, along with UI records, which, since they’re derived by state UI offices, have mostly continued to flow.

And these data are flashing some warnings. I’d barely call these “yellow” flashes, and they’re certainly not red. But in cases like this, you’ve got to use your sniffer to try to sense if there’s a potential new trend developing, and I’m concerned there’s something in the air.

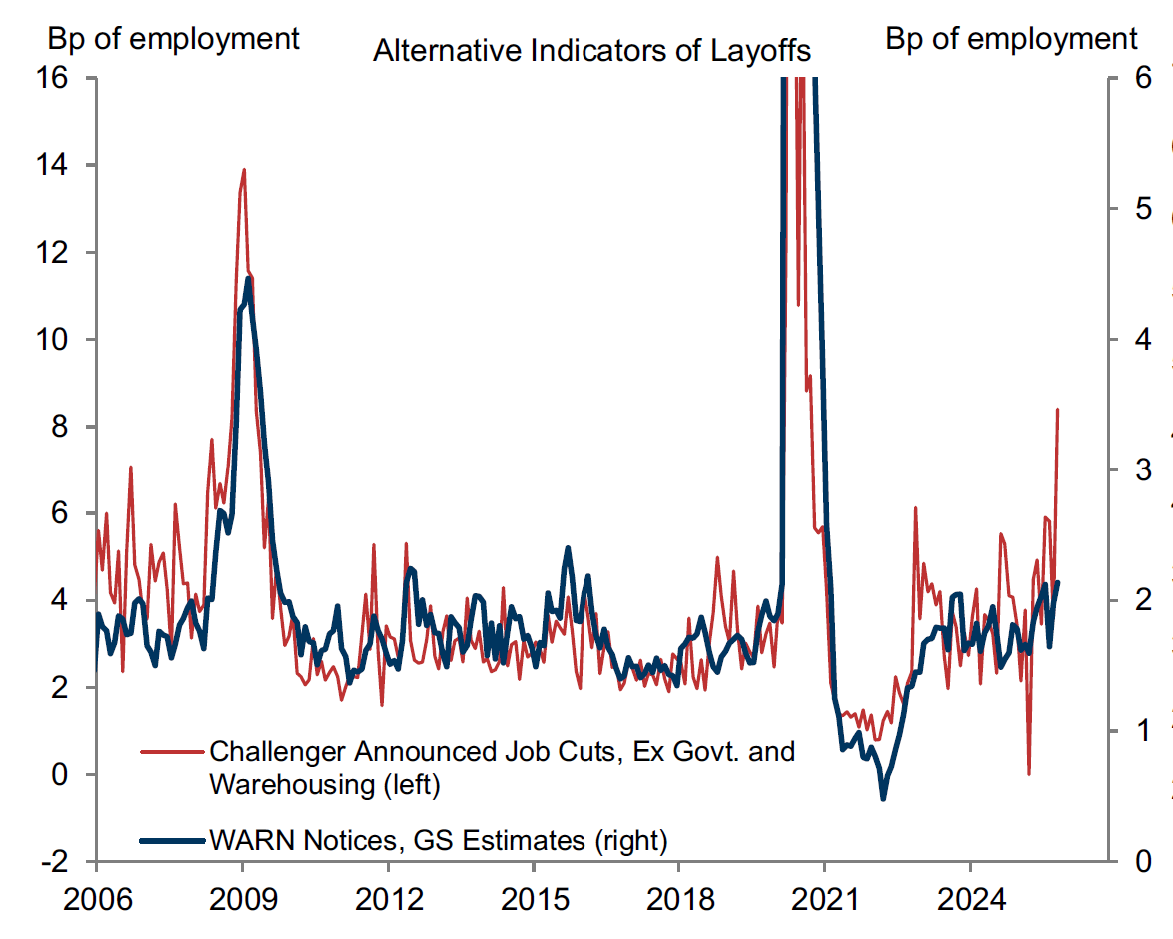

The GS Research team posted a couple of interesting, less familiar figures on layoffs. This one shows the Challenger et al data, which tracks corporate layoff announcements, along with the WARN data, which companies must file in advance of large layoffs. They’re quite noisy/jumpy, and they’re around their levels in the solid 2010s labor market, but there’s a tilting-up trend at the end.

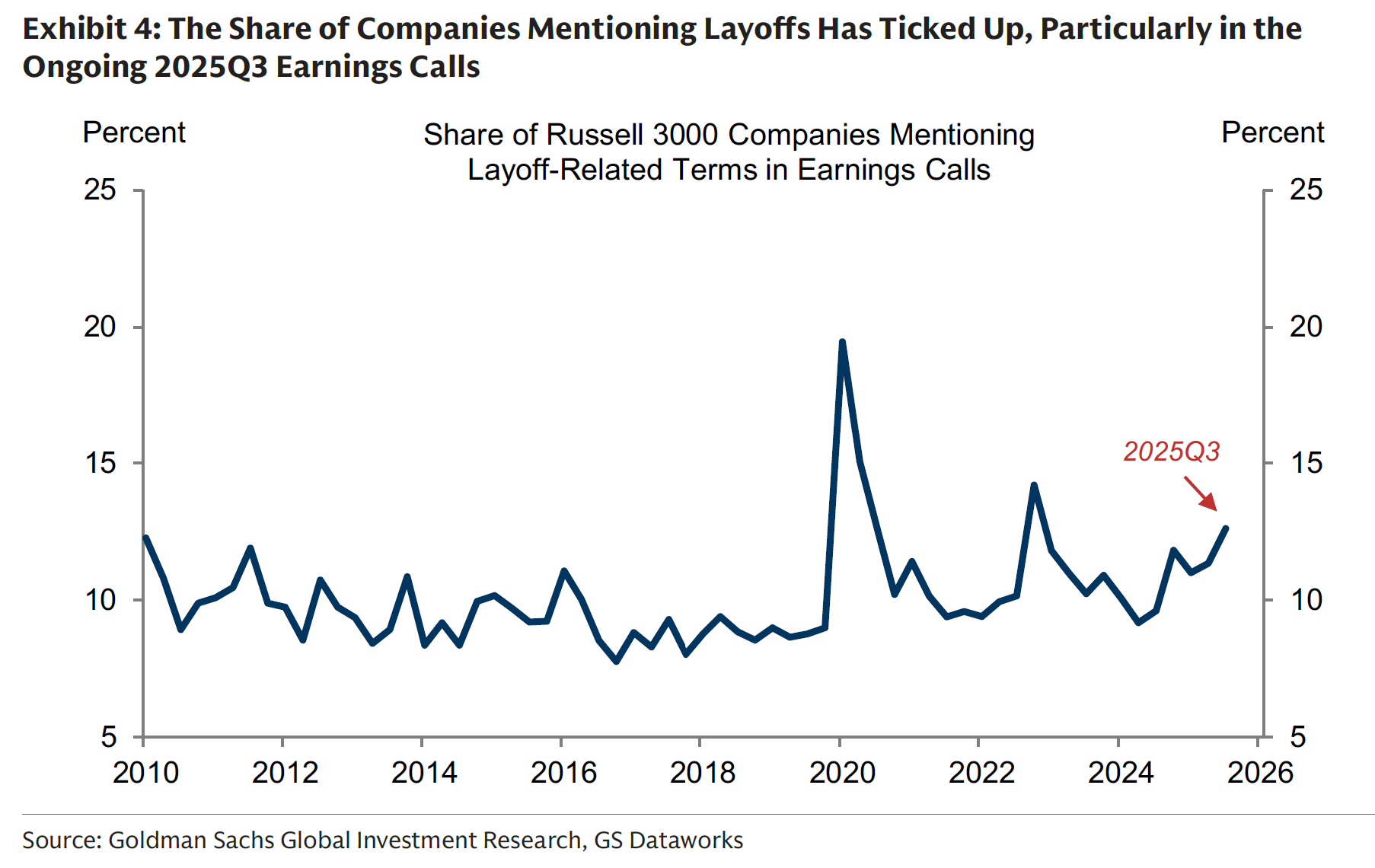

The GS team shows a similar, though again pretty subtle, uptick in layoff-mentions during the earnings calls of large and small cap companies.

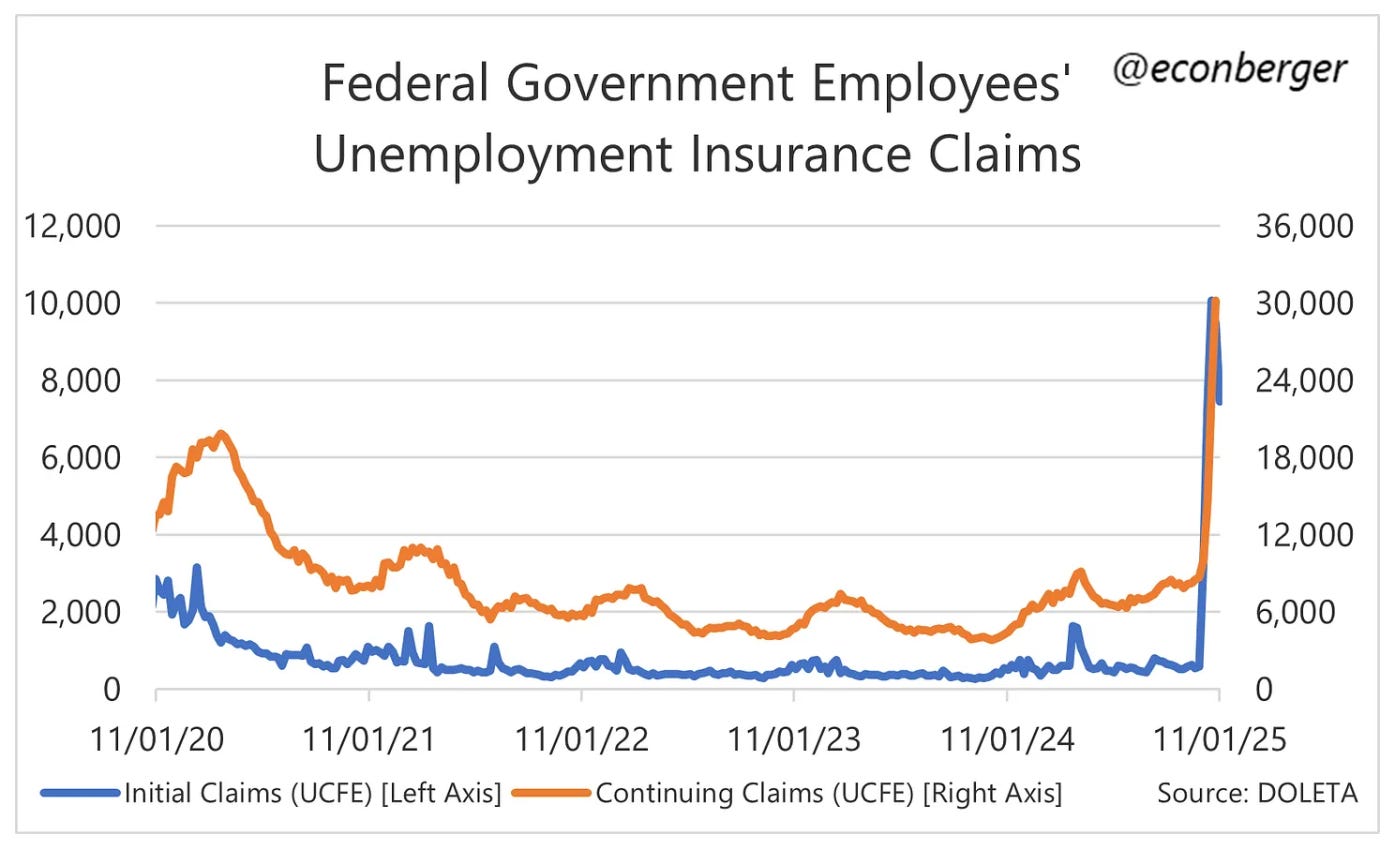

Initial and continuing UI claims, however, are not trending up much at all, with the dramatic exception of the spike in federal gov’t UI claims (from Guy Berger’s excellent summary of labor market data). Of course, given that the reopening agreement includes bringing these workers back, that spike should reverse, if the Rs keep their word, which I’ll want to see to believe. At any rate, while initial claims are among the most timely labor market data we get, they lag, e.g., WARN notices, again by definition.

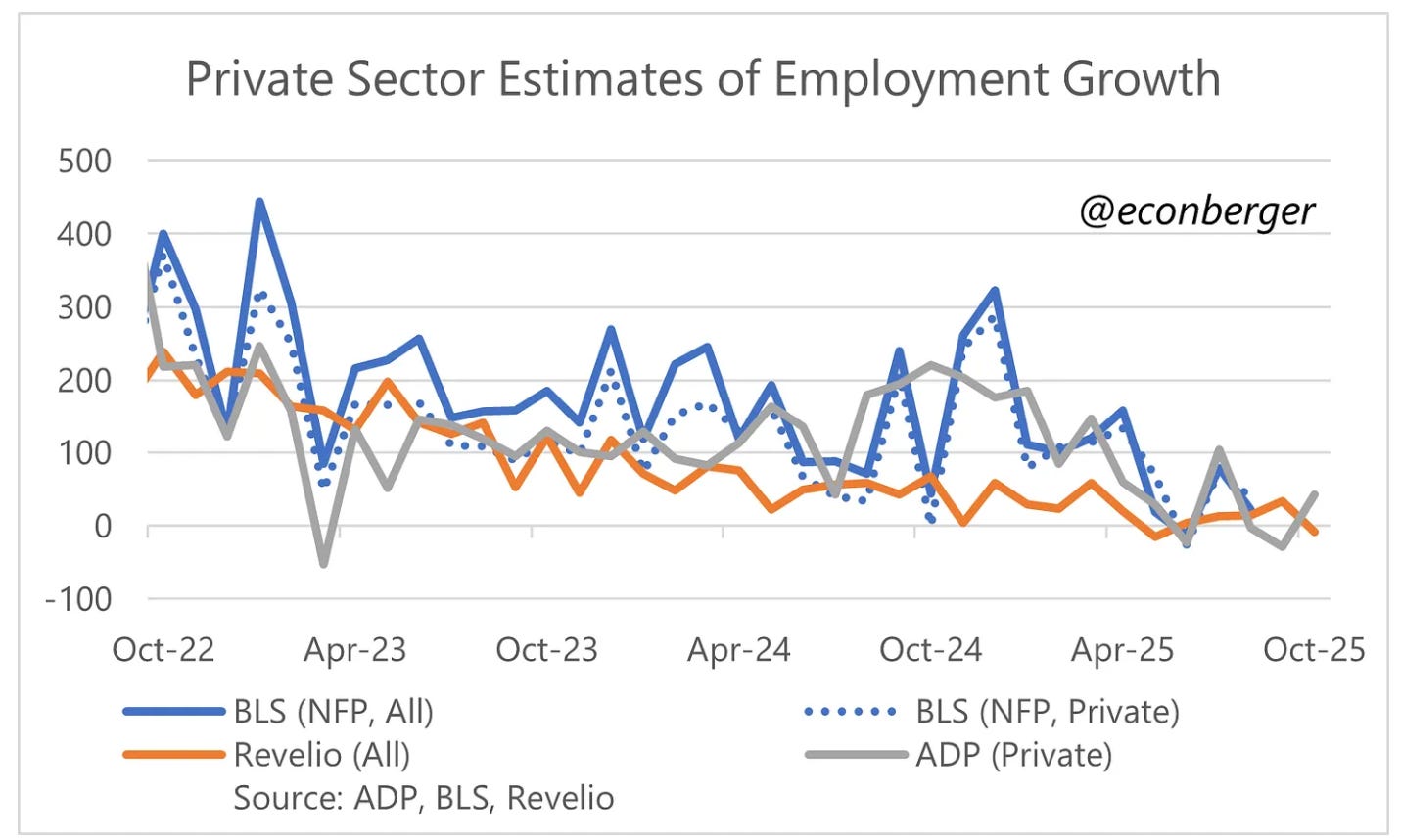

Berger also shows that hiring remains very weak, with some of those series scraping bottom. (If you’re not familiar with “Revelio,” they’re a private data source that, according to ChatGPT “uses hundreds of millions of online professional profiles, scraped or aggregated from professional networking sites, resumes, job-history repositories.”) :

Both GS and ADP predict payrolls declined in October, and remember, ADP is private sector only, so that’s not including gov’t workers.

The thing you always want to ask yourself in these moments of non-clarity, which are not uncommon in empirical analysis of high-frequency data, is what’s the potential macro story behind this? When you’re noodling over the labor market, recall from econ 101 that demand for labor is derived demand, stemming from spending, investment, and “animal spirits” (consumers’ vibes).

As I referenced in passing above, consumer spending seems okay though it’s hard to tell without gov’t data. The WSJ leans hard into the “wealth effect” story, arguing that “Americans with large investment portfolios feel markedly better about the economy than those who don’t own stocks:”

…and their story is ripe with anecdotes from retailers about declining sales from consumers who depend on their paychecks as opposed to their stock portfolios.

Similarly, business investment appears solid, but it’s thin, driven largely by tech, AI, and data-center capex.

Consumers’ vibes are in a particularly bad place, though you have to discount this a bit because they’ve been so for a long time now, including over periods when spending was strong. When it comes to the American consumer, don’t just listen to what they say; watch what they do.

Okay, that a lot of on-the-one-hand-on-the-other for a Tuesday before noon. So, here’s my bottom line:

Growth is positive but fragile, and there are signs that layoffs may by ticking up. Once we start getting labor market data again, don’t be surprised to see the jobless rate tick up a few tenths. None of that is near-term recessionary, but if the slight layoff trends shown above turn up sharply…well, that’s a different story.

Jared - thanks for sharing! I’m not cool enough to be on the GS distribution list. :)

I’m interested in how the GS layoff tracker will perform out of sample - my bet is we’ll know pretty soon, via initial claims, whether layoffs really are increasing by a meaningful amount.

Final point - looking at the time series, the layoff tracker has been running above late 2010s levels for the last few years. That contradicts JOLTS

One shouldn't keep chasing noise. These kinds of data are very noisy and a change has to get way outside of the region of normal variation for one to be able to conclude anything in a short time period or two. The graph of Federal workers' unemployment claims is an example of going well beyond normal variation. These month-to-month changes in job data are not.