Digging Into The Recent Wage Decline

It's mostly war-driven inflation, but it's not only that.

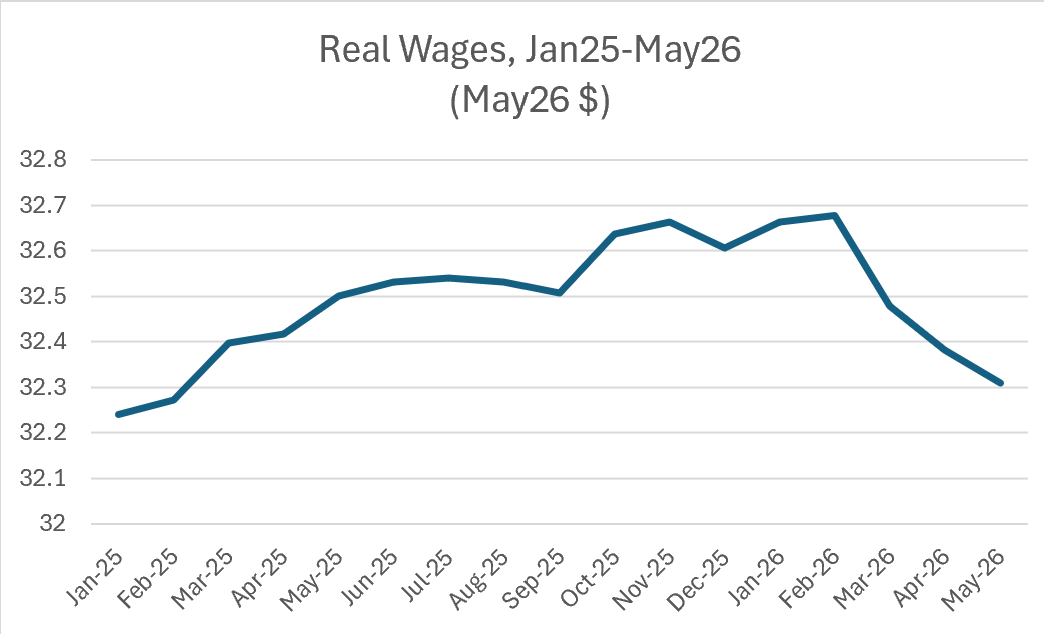

We’ll see if the most recent round of negotiations to end Trump’s war-of-choice in Iran is truly taking hold. Spokespersons from both sides have zero credibility. But what we can know is that the war has taken a toll on real wages. The figure below shows the real hourly wages of the 80% of the workforce that’s middle- or lower-wage workers (“production, non-supervisory”) in May ‘26 dollars, from Jan25-May26.

As the war commenced and inflation spiked, real wages fell (see also Aaron Sojourner on this point). But it wasn’t only inflation. The other part of this decline is slowing nominal real wage growth.

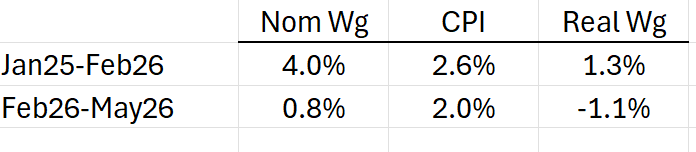

The percent change in real wages roughly equals the percent change in nominal wages minus the percent change in inflation (use natural logs, as I do throughout, which approximate percent changes, and you can lose the “roughly”). Higher inflation, lower real wage growth; slower nominal wage growth, same result. Here’s a table breaking out these components over the real-wage-increase and decrease periods.

Over the wage-growth period, nominal wage growth beat price growth by 1.3% (which is 4%-2.6% with the difference not exact due to rounding). Since Feb of this year, the reverse has occurred, with inflation outpacing wage growth to the extent that it wiped out almost all the real-wage progress since Jan25.

It is important to note the these changes are not adjusted for the fact that they’re taken over time periods of different lengths. It looks like inflation grew more slowly in the real-wage loss period but that period lasts for only 3 months vs. 13 months for the real-wage gain period. Annualized (i.e., put on a comparable basis), inflation grew 2.4% over the first period, and 7.9% over the second period.

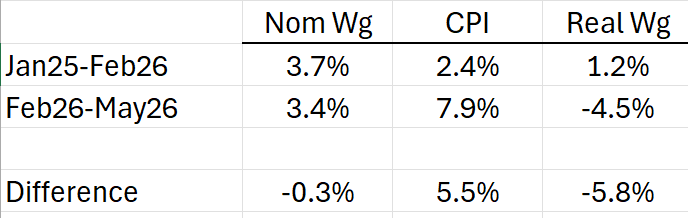

Annualized version:

Now, focus on the “change” line. On an annualized basis, meaning what we’d see over a year if these growth rates persisted over a 12-month period, wage growth swung from rising at an annualized rate of 1.2% to falling at 4.5%, and negative swing of almost 6%. Most of that was inflation, but a little bit was slower nominal wage growth.

In other words, working families, already stressed by trying to make their paychecks go far enough to meet the affordability challenges they face, are now hit with slower wage gains and much faster inflation. And since these maladies are policy driven, you could call it an own-goal kick or a kick-in-the-face. And by the guy who, a couple of days ago, said the following:

That is a surprising take.

A few caveats must be considered re the above. There are many different wage series, all of which come out later than the one I used, so we’ll need to see what they do in this regard. The most important caveat is that if the war ends and the oil supply goes back to something close to prewar supplies, inflation will come down and real wages should start to grow again. Also, there are some signs—though I’m not certain how reliable they are—that the American job-creation machine is running in a higher gear. If that’s so, we should see the labor market tighten and that could boost nominal wage growth.

But if there’s one theme two themes I keep coming back to in this Substack, it’s that a) policy matters, and bad policy will eventually show its works, and b) this administration is pushing hard in the wrong direction on affordability. While that conversation often takes place in price terms, the buying power of the wage is, of course, a critical piece of this puzzle.

Might be worth running the CPI without fuel. Wonder in the nominal wage slowdown is about sectoral composition of recent job growth…

Typical families respond to inflation by taking on additional debt or second jobs to maintain spending levels. There are signs that debt service is becoming a problem. The inflation we’re experiencing could trigger interest rate increases, which will cause even more problems with debt service. We’ve had fifty years of fiscal policies that benefit the wealthy at the expense of all others (lower income tax rates, lower capital gains tax rates, higher exemptions from inheritance taxes). We’ve had 40+ years of rulings from the Supreme Court that tip the balance of bargaining power to employers. The middle and working classes have been stretched to the point where modest inflation and modest interest rates (6% mortgage rates are not that high on a historical basis) cause meaningful problems. Now, we have moderate inflation and moderate interest rates and we’re about to have major problems.