Reflections on Two Recent Posts: Debt and Prices

Also, if you're not doing lunch with me and my friends at the Contrarian on Tuesday at noon (ET), you should be!

The subject of two of my recent posts have been bouncing around in the press lately in ways that warrant revisiting. I’m referring to the Presidents and Prices post and the Debt Unsustainability post.

Starting with the debt post, I argued that current policies by Trump and the Republican Congressional majority bode ill for the debt outlook. I didn’t show the algebra but in this case, I think it’s perhaps clarifying.

This is one common way of representing debt dynamics, from this helpful explainer.

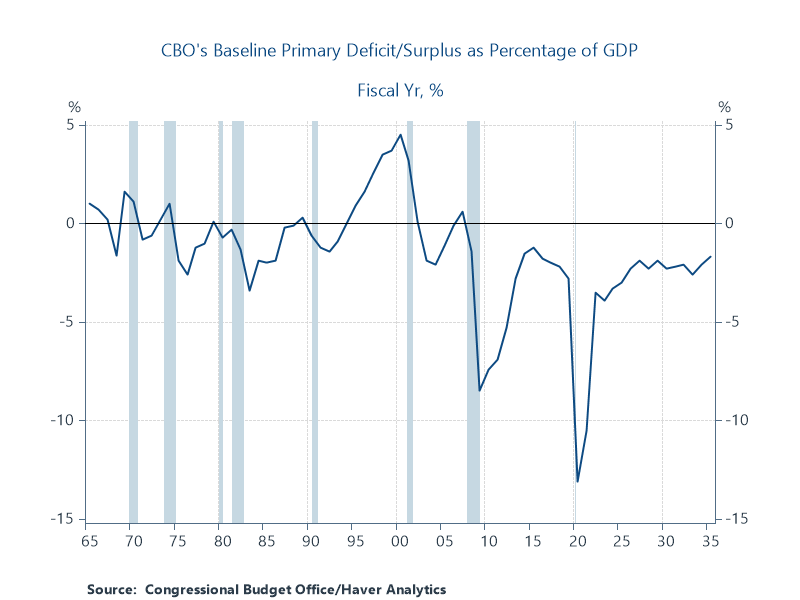

“b” is the debt/GDP ratio, r the interest rate, g the growth rate. I spoke about those yesterday, but I didn’t say much about s, the primary deficit (the deficit net of interest payments on the debt) as a share of GDP, and s is big deal. A very big deal. But put it aside for a sec.

What this formula says is that, again, putting aside s, the interest rate relative to growth rate times last period’s debt/GDP determines this period’s debt ratio (that -1 next to b just means lagged one period).

Suppose r = g. Than the first term equals 1 and (still ignoring s), this period’s debt equals last period’s. r > g, b goes up relative to b(-1), etc.

Much of the r and g discussion stops there. And for many years, that made sense because primary deficits weren’t a big factor (see figure below). The latter 1990s, in fact, featured sizable primary surpluses (btw, s stands for surplus, so a primary deficit in the formula is added onto the debt).

But those days are behind us, and CBO predicts them to stay behind us. Moreover, should the R’s pass their budget plan, CBO’s budget-forecast update will show much larger primary deficits.

This is why s is so important. If you follow these numbers and you think about the formula above, you might think: “hmmm, we’ve had solid growth and low interest rates for years, so how could it be, given that first term in the formula, that b (debt/GDP) has gone up? It must be s!”

Bingo.

Which is why we get this in today’s NYT:

…the concern is that the administration’s tax bill will add to the federal deficit, which is the difference between the government’s income and expenditures.

That would mean more borrowing — the U.S. federal debt on pace to set a record, relative to the size of the economy, going back centuries — and investors potentially demanding higher interest rates in return. Already there are signs that the premium demanded by investors to lend to the government has risen, a sign that they perceive a higher risk.

In formulaic terms—and here I’m just mapping what I said yesterday onto the math—current fiscal policy threatens to push up r, current tariff policy threatens to lower g, and the truly egregious deficit-financing of the tax cut seriously threatens s. Every term is under siege, so yeah…this time is different.

And the formula is unforgiving (i.e., nonlinear). Just for giggles, I added a point to r, subtracted a point from g, and added a point to s (increased the primary deficit by one point). That added 6 percentage points to the debt ratio. Which is a lot. I knocked my simulation down to half a point, which added 4 ppts. Also a lot.

Turning to Presidents and prices, I wanted to bring this interesting Noam Scheiber piece to your attention. It’s about how presidents, in this case, both Biden and Trump, try to push companies to lower prices. My experience, as noted in my post, is that firms generally don’t give a ton of weight to such bully pulpit-ing, but what I found notable in the piece was how many different views there are about how prices are set.

Elizabeth Wilkens, the president of the Roosevelt Institute:

“I’m not here to tell you whether [Trump’s] right about certain industries. But the basic idea that companies have more pricing power than we believe that they did is something we should interrogate.”

“…the size of a company’s profits has little effect on its decision to raise prices, said Chad Syverson, an economist at the University of Chicago. Most companies want to preserve their profits whether they are large or small, because failing to do so would incur the wrath of their owners or shareholders, some of whom are pension funds and small-time investors. They pass along price increases to consumers instead.”

“if, in some cases, companies increase prices by even more than the jump in their costs, that doesn’t necessarily reflect nefarious behavior, said Alexander MacKay, an economist at the University of Virginia. It may reflect the fact that consumers are no longer as turned off by price increases.”

Oren Cass, American Compass:

“If Walmart were to simply adopt a policy that ‘we will not change our prices in response to the tariffs,’ there would be some situations where suppliers ate the costs, some where suppliers shifted to other sources of supply to avoid the tariffs and some where Walmart accepted lower margins.”

There’s margins to protect, pricing power (which in textbook econ is generally considered to be nil, at least for non-monopolists), consumers’ response to price changes, the degree of competition in a sector enforcing more competitive pricing, and Cass’s just-do-what-the-president-tells-you, damnit!

I agree that all of these can be in play, though as I argue in the piece, many of the above forces ebb and flow based on evolving factors. If people get a positive income shock, that can dampen their responsiveness to price hikes. Firms can take advantage of an economy-wide price shock to raise prices not just to cover costs, but to boost their margins. Though as the shock fades, that pricing power also ebbs.

But I tend to be guided by the view that the one constant amidst all these dynamics is margin protection. Of course, margin width matters, as Trump himself kinda says in Scheiber’s piece.

Mr. Trump suggested that Walmart use its billions in profits from last year — “far more than expected,” he wrote on his platform Truth Social on Saturday — to cushion consumers against price increases.

But that’s not really how they roll, as Syverson says. That is, firms don’t go here: “Hey, we had a good year last year, so we’re gonna help the POTUS this year by eating the tariffs.” This is why virtually every empirical study shows that firms will try to pass at least some part of cost increases, including tariffs, forward to consumers.1

It’s also the case that in much of retail, even big-box, margins are narrow, in the 2-4% range, so there’s only so much they can eat. I thought this Axios post today on the price of footwear was elucidating in that regard.

Given typical margins in these industries, importers can only eat so much of the tariff costs before they hit a cash flow crisis that leaves them short on the capital necessary to import the next batch of goods.

When I was in the White House, we spent a lot of time thinking about price-setting issues, along with peoples’ response to price pressures—that whole vibes thing. It’s a very rich area of inquiry, one I’d argue economists could usefully spend more time digging into.

Finally, does everyone here know about the Let’s Do Lunch event I run every Tuesday at the Contrarian from noon to 12:30? I’ve been getting incredible guests to answer folks’ econ questions, which we burn through with speed and, I think, pretty good clarity. Here’s yesterday’s with an up-and-coming economist you should know. I think he’s gonna be important some day. Next week, the return of the thoroughly awesome Heather Long!

Yes, this includes minimum wage hikes. It’s one reason why the argument that firms will just fire the affected workers is wrong.

One aspect of the shift in source of federal tax receipts from corporate income tax to personal income tax combined with the decline in IRS enforcement is an increased beta between GDP declines and general Fed receipts.

As your graph shows clearly, economic contractions lead to rapid and substantial tax receipt declines.

What happens when our economy slows down this time?

Not only will withholdings decline BUT ALSO clever accountants will help oligarchs and oligarch adjacents avoid tax. This will be 2008/09 on steroids.

We so needed to elect a Dem, raise taxes on the wealthy and beef up IRS enforcement.

I hate a President who bullies companies to cover his stupidity. But there are some additional facts to greedflation in America. I do remember a time, when I was young, that buybacks were illegal.

https://www.baystreet.ca/articles/stockstowatch/103265/Walmarts-Stock-Buybacks-In-Fiscal-Q2-Totaled-Nearly-1-Billion

On top of the buybacks of 2022 and 2023.