This Ain't No Light Switch

If the ceasefire holds, it will take time before you feel the difference in your wallet. (Also, a few sentences on this AM's PCE data.)

The cease-fire appears shaky and markets/oil are, at least for now, reversing some of yesterday’s gains. From the NYT:

In a statement on social media, Iran’s parliament speaker, Mohammad Bagher Ghalibaf, insisted that three clauses of what he said was a 10-point “agreed framework” between the U.S. and Iran had already been violated, including an end to Israeli attacks on Iran-backed Hezbollah fighters in Lebanon. The Trump administration says that was not part of the agreement.

I’ll leave it to others with more experience in such matters to interpret the negotiations that are slated to start this weekend in Pakistan. What I wanted to briefly note this AM, while awaiting the late arrival of the February PCE data, is why consumer costs will face ongoing pressure from the economic impacts of the war, even if it is winding down, which is, at this point, not a small “if.”

First, there’s a fair bit of chatter about the “rockets/feathers” point I’ve often made here re gas prices. A common explanation I’m seeing in the papers is that gas prices fall more slowly than oil prices because stations will use up their more expensive inventory before lowering retail prices upon receipt of cheaper gas.

Okay, I guess, but that’s an asymmetric argument: sellers don’t wait to raise the price while they’re working through their cheaper inventory. You’ve got to factor in consumer behavior. Apparently, once prices start to come down, we don’t do a lot of searching for a station where they’re falling faster. The price setters know this, so as long as they’re gradually—feather-like—cutting costs, they don’t have to worry about competitive pressures.

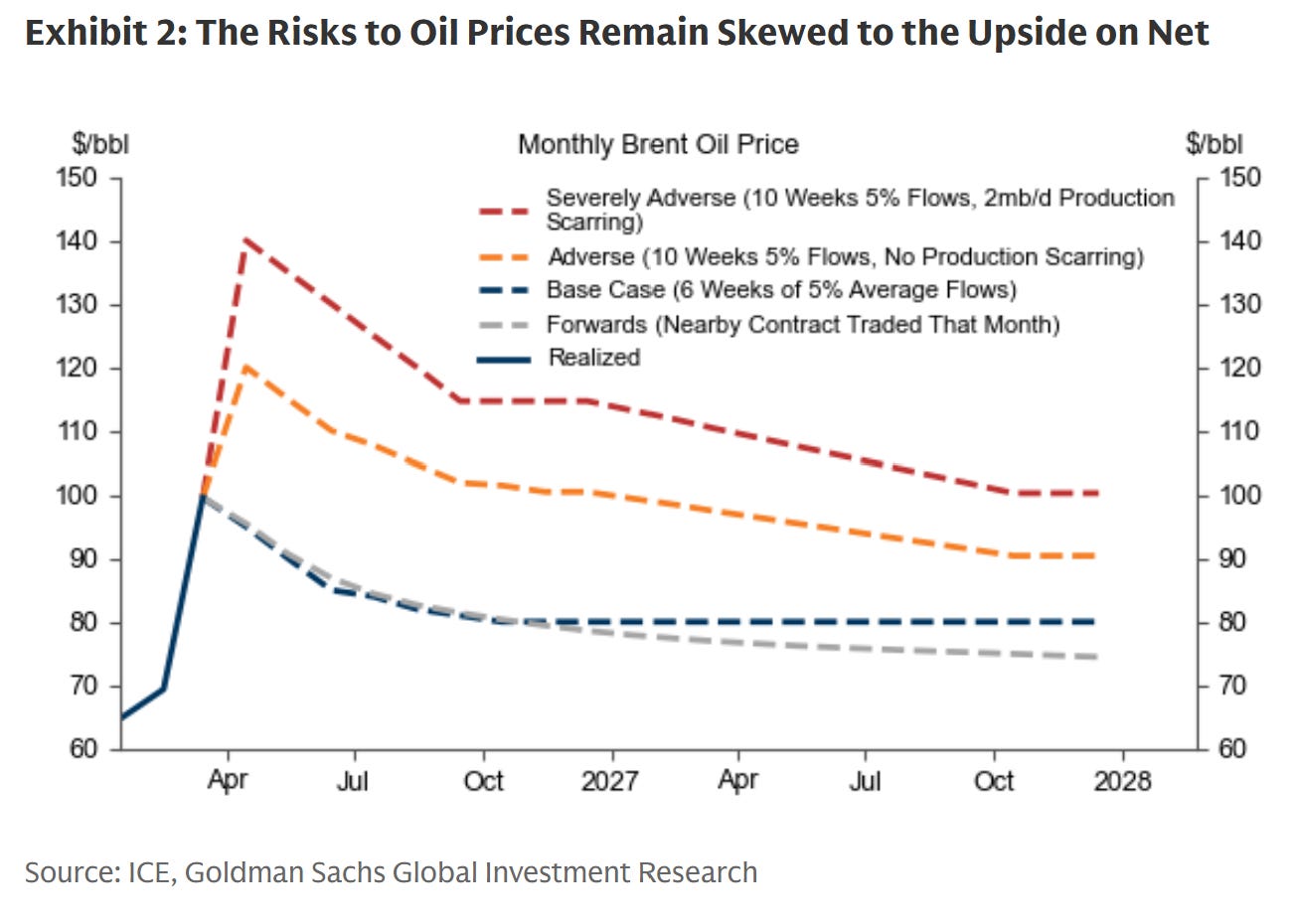

The upshot is that, if oil follows the new GS base case shown below, which is close to what we simulated in our exercise of mapping that trajectory onto retail gas prices…

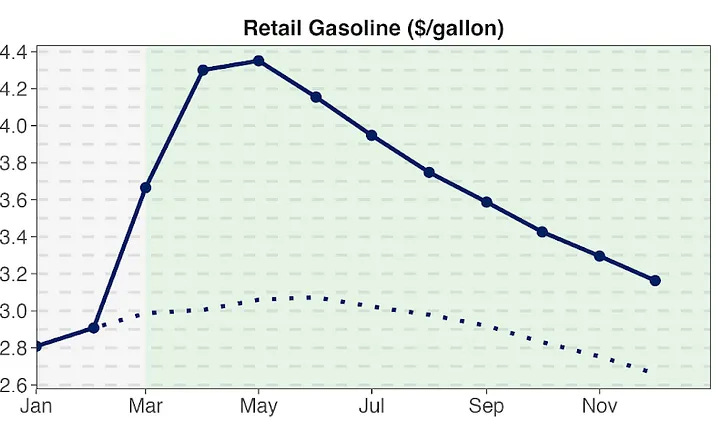

…we expect to see a gas-price trajectory that looks like this (the dotted line is the prewar baseline)…

…meaning we don’t get back to prewar levels this year.

GS researchers say, and I agree, that there is upside risk to their base case for oil, meaning there’s a decent chance we’ll end up with the yellow or red lines in the oil figure above, which assumes that it takes longer to unsnarl the SoH (yellow) and adds to that production destruction (red line) in the most adverse case.

Regarding that last point, when it comes to restarting energy production, especially given war damage to infrastructure—and importantly, we’re talking both oil and natural gas production—this is no light switch. Here’s a great read on that:

…dozens of refineries, storage facilities, and oil and gas fields in at least nine countries, from Iran to the United Arab Emirates and beyond, have been targeted in strikes. All told, 10 percent or more of the world’s oil supply has been turned off. Restarting those operations will require not only safe passage through the Strait of Hormuz, but also inspecting pumps, replacing bespoke processing equipment and recalling employees and ships that have scattered across the globe.

Re that “safe passage through the SoH” part, we don’t even get to this turn-on operation until that’s clarified. I assume we’ll learn more about where the parties stand on this once the negotiations begin, but among the strategic failures of this war from the US perspective, the fact that we’ve emboldened the Iranian regime to flex their control over the Strait and thereby the Persian Gulf and thereby the rest of the world, stands out as the most egregious.

We learned this morning that the PCE price deflator for February (prewar) rose 2.8%, year-over-year, which is around where it’s been stuck for a while. This is the inflation gauge the Fed watches most carefully, and it remains well above their 2% target. In other words, the PCE was already elevated before the war, partly due to tariff pressures. Same with food prices, btw, which were up 2.3% yr/yr through Feb in the PCE (2.4% for CPI groceries).1 Tomorrow, we’ll get the CPI for March, which will reflect the war’s impact. It’s expected to come in a 3.3%, almost a point higher than Feb’s 2.4%. I’ll write up both the CPI and PCE reports tomorrow AM.

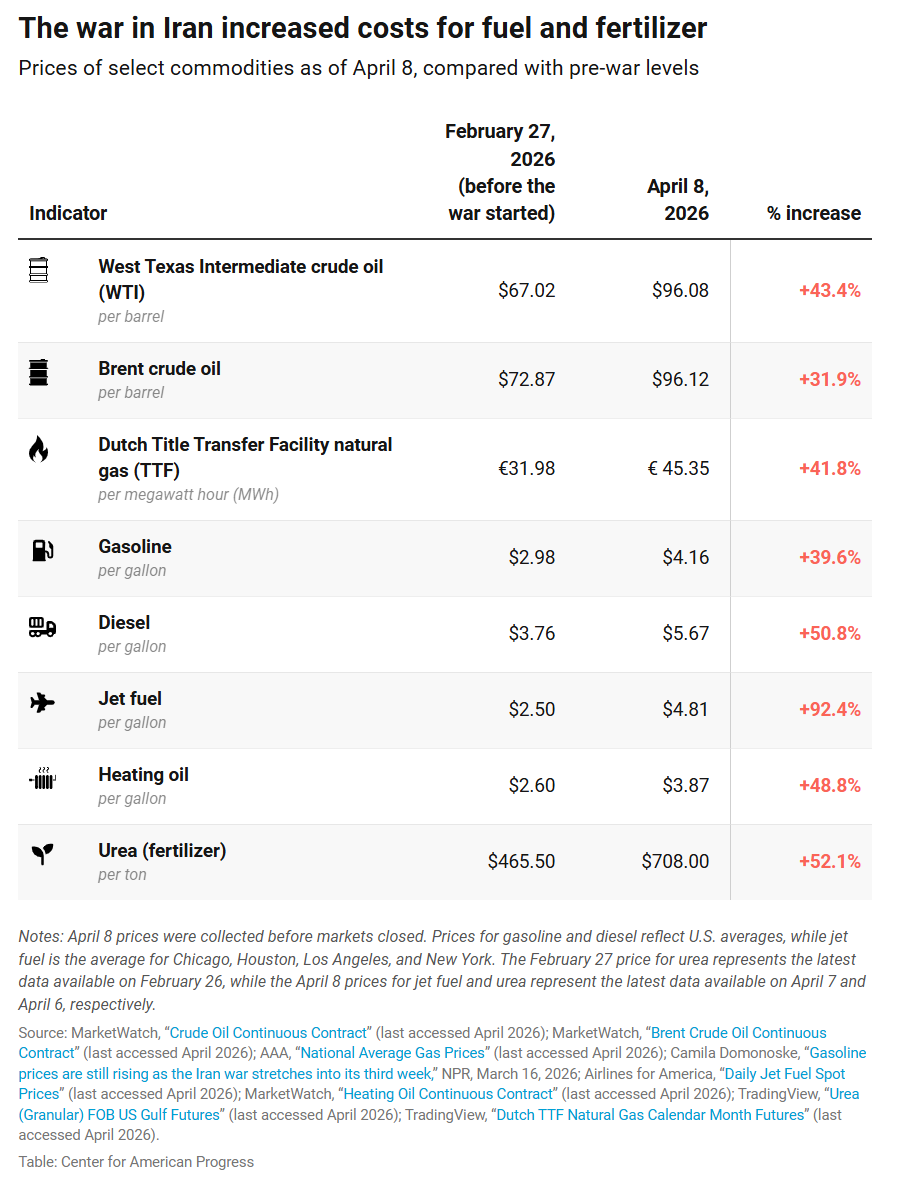

Below is a table from my CAP colleagues on war-cost increases for key commodities affecting energy and food:

These are historically large spikes, and while I expect some forthcoming down drifts, I expect the same “elevator up, stairs down” for most of these prices as described above for the gas price.

Here’s something I read this AM that resonated:

America’s allies and partners in the Middle East fear that…they will end up paying the price for a war in which the overwhelming military might of the U.S. and Israel failed to secure political gains.

Again, others will plumb the geopolitics of that view, and as we’re still in the middle of this cluster-mess, it’s too soon to evaluate the longer-term outcome. But it’s not too soon to assess the impact of the war on costs and affordability. It has raised prices on an already price-stressed public, and those prices are not likely to retreat anytime soon. It is thus the latest example of the Trump administration pushing hard in the wrong direction on the very issue most households are most worried about.

If higher prices were the cost of a just war that made sense to the American people, that protected our allies and innocent civilians against oppression, that disempowered a non-democratic aggressor, that would be a price that most of us would willingly pay. But this is not that.

Other relevant Feb PCE results include the core inflation rate also stuck at an above-target 3% for three-months running, and weaker than expected real consumer spending, up 0.1% in Feb after being flat in Jan. I’ll go deeper tomorrow, but the report is likely to be another data point that keeps the Fed on hold re interest rates, though also concerned that real spending, which has a long been a key growth source for US macro, could be slowing down.

Oh,the damage is long term and done! Project 2025 is made to kill democratic rights of the indentured servants and they are allowing it to be done to them by the criminal US regime.

Roll guillotine! We need to tear this government down and rebuild EVERYTHING because we have allowed the greedy and hateful into power. Let it get uncomfortable; I am waiting for the rest of the country to figure out what many decent people saw decades ago for the need to make the UD government work for its citizens, not us to support Oligarchs and senators.

Wake up, America!

Keep in mind that it takes 5-6 weeks for ships leaving the Gulf to reach China or Europe. Ships leaving before the closure are just now reaching their destination. Thus, there really hasn't been an experienced shortage up until now. The price spikes have been anticipatory. Ships that didn't leave the Gulf during the shutdown are only now starting to not arrive, so even if the Strait opened fully, we'd see a shortage for the next month or so.