Last Week's Wrap-up

What now, after Carney's bold stand at Davos? We too should import China EVs under a low quota. Inflation, spending, net worth. Japan's Truss moment: could it happen here?

“I sent for you yesterday, but here you come today.”—Count Basie

I’m a day late with the wrap-up as I wrote yesterday about the national emergency unfolding in Minneapolis, one on which I will continue to focus until the killers and their enablers are brought to justice.

Carney’s Bold Stand

By now, many commentators have touted the courage, clarity, and force of Canada’s PM Mark Carney’s speech at Davos (mine was an early entry). In my experience, it is sometimes the case that in the midst of a crisis—in this case, NATOs most powerful country turning against the alliance—should someone stand up a tell the truth, as Carney did, it frees a lot of other people to climb out of the river of de’Nile, towel themselves off, and get to work building a new regime.

We’ll see how far that goes, and in Canada’s case, in particular, the path outlined by the PM is not at all without risks. Consider the USMCA, the trade agreement the US signed with Mexico and Canada in Trump’s first term. Because this agreement is (somehow) still holding, the vast majority of Canada’s exports to us are duty-free. And, of course, the US is the destination for about three-quarters of Canada’s exports.

Later this year, the deal comes up for renegotiation, so it seems clear that Carney is operating under the assumption that it won’t get renewed, or at least not with acceptable terms. And no one can trust this admin to honor a deal, anyway.

I agree with Fen Hampson, professor of international affairs at Ottawa’s Carleton University, who said in the WSJ, that:

Carney might be making a “calculated bet that USMCA cannot be salvaged on acceptable terms, so the best option is to diversify trade, look for investors, and lead a coalition of rules-based partners.”

It’s the right calculation, and the text of his speech made it clear that this only works if “a coalition of rules-based partners” comes together sooner-than-later. In other words, all of this bears close watching. Carney made a brave and insightful speech, underscoring that step one is to call out the bully. But steps 2-n are to build out a new global order while the destructive hegemon wrecks havoc.

Which brings us to:

Carney’s China EV Play

Though he’s very clear that he’s not signing any sort of sweeping trade deal with China, Canada and China did agree to the following:

Breaking with the United States this month during a visit to China, Carney cut its 100% tariff on Chinese electric cars in return for lower tariffs on [certain] Canadian products.

Carney has said there would be an initial annual cap of 49,000 vehicles on Chinese EV exports coming into Canada at a tariff rate of 6.1%, growing to about 70,000 over five years…in exchange, China is expected to begin investing in the Canadian auto industry within three years.

This is a smart play, one we should emulate. China makes high-quality, affordable EVs, that are allegedly quite fun to drive. Travel to almost any other advanced country and you’ll see them. In fact, you’ll see too many of them, as China’s mercantilism—export driven growth to an extent that saps demand from importing countries—is in full view.

But with a low quota and an agreement to build here, we accomplish numerous goals. First, we push out the EV demand curve more than the supply curve (because of the low quota) which helps domestic EV producers. True, our automakers have soured on EV production, but I predict that would change once folks learn that low-cost, high-quality EVs are a possibility. If so, and with the engineering partnership that’s part of the deal, we start making affordable EVs here.

And I haven’t even mentioned the environmental advantages.

If you’re thinking this will never happen under Trump, you’re of course right. Truth be told, it would probably be hard for any politician to pull this deal off in the US (to be clear, the Canadian autoworkers weren’t exactly applauding the agreement). And maybe by three years from now, US automakers will figure this out themselves. That was certainly our goal in the Biden admin, nudged by incentives to build and sell domestic EVs. But those days and incentives are behind us.

For now, we should watch this carefully from our side of the border and see how it plays out.

Inflation, Spending

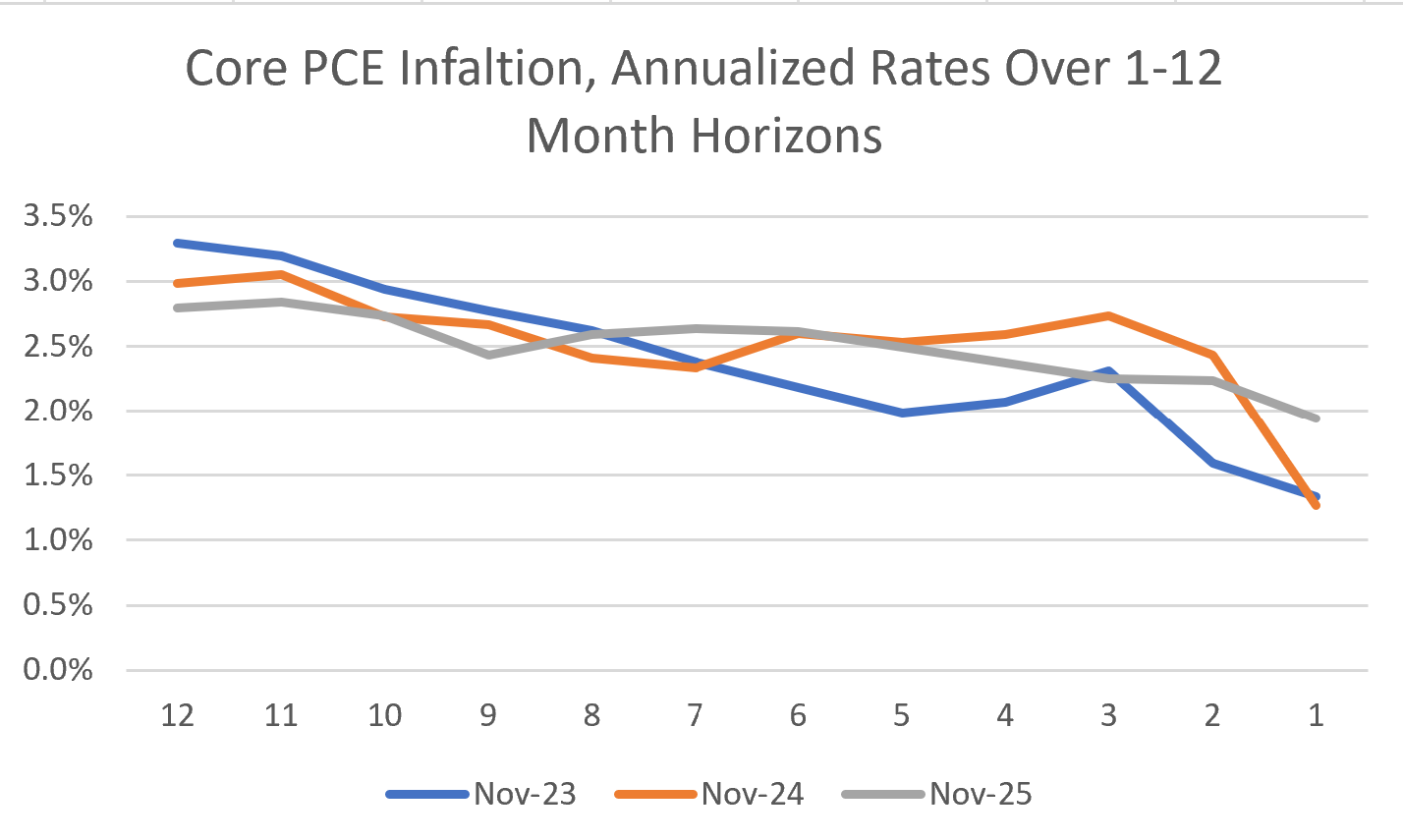

I covered this when the data came out and don’t have much to add at this point. I’m always interested in whether inflation is speeding up or slowing down (i.e., the price level’s second derivative) and a popular way to do that is to look at annualized rates of change over shorter time periods to try to capture more recent change dynamics than you’d get from year-over-year measures.

This figure shows this for PCE core inflation for the past three Novembers. All rates are annualized, and the numbers on the x-axis show the months used for the change. EG, 12 is yr/yr, 6 is 6-month ann change, etc. If the curve trails down towards the shorter monthly changes, it suggest inflation is slowing.

In a pattern that underscores points Chair Powell has recently leaned into, the direction of travel is lower inflation at higher frequencies, though perhaps a bit less so now than in ‘23. Anyway, that’s a good sign re core inflation slowly working its way back to target, one that’s harder to see if you just look at yr/yr.

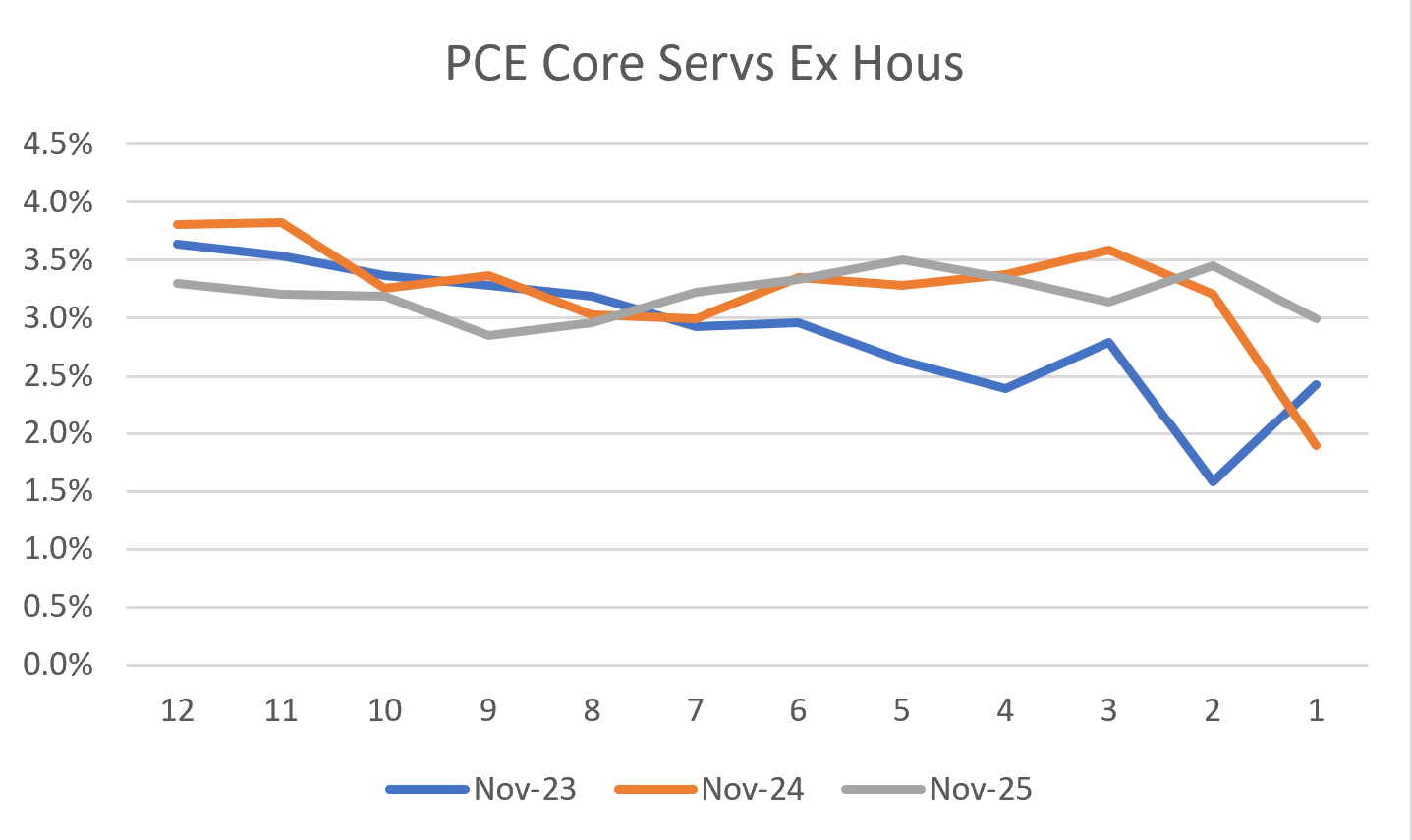

But I remain concerned about core services (ex-housing) inflation. Here’s the same figure for those prices. The line for the most recent data (Nov25) is flat, suggesting little deceleration.

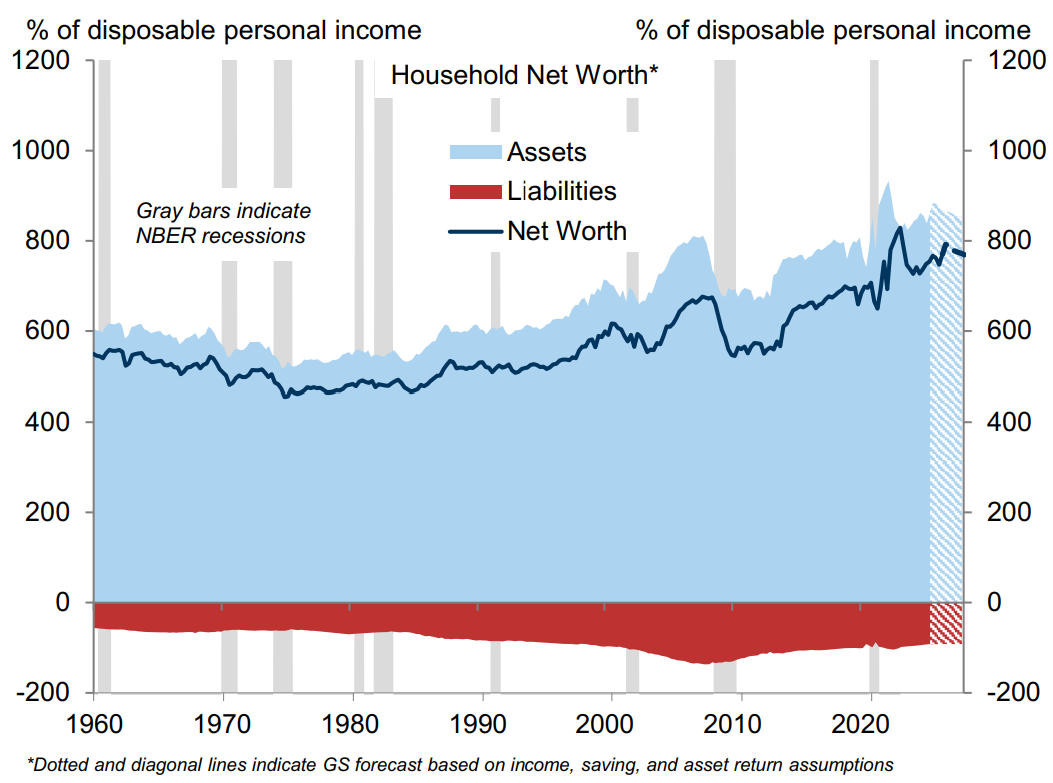

As noted in my report, real spending just keeps on truckin.’ It may well be K-shaped (fueled more by high-end spenders) as some recent evidence has suggested, and as I suspect is probably true. There’s another variable helping to support spending these days which I didn’t show in my original write-up: net worth (assets - liabilities). Here’s a look at that from GS researchers with a forecast at the end. Again, this is an aggregate, driven by high-end financial portfolios and housing wealth. But it is definitely supporting consumer spending.

Japan’s Debt Selloff: Could It Happen Here?

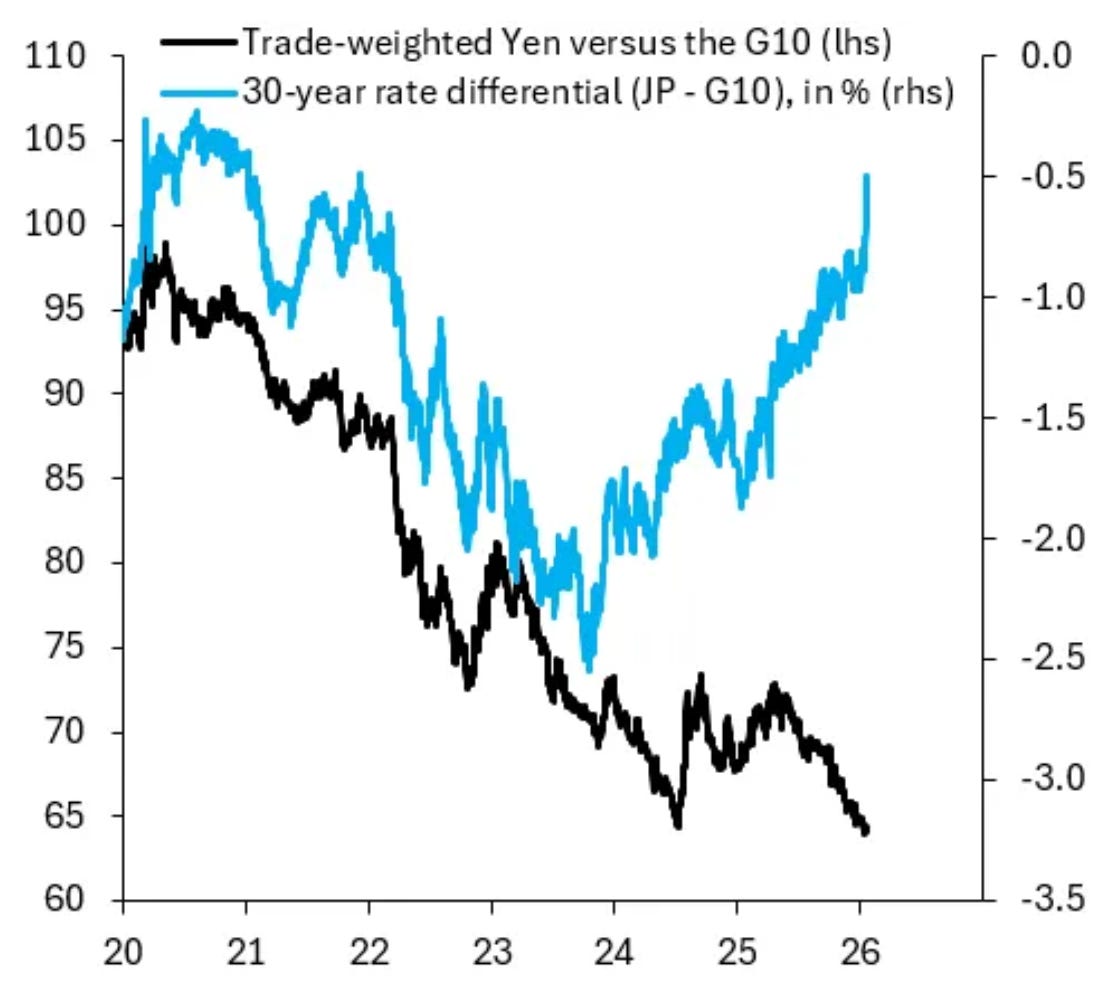

Read Robin Brooks (that’s his figure and text below) to get the gory details but Japan appears to be in the midst of its own mini-Liz-Truss moment.

Prime Minister Takaichi is running on an end to “excessive” fiscal austerity. That’s highly irresponsible. I’ve been flagging for a long time that we’re in the early stages of a global debt crisis. Long-term government bond yields have risen sharply everywhere. Markets are losing patience with governments that are chronically unable or unwilling to bring public debt down. This is no time to pretend Japan’s humungous debt isn’t a problem. Denial isn’t a plan.

The fact that the yen is falling while the interest rate is rising is a signal that investors in Japanese debt, which is famously north of 200% of Japan’s GDP, are spooked.

Now, where have we seen that before?? Ah yes, the old Trump-induced “sell America” trade. And if Brooks is right re “markets losing patience” with countries whose fiscal outlook is unsustainable, then Houston, we have a problem wherein buyers of US debt begin to insist on risk and inflation premia, meaning higher interest rates and higher debt service.

As I’ve written, I think there’s something to that, but the US still remains significantly insulated from creditors’ angst. Our sovereign debt market is close to 4x the size of Japan’s and is highly liquid, our currency is the global reserve; even with all the Orange Madness, US safe-haven status remains intact. I do not see a Truss moment in our near or even medium-term future.

But that status has been dented, our dollar/rate pattern is similar to that above (weaker dollar, higher interest rates), and refuge-in-gold has pushed that price up to new highs. Trump is both making the fiscal outlook a lot worse (I’ll have some hard-hitting new evidence on that out soon) and even worse, he’s aggressively chipping away at the safety and liquidity of US markets.

Okay, you’re up-to-date even if it’s a day late and a weaker dollar short.

Let's all decide not to live within the lie. If Trump can rename cabinet positions, so can we. The Department of Homeland Security is now the Department of Domestic Warfare. After all, he told us, "The enemy is within."

The only downside to limiting Chinese EVs is that it induces them to send their priciest ones. We actually want their lower-end models that compete with polluting used cars more than with new ones.