Weekly Wrap-Up: Pre-War baseline + Post-War Econ Impacts

Yes, it's oil and gas. But it's not just them.

Late last week some data came in that looked concerning, and these were pre-war data. One report showed slower growth than we’d thought and another showed higher inflation; thus they flashed stagflation vibes.

Starting with real GDP growth, 25Q4 was revised down from an already low 1.4% to half that: 0.7% (annualized quarterly growth rate). That’s not great but it’s better than it looks, because the gov’t shutdown that quarter shaved over a point off the growth rate. To be clear, that doesn’t mean it didn’t happen or that it was costless! But it does mean that some of the growth lost to the shutdown in 25Q4 will get added to 26Q1, which is tracking at around 2.5-3%.

Bottom line, GDP is probably growing at around trend, which is around 2%. More accurately, it was growing at trend before the admin started this war, which is having many negative economic effects beyond the gas price. More on that in a moment.

If the GDP data were better than they looked, the inflation data—January PCE—looked concerning, full-stop. In fact, there was a smallish data issue here which made the slightly-hotter-than-expected inflation data look a little better than they were.

Given that these were January data, we’re definitely looking in the rearview mirror here, but given that they were already a bit warmer than expected and the war is putting more pressure on future inflation prints, this is a problem for both consumers and the Fed.

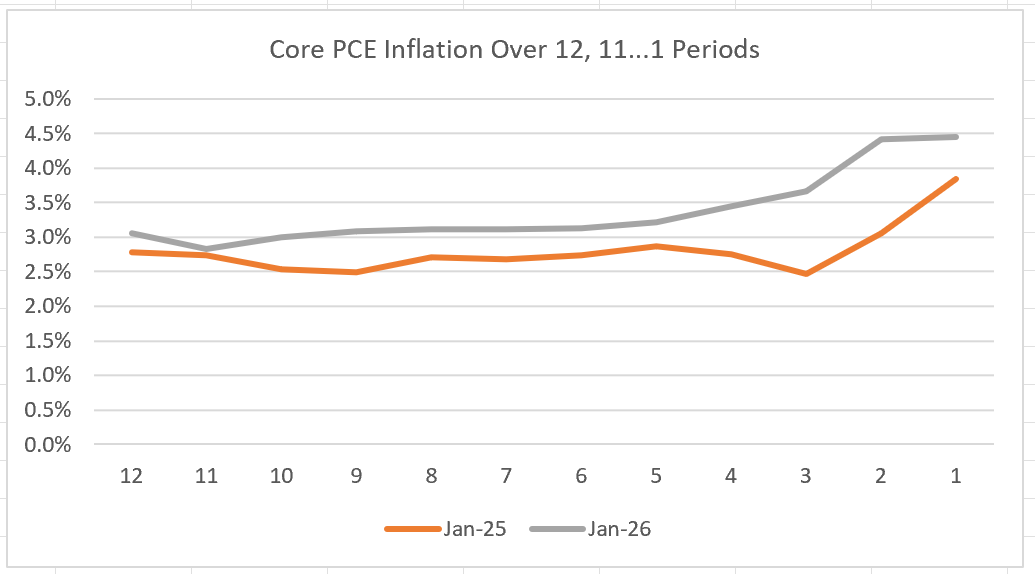

I may be the only one who likes to look at it this way, but I like to assess both where inflation is and where it might be headed by plotting annualized growth rates at 12, 11, 10,…,1 month intervals. This allows us to assess the level of inflation across time periods by comparing the lines over different months—in this case, the most recent Jan ‘26 print against Jan ‘25’s print—as well as whether shorter annualized periods are growing faster, implying potential acceleration.1

What you see above is that our most recent read on core PCE is growing faster than it was a year ago, and possibly accelerating a bit. Some unwelcome trends were also seen under the hood. EG, core goods inflation, which likely reflects tariff effects, has gone from its pre-pandemic pattern in ‘24 to tracking significantly higher this year, and core services inflation, which doesn’t have a direct tariff connection, is stuck well above its pre-pan rate.

There was a sort of data glitch in these inflation data, or at least a minor switch in how the gov’t statisticians produce the PCE (a source swap in how a minor component is calculated). Ben Casselman covers it here if you want weedy details, but what caught folks attention is that this change both lowered the reported PCE inflation rate by almost a tenth, and it wasn’t announced in advance by the BEA. That’s not totally unprecedented but in the current climate, it’s a notable mistake.

Omair Sharif, an inflation analyst to whom I listen closely, told Casselman, “On its merits, you can defend the change. Optically, it’s just not a good look in an environment when people are worried about political interference.”

I’ll say more below about the implications of this warmer inflation for the Fed, but bar for a rate cut has gotten higher.

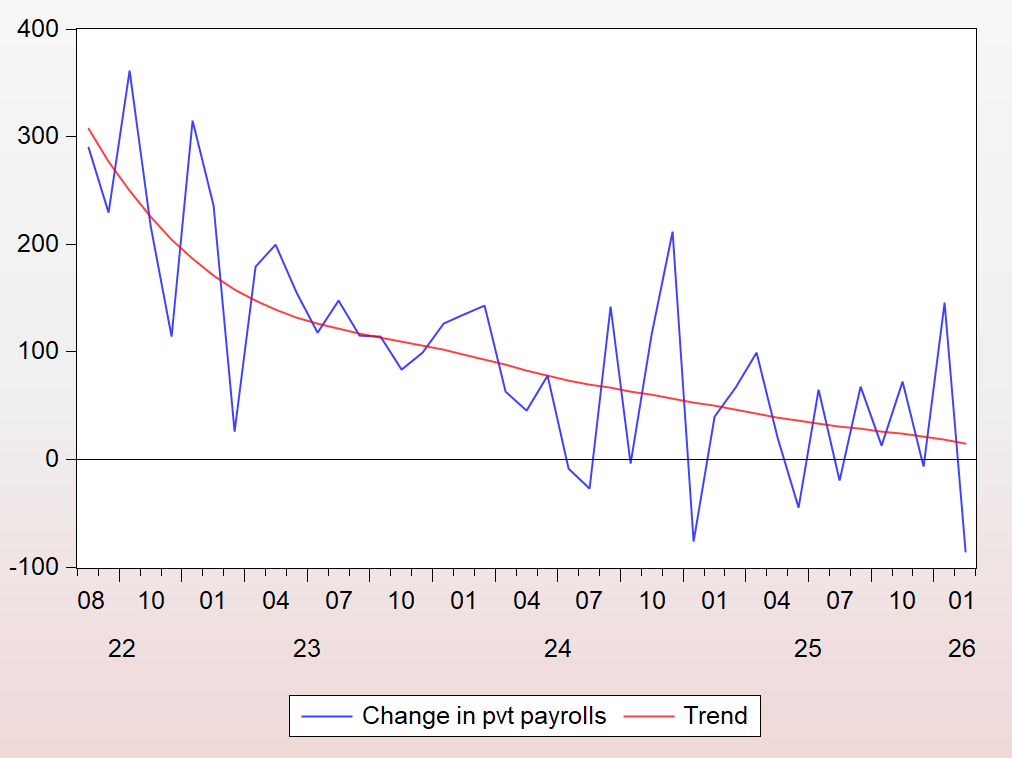

The last pre-war baseline point I’ll make is about employers’ hiring strike in the labor market, reposting a figure from last week on the February jobs report. It shows the very jumpy monthly changes in private-sector jobs with a smooth trend cutting through the data. The last trend data point was about 15,000 added jobs per month, which, should it persist, is too low to prevent unemployment from rising.

That’s the Pre-War Baseline: Here’s Some War Impacts

As the NYT put it yesterday:

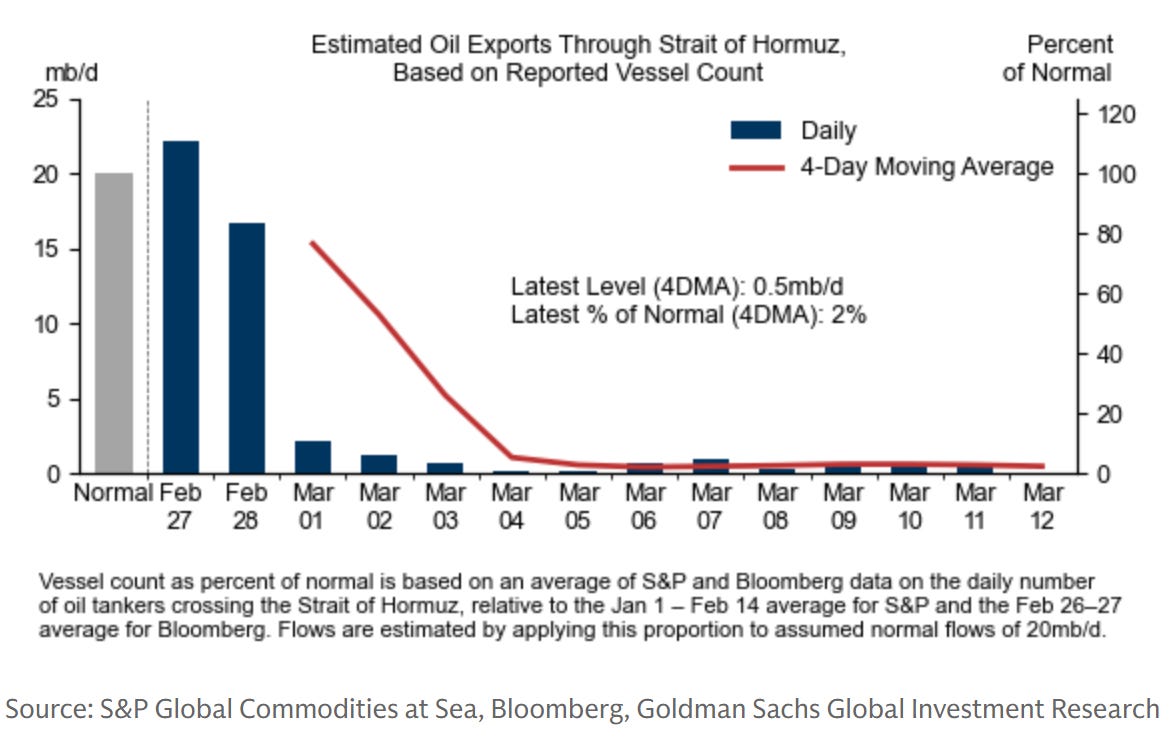

From the start, I’ve argued that the key variable re economic impact is duration. In this regard, look at flows through the Strait of Hormuz, or the lack thereof:

Now, I suspect you heard, as I did, our benighted Sec’y of War and Lethality assure us that were it not for Iranian missiles and drones, the transit would be fine, and that we “don’t need to worry about it.” Not only is this further evidence that this war is being prosecuted by inept people who never should be there in the first place—a reminder of the culpability of the Senators who confirmed them. Re duration, we can’t trust what they’re telling us. A far lesser concern is that this is also going to make it very hard for Colin Jost to parody Hegseth on SNL.

On the lower-duration side, I read something interested today: the Ukrainian drone blockers are now helping us in the war zone. No one knows more about how to block drones than they, so, given that Iran’s ballistic missile capacity is reportedly low, this is a positive development.

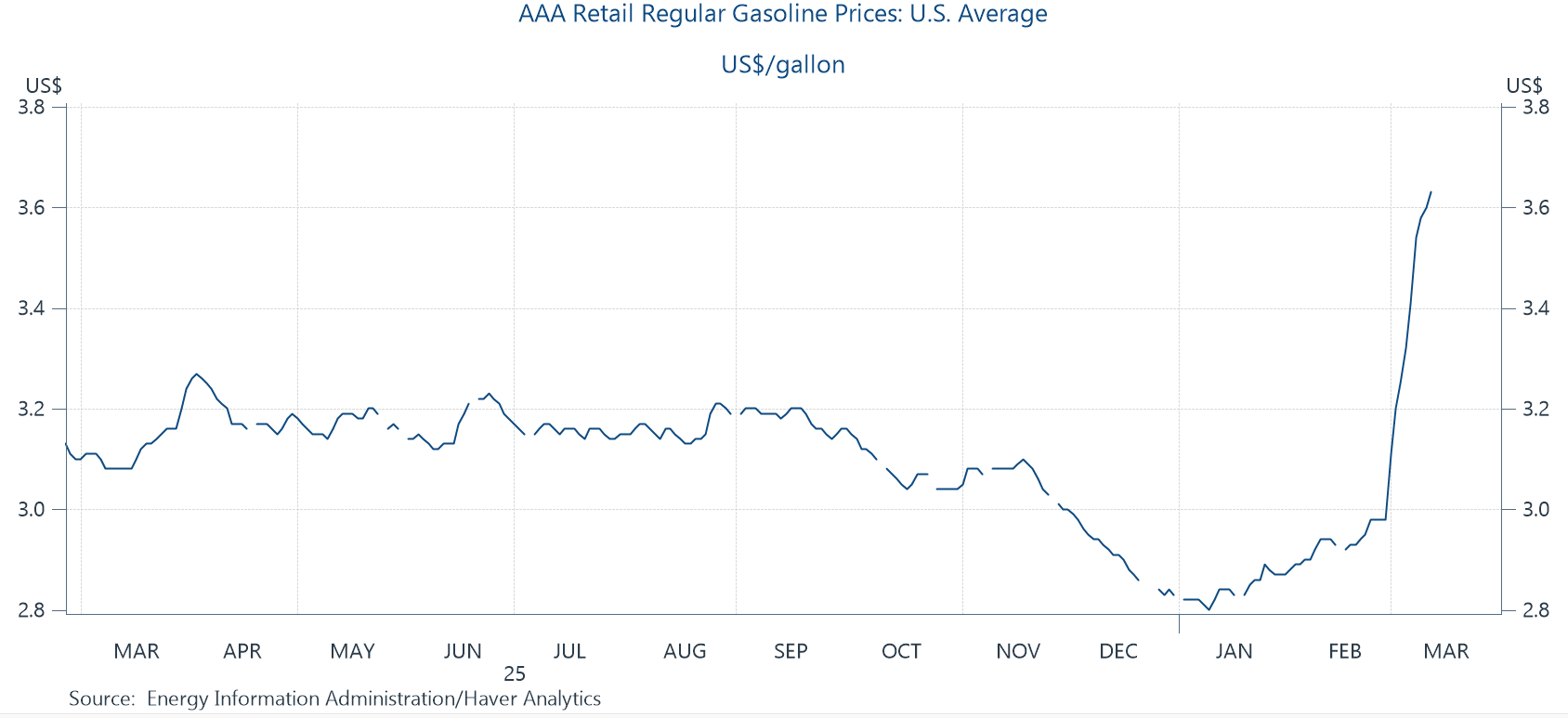

Of course, the first post-baseline impact on consumers is gas at the pump. The figure below is through Friday. Sunday AM, the gas price is up again, hitting $3.70, its highest since Oct 23 and 26% above its value of $2.93 a month ago.

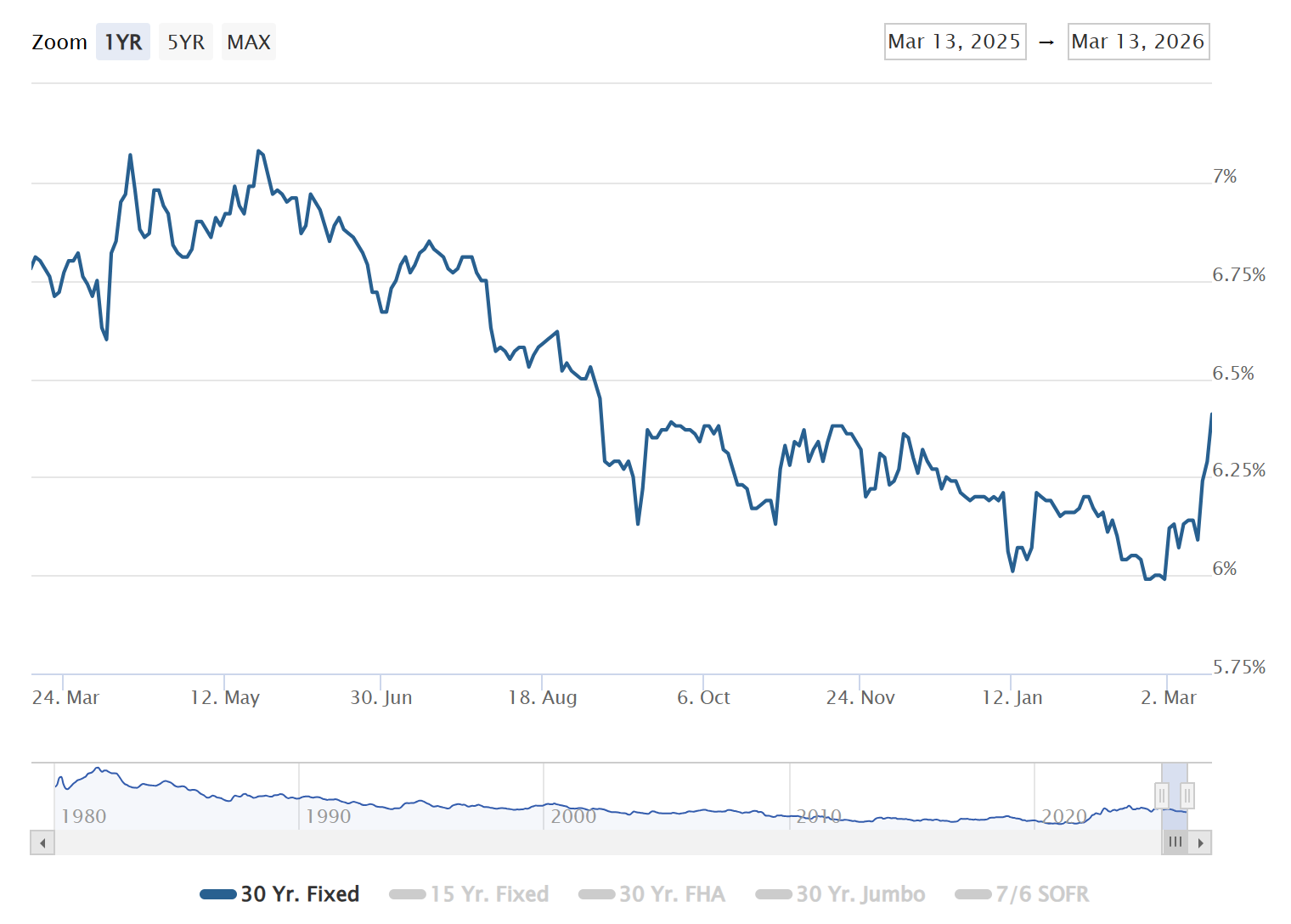

That’s boosting inflation (headline more so than core) and interest rates. Re the latter, the spike you see below in the 30-year fixed rate mortgage is another important war impact. The FRM moves with the 10-year gov’t bond yield, which is up since the war. I was talking about this with economist and housing-finance expert Mark Zandi, who judged that it was very likely to “short circuit” the recent increases in refis and home sales.

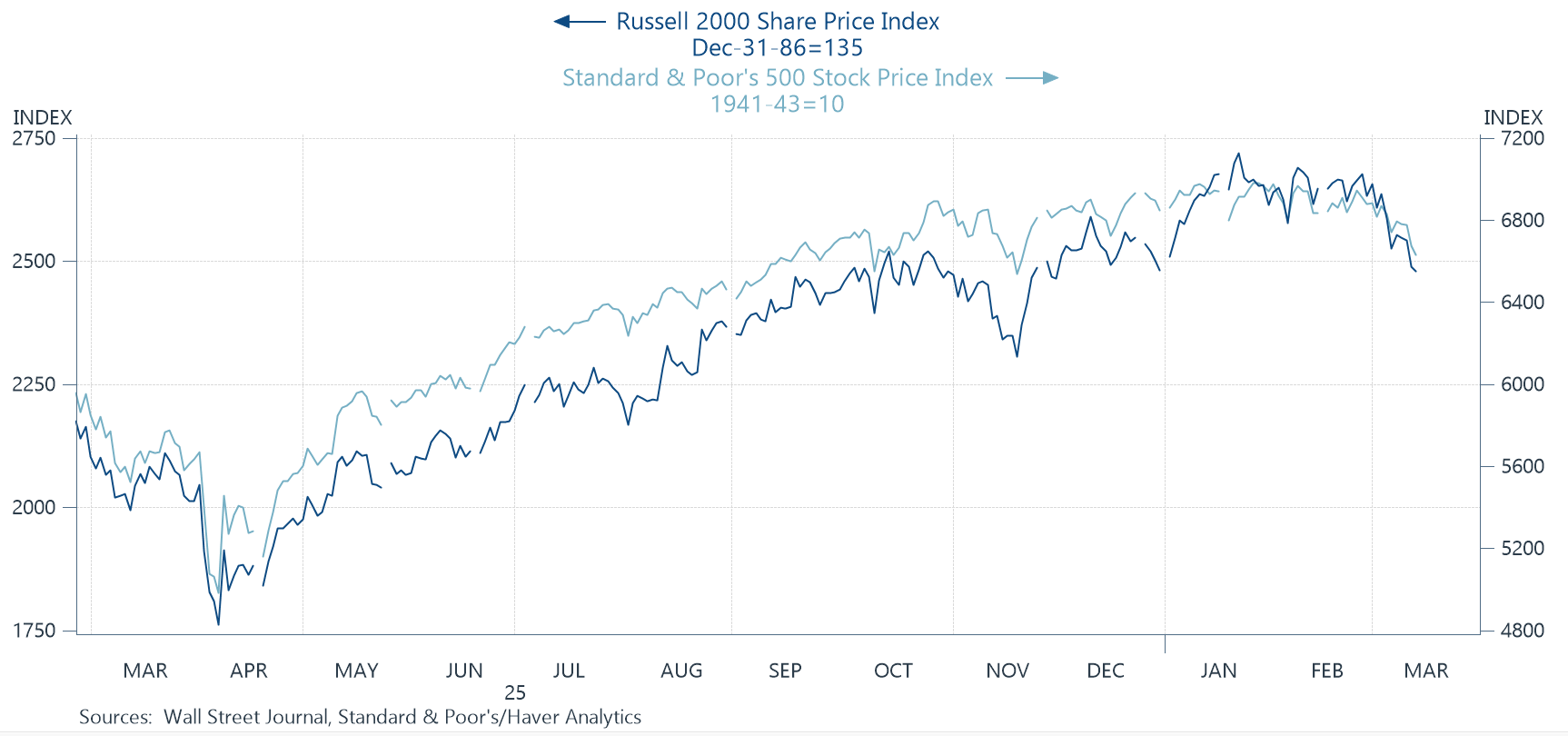

Equity markets, which tend to be a Trumpian benchmark, have been trending down, including the Dow, S&P, and small caps (Russell 2000). The so-called “fear index,” the VIX, which in normal times tracks around 17, closed at 27 on Friday, after peaking at 40. I’m confident that this is a partially a symptom of the fact that we can’t begin to trust the reporting of the leadership, which failed to prepare people and markets for this war.

Re where inflation is headed, here’s a repeat of a slide I shared from GS Research earlier in the week, showing that their baseline forecast is for PCE inflation (the gauge the Fed follows most closely) to jump about a point, with much bigger jumps from more adverse oil scenarios. Their core forecast is, as expected, more benign, but, in tandem with the news above about Jan’s PCE, it should surprise no one that futures markets have gone from expecting two Fed cuts this year to expecting none. This is one of the factors pushing up the mortgage rate, btw.

Okay, I’ve battered you enough with facts and figures for today. Two final quick points.

First, here is our president, speaking on Thursday in Kentucky:

“Inflation is plummeting, incomes are rising, the economy is roaring back and America is respected again.”

Other than his MAGA base, I can’t imagine anyone is buying such misinformation, and the polls strongly suggest I’m right about that. I’ll just say that unilaterally taking the country into an immediately unpopular war and lying about its economic impacts is both a losing political strategy (see figure below, from this source) and antithetical to democracy.

Finally, I know folks are wondering if all these war impacts are recessionary. It is not obvious to me that they are. Remember, the US oil majors are doing great on the back of the war, and thus far, the US economy has been extremely resilient to destructive Trumpian policies. EG, there’s no reason to think the war will dampen the AI investment boom. The billionaire class certainly remains intact.

But for regular folks, these war economics hurt, and that’s on top of the existing hurt they’ve been experiencing in the pre-war baseline. If there’s any upside to this, it’s that it should now be clearer than ever that this president and his lackies have zero interest in their interests.

One problem with this approach is that the annualized rates over shorter periods are more volatile.

People vote with their dollars but the evil associated with a corrupt system has a way of eroding souls and diminishing humanity. And, as corrupt as America is, it is currently at it's worst and still descending into the depths of evil. Bottom line: Y'all may be keeping your 401Ks and buying crap but the world hates you and you hate yourselves, That's gonna show up in every aspect of 'Merican society. And I think it already is......

The AI boom is dependent on continuing supplies of advanced silicon chips. Making those chips is dependent on a continuing supply of helium. A large fraction of the world's supply of helium goes through the Straits of Hormuz. So maybe AI isn't going to provide an impetus to the economy.